ELSS Vs NSC: Risk, Tax Benefits, Difference, Which is Better

Updated on June 19, 2024

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

What is ELSS?

Equity Linked Savings Scheme (ELSS) is a mutual funds scheme that invests in equity markets while providing tax saving benefits. ELSS is considered to be diversified in nature as it invests in stocks of companies across different sectors and market capitalizations. Returns earned are directly linked to the performance in the markets. This scheme is very popular among investors for its potential to generate the highest returns amongst all the tax saving investment options available in the market. As the major portion of investments are made in equities, elss funds are advisable for those investors who have a long investment horizon of at least 5 years.

Let’s take a look at the principal features of ELSS or Tax-saving Mutual funds.

Features of ELSS

1. Long-Term Investment

ELSS has a lock-in period of three years which means it is mandatory for the investors to remain invested in the scheme for at least three years without exiting. After three years, it is up to investors to either exit or stay invested in the scheme. However, it is advisable to stay invested in ELSS schemes for as long as possible (subject to periodic reviews) to earn good returns.

2. Tax Benefits

When it comes to ELSS, one can avail a tax deduction of up to Rs. 1.5 Lakhs under section 80C of IT Act, 1961 on investments in ELSS annually. There is no upper limit set for the amount of investment one can make in a financial year.

Since the investments in ELSS funds are held for more than 1 year, the returns are subject to Long Term Capital Gains (LTCG) Tax. This is applicable on returns that surpass Rs. 1 lakh in a financial year and are taxed at 10%.

3. Risks

ELSS funds usually involve moderate to high levels of risks (depending upon the investment style of the fund) due to investments in equity markets. ELSS investments involve the risks of instability or volatility in the Net Asset Value (NAV) of funds due to their equity market exposure. Therefore, ELSS funds are recommended to investors having high risk tolerance.

Read: Best ELSS Mutual Funds to Invest in India

What is NSC?

NSC stands for the National Savings Certificate which is a post office savings scheme carrying the sovereign guarantee of the government on the investments as well as the returns earned. The saving scheme was launched with an objective to encourage a habit of savings & investments among citizens for meeting long term financial goals. The rate of interest on the certificate is subject to revisions by the government every quarter. Currently, the scheme offers an interest rate of 6.8% which is compounded annually. The minimum amount required to make investments in NSC is Rs 1000 and there are no upper limits. The National saving certificates are also one of the popular tax-saving investments available in the markets and are generally preferred by investors looking for risk-free returns & investment.

Let’s have a look at the principal features of the National Savings Certificate.

Features of NSC

1. Investment Tenure & Lock-in Period:

NSC has a maturity & lock-in term of five years. Premature withdrawals are only allowed under certain circumstances.

2. Tax Benefits

An investor can claim tax deductions of up to Rs. 1.5 Lakh per annum under Section 80C of the Income Tax Act, 1961 on investments in NSC.

3. Risk

NSC involves very low or almost negligible risks since this investment is backed by the government of India.

Differences between ELSS and NSC

There are various differences between ELSS and NSC, some of which are discussed below:

1. Nature

Equity Linked Savings Scheme (ELSS) are mutual fund schemes that invest in equity stocks to generate returns for investors along with providing them tax benefits under section 80C. On the other hand, National Savings Certificates (NSCs) are small saving schemes offered by the post office that provide guaranteed & risk free returns on investment.

2. Lock-in Period

ELSS have a lock-in term of 3 years which is the lowest among all the tax saving investments whereas NSC has a lock-in term of 5 years.

3. Taxation

In the case of investments in ELSS, one can avail a tax deduction of up to Rs. 1.5 lakhs annually. For holdings longer than 1 year, returns that surpass Rs. 1 lakh within a financial year are taxed at 10% Long Term Capital Gains (LTCG) Tax.

When it comes to NSC, an investor can claim a tax deduction of up to Rs. 1.5 Lakh per annum Section 80C, as well. However, the interest earned on the investments is taxable as per the income tax slab of the investor.

Also Read:

4. Risks Associated

ELSS funds usually involve moderate to high levels of risks due to investments in equity markets.

NSC, being a government backed scheme, involves very low levels of risks and is in fact considered almost risk-free. This investment is recommended to investors who have low risk tolerance.

5. Returns

The expected returns from ELSS funds are 12-15% for long term investments.

NSC, as of July 2020 offers an interest rate of 6.8% which is compounded annually and is paid at maturity. The interest rates are subject to quarterly revisions by the government.

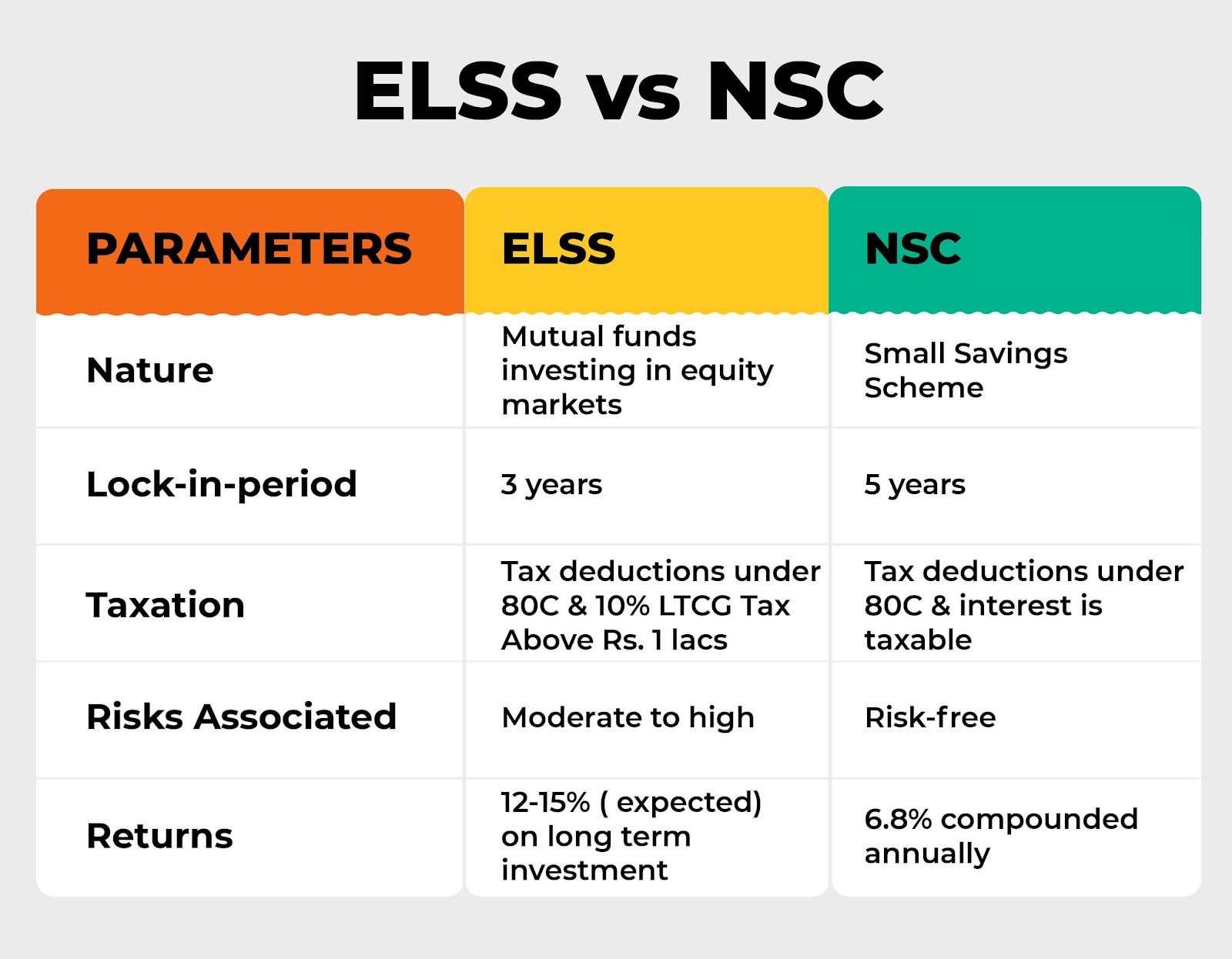

| Parameters | ELSS | NSC |

| Nature | Mutual funds investing in equity markets. | Small Savings Scheme |

| Lock-in period | 3 years | 5 years |

| Taxation | Deduction under Section 80C of up to Rs. 1.5 lakhs. LTCGs- 10% Tax on returns above Rs.1 lacs. | Deduction of up to Rs. 1.5 Lakh per annum Section 80C. Interest taxable. |

| Risks Associated | Moderate to High | Risk-free |

| Returns | 12-15% (expected) on long term investments | 6.8% compounded annually |

Which is better, ELSS or NSC?

Both these investments are popular tax saving investments. The risk-return characteristics of these investments are very different and hence are suitable for different kinds of investors. Investors having a high risk appetite should consider investments in ELSS funds for their tax saving needs as they would have the potential to generate higher returns. While, investors who are risk-averse would be better off investing in NSC which will provide stable & guaranteed returns on their investment.

More Information:

ELSS VS PPF - Comparison, Tenure, Risks, Returns, Tax Benefits

ELSS vs ULIP: Risk, Cost, Returns, Coverage, Tax Benefits, Which is Better

Difference between Direct And Regular Mutual Funds

Best Large Cap Mutual Funds to Invest in India

Best Small Cap Mutual Funds to Invest in India

Best Multi Cap Mutual Funds to Invest in India

Best Mid Cap Mutual funds to Invest in India