Employees Provident Fund (EPF): Benefits, Eligibility, Forms, Registration Process

Updated on June 27, 2024

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

Employees’ Provident Fund (EPF)

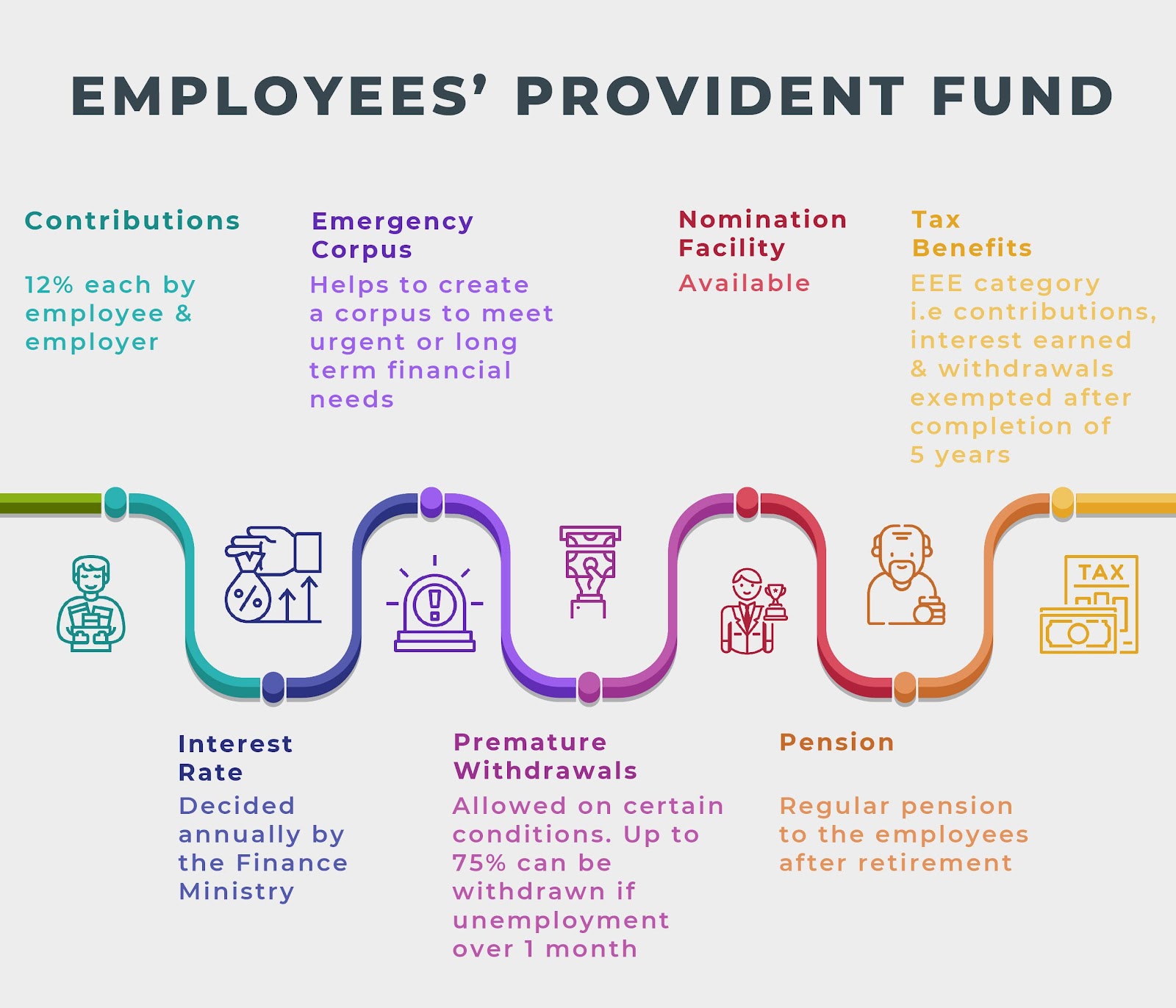

Employees’ Provident Fund (EPF) is an investment scheme introduced under Employees’ Provident Funds and Miscellaneous Act, 1952. The EPF investment scheme is managed by Central Board of Trustees (CBT) and activities are assisted by Employees’ Provident Fund Organization (EPFO). In this scheme, an employee is supposed to contribute 12% of his/her income monthly to the fund. The employer has to match the amount with equal input so that when the employee retires, he/she is entitled to receive complete corpus including private as well as employer’s contribution along with interest. The EPF scheme involves low levels of risks. There are certain provisions set for this scheme such as a company which has employed at least 20 employees needs to maintain EPF accounts and the provision of an EPF account is mandatory for employees with wage lower than Rs. 15,000 per month to register for an EPF account. However, employees with more than Rs. 15,000 per month can also register for an EPF account with the approval from Assistant PF Commissioner.

Features and benefits of Employees’ Provident Fund (EPF)

The EPF scheme has very attractive features and benefits which are mentioned below:

1. Emergency Funds

This scheme helps the individuals to create an emergency corpus which can be used or withdrawn from the account for meeting emergency needs.

2. Rates of Interest

Currently, the rate of interest on the EPF Deposits is 8.50% per annuum. The interest earned goes to the EPF account on an annual basis. The interest rate is decided by the Government of India with the Central Board of Trustees (CBT).

3. Tax Benefits

The EPF scheme investment falls under the category of Exempt-Exempt-Exempt (EEE) in which Exempt 1 stands for investments being qualified for deduction under section 80C and a section of annual income which is equal to investment amount is not taxable. Exempt 2 stands for interest earned on investment is exempted and Exempt 3 stands for amount generated from investment isn’t taxed during the time of withdrawal. However, this tax benefit isn’t available in the case where the investor withdraws investment before completing five years.

4. Premature & Partial Withdrawal Facility

The EPF scheme allows investors to withdraw prematurely and partially under certain terms and conditions. Partial premature withdrawal is permitted in the cases of medical expenditures, marriage, higher education purpose, purchase of land or property as per the pre-defined limits. Partial premature withdrawal facility is available only after completing five financial years. In the case of unemployment or resignation for more than 1 month, investors can withdraw up to 75% of EPF corpus to meet financial requirements. And for being unemployed for two months or more, the balance 25% can also be withdrawn.

5. Nomination Facility

The EPF scheme offers nomination facilities subject to certain terms and conditions.

6. Liquidity

The EPF scheme is generally an illiquid investment. However, in times of a financial emergency, provisions for premature withdrawal are available. This withdrawal is subject to certain provisions. Hence, the EPF scheme offers a certain level of liquidation.

7. Accessibility

There is easy access to the PF account for employees through the EPF member portal with the help of Universal Account Number (UAN).

8. Pension

This scheme facilitates making contributions towards employees pension which will be regularly paid to the employee after retirement.

Also Read: Public Provident Fund (PPF): Interest Rate, Eligibility Criteria, Benefits, Application Form

EPF Eligibility Criteria

There is an eligibility criterion set for the EPF scheme. As per law, it is compulsory for companies with more than 20 employees hired to register for the EPF scheme for the employees with wages/salaries less than Rs. 15,000 per month(Basic+DA) to enroll for an EPF account. However, companies with less than 20 employees hired can also enroll into join the EPF scheme voluntarily. Employees with more than Rs. 15,000 per month salary can enroll into this scheme as well after getting approval from Assistant PF Commissioner.

Acts Governing Employees’ Provident Fund (EPF) Scheme

The Employees’ Provident Fund (EPF) Scheme is governed by three acts which are

- Employees’ Provident Fund Scheme, 1952

- Employees’ Pension Scheme, 1995

- Employees’ Deposit Linked Insurance Scheme, 1976

EPF Forms

The EPF Forms are compulsory for all actions that employees would like to undertake in their accounts. These actions may include registration, withdrawal, loan availing, transfer of PF, etc. Different forms and their purpose are mentioned below:

| EPF Form | Purpose |

| Form 31 | EPF Withdrawal |

| Form 14 | To Buy LIC Policy |

| Form 10D | To claim monthly pension |

| Form 10C | To claim withdrawal benefits or scheme certificate of EPS |

| Form 11 | For EPF Account Transfer |

| Form 19 | For Final Employees’ Provident Fund Settlement |

| Form 20 | For EPF Final Settlement if there is a case sudden demise of employee |

| Form 2 | Declaration and Nomination form for EPS & EPF |

| Form 5 IF | Claim according to EDLI scheme |

| Form 15G | To save TDS on the interest income on EPF |

| Form 5 | New employees registering for EPF and EPS |

| Form 11 | For auto transfer of EPF |

Registration Procedure into EPF Scheme for Employers

Certain steps are needed to be taken to register to EPF Scheme which are mentioned below:

1. Go to official website of Employee Provident Fund Organization (EPFO)

2. Go to the section of ‘Establishment Registration’ which opens a new page of ‘Instruction Manual’ which will explain the process of Employer Registration, DSC (Digital Signature Certificate) registration of employer. This is considered to be a prerequisite for new application submission.

3. Proceed further and fill up the details to register.

4. An e-link to email will be sent which has to be activated and a mobile PIN is sent which is required to upload certain documents for registration.

5. Those who have registered can also log in via Universal Account Number (UAN).

Registration Procedure into EPF Scheme for Employees

Universal Account Number (UAN) Activation for EPF Scheme

1. Visit the member website of EPF i.e., EPF e-SEWA/EPF Members Portal.

2. Click on the option of ‘Activate UAN’ which can be found at the right corner of the site.

3. A new dashboard will open where one needs to enter either UAN/PAN/Aadhar and rest of the details like name, birthdate, address, etc. as per the requirements of EPFO Records.

4. Verify the ‘Captcha’ code and receive authorization PIN on registered mobile number with EPFO.

5. Use the One Time Password (OTP) for validation and activation of UAN online.

6. A message to confirm UAN activation will be sent.

7. Once UAN is activated, login with it in order to check the status of PF.

Procedure for EPF Payment

In order to proceed the EPF payment, following steps can be taken:

1. Login to EPFO Portal with the use of Electronic Challan cum Returns Credentials (ECR).

2. Click on ‘Payments’ and proceed to ‘ECR Upload’.

3. Select salary month, wage disbursal date, rate of contribution.

4. Proceed further to upload the ECR text file and select the rate of contribution. A popup will appear on the screen saying ‘File Validation Successful’ in the case when the uploaded file is validated under predefined conditions. If there is a case of file not being validated, pop-up will appear that may say ‘Error’ on the screen.

5. Click on ‘Verify’ as the TRRN will be presented on the screen.

6. In order to obtain the summary sheet for ECR, click on ‘Prepare Challan’.

7. Then enter the required Admin/Inspection Charges and select ‘Generate Challan’.

8. Proceed to pay by clicking on ‘Finalize’.

9. Choose the Online mode as payment mode and choose any bank account.

10. Once the respective bank account is selected; the payment gateway will be redirected to the selected bank account.

11. Make payment via net banking. Once payment is successful and confirmation will be generated with Transaction ID and e Receipt and transaction will further be uploaded on EPFO Portal and confirmation through TRRN number will be provided.

Frequently Asked Questions (FAQs)

1. Does UAN need to be changed if there is a switch in the job?

No, UAN allotted to a member remains the same but a new PF account will be opened by a new employer which has to be linked to the UAN of the employee.

2. What is the time limit for withdrawal of EPF dues?

There is a duration set only in the case of resignation of two months for withdrawal from EPF account.

3. Can an apprentice become a member of EPF?

No, when the person ceases to be an apprentice, he/she may be enrolled immediately.

4. What is the Universal Account Number (UAN)?

Universal Account Number (UAN) is a unique 12-digit permanent number allotted to members and remains the same throughout the working tenure.

5. What is the current rate of interest on EPF Deposits?

Currently, the rate of interest on the EPF Deposits is 8.50% per annuum.

More Information:

PM Vaya Vandana Yojana (PMVVY): Scheme Eligibility, Interest Rate, Process to Apply

National Pension Scheme (NPS )- Tax Benefits, Eligibility, Features, How to Open, Application Form

Kisan Vikas Patra (KVP) Scheme: Benefits, Types, Interest Rates, Eligibility, Calculation

Sukanya Samriddhi Yojana (SSY) Scheme: Benefits, Eligibility, Interest Rate 2020, Application Form

Kisan Credit Card (KCC) Scheme - Eligibility, Interest Rate, Loan, Fee

Post Office Saving Schemes: Plans, Types, Benefits, Interest Rates

Senior Citizen Savings Scheme (SCSS): Interest Rate, Eligibility, Benefits, Calculation