Kisan Credit Card (KCC): Scheme Eligibility, Interest Rate 2021, Loan Fee, Online Apply, Application Form

Updated on February 16, 2023

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

What is Kisan Credit Card Scheme ?

While we were seeing developed economies announcing stimulus packages equivalent to a major chunk of their GDP, our union government was criticized for being very conservative. The measures taken by the lender of last resort aka the RBI, including TLTRO 2.0 wasn’t achieving its objectives effectively. As we were undergoing one of the world’s strictest lockdowns, the government seemed clueless about saving an already plunging economy.

Atmanirbhar Bharat Abhiyan

Amidst all these dire scenarios, the Prime Minister made a few important announcements in his address to the nation on 12th May. He disclosed a special economic package under the banner 'Atmanirbhar Bharat Abhiyan', indicating a mission to make the state self-reliant. He added, under this scheme the government would declare an economic package worth Rs 20 trillion (nearly equivalent to 10% of our GDP). In response to this announcement, we witnessed values of stocks surging in our bourses the following day. While our FM Nirmala Sitaraman presented the scheme in subsequent tranches, the 2nd day of announcements were very significant for farmers, migrant labourers & street vendors.

Read More: ICICI Prudential Freedom SIP

Farmers:

Let us streamline our focus to the plans benefitting the farmers in this composition, especially the one involving Kisan Credit cards. There were 2 significant announcements:

- An extension of additional refinance support of Rs 30,000 crore. This would be the emergency working capital funding for farmers ahead of the kharif season.

- To boost the farming activities, a concessional credit of Rs. 2 lakh crores will be offered to about 2.5 crore famers. This would be enabled through the Kisan Credit Card (KCC) scheme. The plan also covers fishermen and animal husbandry farmers.

The FM also specified that close to 25 lakh new Kisan Credit Cards are about to be distributed to small and marginal farmers.

Know More About Kisan Credit Card Scheme(KCC)

As most people think, the Kisan Credit Card scheme is not a fancy product of digital India. Believe it or not, the KCC scheme had been introduced in August 1998 by the banks of India. It was announced as a part of the 1998-99 budget, with an intention of satisfying the financial needs of farmers through institutional credit. On the recommendations of R.V. Gupta committee, the model scheme was prepared & proposed by NABARD (National Bank for Agricultural and Rural Development) and the RBI. The participating entities are Co-operative banks, Regional Rural Banks (RRB) and all commercial banks as well.

The basic objective of the scheme is to offer loans to the farmers at a concessional rate, for various stages of agricultural activities. This could save farmers from getting stuck in a debt spiral, as local moneylenders could charge at rates as high as 60-70%. Although the KCC helps farmers get emergency credit for short-term needs, they can also take term loans for various substantial needs.

Eligibility for Kisan Credit Card

- Farmers who are individual or joint borrowers of the cultivable land are eligible for KCC scheme.

- Anyone who is in the age group of 18 to 75 years, engaged in agriculture or allied activities can apply for a Kisan Credit Card.

- If the farmer is a senior citizen (60 years and above), a co-borrower is mandatory (who must be a legal heir).

- The eligibility is also extended to tenant farmers, oral leases, shared croppers and the self help groups or joint liability groups formed by them.

- The KCC scheme has also included fisheries (inland/marine) and animal husbandries (poultry/dairy) as beneficiaries.

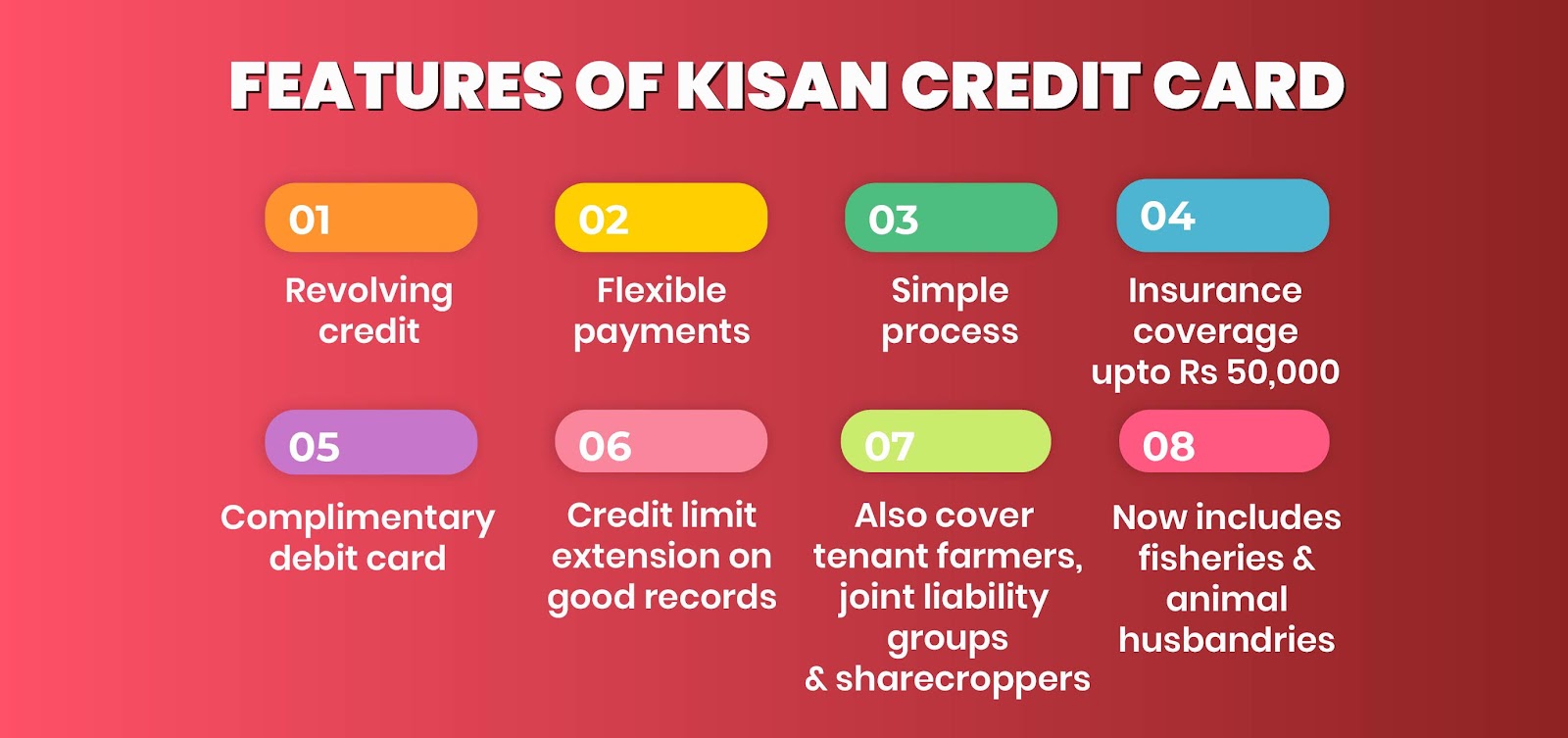

Features of Kisan Credit Card:

- Revolving Credit: If the borrower is not able to pay within time, the amount can be added to next month’s statement, after charging a minimal interest.

- Flexible payments: On occurrence of a calamity or a pest attack, the beneficiary is allowed to reschedule payments.

- Simplicity: The processes including application for KCC, screening of borrowers and credit disbursement are all simple and hassle-free.

- Insurance Coverage: The borrowers are covered up to Rs 50000 for death and Rs 25000 for accidents resulting in disability.

- The farmers are issued a debit card in addition to the Kisan Credit Card

- On grounds of good credit record, the credit limit can be extended to borrowers at the discretion of the issuing bank,

- The scheme is not limited to owner-cultivators. It also covers those farmers who cultivate on others’ land (tenant farmers), Joint liability groups and sharecroppers.

- The Kisan scheme now includes fisheries and animal husbandries as beneficiaries. This encompasses inland / marine fishery, poultry and dairy.

Read More: Top Multi Cap Funds to Invest in India

Getting a Kisan Credit Card:

Kisan credit cards can be obtained both in offline / online mode. For people who are not comfortable in accessing the internet, banks extend this service at their rural branches. Any farmer who wishes to benefit from this scheme must produce the documents including ID proof, address proof, filled application form, land documents and a passport size photograph.

Kisan Credit Card Online:

A few banks offer the facility of applying for Kisan credit card online, through their websites. Their ‘Agricultural banking’ section has the provision to apply for KCC online. After filling the application form in the ‘Kisan Credit Card’ tab, an application reference number is received. The bank contacts the applicant for document verification, and the KCC is delivered to the registered address in the event of successful verification.

Kisan Credit Card Loan:

The term loans offered under the Kisan Credit Card scheme is one of its salient features. The credit given using the card might suffice only short-term requirements. However, for significant expenses like equipment purchase, fertilizers procurement and other agricultural expenses. Numerous factors are considered before disbursing KCC loans to the farmers. It includes credit record, type of crop, land area cultivated etc. On satisfactory terms, the loan amount could be even up to Rs 3 lakhs. The issuing bank makes the decision of securing collateral for the loan and repayment duration, depending on the above said factors.

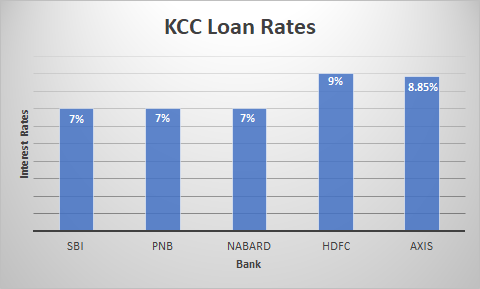

Kisan Credit Card Interest Rate and other charges:

The rate of interest charged on a KCC loan is dependent on different criteria including crop type, land area cultivated, loan amount claimed, value of land etc. However, on an aggregate level we can see that the KCC interest rates fall in the range of 7% to 12%. Apart from the interest charges, banks also collect service charges for collateral valuation, insurance premium, processing fee, land mortgage deed charges etc. These charges vary with the lending bank. SBI waives off these charges for loans up to Rs 3 lakhs.

The above rates of interest might change on grounds of conditions like government subvention, prompt repayment etc.

Read More: Investment Advisor

Success story of Kisan Credit Cards in Agriculture sector:

Prior to the introduction of Kisan credit card yojana, farmers had to apply for loans every cropping season. This hiccup was resolved by the KCC scheme where revolving cash credit was made available. Also, the card is valid for 5 years which is a big relief for farmers. The interest rates are quite low as compared not only to local moneylenders, but also in comparison with a lot of other schemes in Scheduled Commercial Banks. In addition to this, at various points of time the government gave subvention to these interest rates, bringing it down effectively to around 4%. We could also see a major share of farm loans are now given by SCBs, thanks to the advent of the KCC plan. As per the latest statistics updated on PM Kisan web portal, there are around 6.67 crore active accounts utilizing the KCC scheme. Since its inception, the scheme has become the main vehicle of short-term credit for agricultural consumption needs.

Also Read: Kisan Vikas Patra Scheme

Challenges faced:

Though the KCC scheme seems to have aided farmers in various fronts, we could not witness any significant improvement in agricultural productivity. This could be attributed to various factors including failing monsoons. Since the plan is only for short term consumption, we may not be able to address a substantial turnaround in the agricultural sector. Another issue faced by the scheme is farmers making arbitrage gains, thanks to its attractiveness. Due to the low-interest rates, borrowers divert these funds to personal financial consumption rather than agricultural consumption. However, adequate vigilance by the lending banks could help cease this issue.

Latest improvements in the KCC scheme:

- On 21st April 2020, the RBI asked banks to extend the interest subvention of 2%. Also, they prompted banks to provide a moratorium of 3 months.

- The RBI announced on 5th May 2020, KCC could use their cards for household expenses (Max. 10% of loan amount).

- On 14th May, FM Nirmala Sitharaman revealed that GoI will extend 2 lakh crore concessional credit under Kisan Credit Card yojana.

Kisan Credit Cards by Top Banks

- HDFC Kisan Credit Card by HDFC Bank

- Axis Kisan Credit Card by Axis Bank

- SBI Kisan Credit Card by State Bank of India

- PNB Kisan Credit Card by Punjab National Bank

- ICICI Kisan Credit Card by ICICI Bank

- BOI Kisan Credit Card by Bank of India

- BOB Kisan Credit Card by Bank of Baroda

Read More: nism online courses

Frequently Asked Questions About Kisan Credit Card Scheme

Q. How long is the Kisan Credit Card Valid ?

A. The validity of KCC is 5 years and can be extended for further 3 years. It sometimes depends on the agricultural activity undertaken.

Q. What is a KCC loan ?

A. It is a short-term financial support provided to farmers, which could be used for various agricultural activities. The borrowing farmers are provided hassle-free loans at concessional rates.

Q. What is the interest rate that is applied on KCC ?

A. The rate of interest depends on the choice of lending bank. But we can observe that the average rate lies at 7% p.a. which could further be reduced by subvention.

Q. What securities are produced as collateral for KCC loans ?

A. For loans up to Rs 1 lakh, hypothecation of crops is required. For loans up to Rs 3 lakhs, additional collateral security may be required by the lending bank.

Q. How can I apply for KCC online ?

A. Various banks are providing the facility to apply for Kisan Credit Cards in their official websites under ‘Agricultural banking’ section.

Q. How is the credit limit on a Kisan Credit Card determined by the lending bank?

A. The credit limit is usually calculated on the basis of:

Type of crops / cropping pattern

Consumption requirements after harvest

Other service fee including insurance premium

Q. In what ways is the KCC scheme beneficial?

A.

Minimum paperwork, hassle-free

Availability at any point of the year

Lower rates of interest

Q. What is the Kisan Credit Card helpline number?

A. The Kisan call centre’s number is 1800-180-1551 (Toll Free)

Read More: