Kisan Vikas Patra (KVP) 2023 - Interest Rates, Benefits, Fee Payment of KVP Post Office Scheme

Updated on June 27, 2024

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

What is Kisan Vikas Patra or Indira Vikas Patra ?

Kisan Vikas Patra is a small savings scheme launched in 1988. It was initiated by the government of India to inculcate a habit of saving for long term goals among rural people. The scheme was originally made for Farmers as the name implies “Kisan Vikas Patra”, but later the scheme was made open for all to invest.

Under this scheme, investments made at a time will be doubled in a specified period. Currently, the scheme promises to double the amount of investment in 124 months (10 years & 4 months) if the investment is initiated in Quarter 1 of FY22 This period of doubling changes as per the interest rate set by the Ministry of Finance in every quarter.

This scheme is suitable for individuals who want to park their surplus money in low risk investments.

Eligibility for Kisan Vikas Patra (KVP) Scheme

Following are the eligibility conditions to make investments in Kisan Vikas Patra KVP:

- Any Indian Resident individual of the age 18 & above is eligible to invest in this scheme.

- Parents or guardians can make investments in this scheme on behalf of a minor or a person of unsound mind.

- NRIs (Non-Resident Indians) and HUFs (Hindu Undivided Families) are not eligible to make investments in this scheme.

Also Read : SBI Bank FD Interest Rates

Types of Kisan Vikas Patra Accounts

There are primarily 3 types of accounts that may be opened for investing in Kisan Vikas Patra. These are:

- Single Account: This type of account is issued to an adult individual for self or on behalf of the minor.

- Joint A Account: This type of KVP account can be opened jointly with a maximum of 3 adults. In this account, all the joint holders are entitled to receive the amount at the maturity of the scheme.

- Joint B Account: This type of KVP account can be opened jointly with a maximum of 3 adults. But only one holder or the survivor will be receiving the amount at the maturity.

Interest Rates for Kisan Vikas Patra (KVP)

Interest Rates are subject to the revisions every quarter by the government. Currently, for Quarter 1 of Financial Year 2021 i.e April 2020 to June 2020 the interest rate applicable is 6.90 % per year, compounded annually.

Read More: Kisan Credit Card Scheme

Following the Current and Historical Interest Rates Offered for Kisan Vikas Patra :

Kisan Vikas Patra Interest Calculator for different Maturities as per historical data

| Financial Year/ Quarters | KVP Interest Rate (compounded annually) | KVP Maturity Period |

| FY 2023(Q1) | 7.5% | 115 months |

| FY 2020-21(Q1) | 6.9% | 124 months |

| FY 2019-20(Q2-Q4) | 7.6% | 113 months |

| FY 2019-20(Q1) | 7.7% | 112 months |

| FY 2018-19(Q3-Q4) | 7.7% | 112 months |

| FY 2018-19(Q1-Q2) | 7.3% | 118 months |

| FY 2017-18(Q4) | 7.3% | 118 months |

Features of Indira Kisan Vikas Patra Scheme

Here are some of the main features of the Kisan Vikas Patra Account:

ACCOUNT

Any Indian Resident above the age of 18 can open a Kisan Vikas Patra or Indira Vikas Patra Account with a post office or any registered bank.

A Joint Account can also be opened with a maximum of 3 adult joint holders

INVESTMENT LIMITS

Only a Lump-sum investment or a single payment is allowed for the deposit in the account.

The minimum amount that can be invested is Rs.1000 and then in multiples of 100. There is no limit on the maximum amount that can be invested.

DISCLOSURE OF DOCUMENTS

To prevent any kind of money laundering activities, the government made it mandatory for individuals investing above Rs.50,000 to present their PAN Card details.

Also, investments of above Rs.10 lacs requires the individuals to disclose their income sources.

RETURNS

The returns or interest rates on this scheme have been designed in such a way that it would double your investments in a specified period. Investments made in the current Quarter of April to June will fetch 6.9% interest compounded annually and therefore, doubling the investment in 124 months.

If no withdrawal has been made after the maturity of the scheme, then the Post office savings rate at simple interest will be accrued to the amount payable but for a maximum period of 3 years.

KISAN VIKAS PATRA MATURITY

The maturity period of the Kisan Vikas Patra yojana is subject to revisions by the government of India. Currently, the maturity period is 124 months with the KVP interest rate at 6.90% for Quarter 1 of FY 2020-21.

Read More: Sukanya Samriddhi Yojana

RISKS

The scheme has negligible or no risk as it comes with the guarantee of the Government of India on the safety of capital and the return on investment. Therefore, this makes the scheme one of the safest investment options for meeting long term goals.

Kisan Vikas Patra Tax Benefits

The amount invested in the scheme as well as the return generated, are not eligible for any kind of tax deductions under section 80C or other sections.

Withdrawals after the maturity are exempted from TDS (Tax Deducted at Source).

Transfer from one to another account

The Kisan Vikas Patra account can be transferred from one post office branch to another post office branch and even from one post office branch to the individual’s account at the registered Bank Branch & vice-a-versa.

One can make the transfer request in their bank or post office branch by filling up the required details in Form B.

Also, the Account is transferable from one person to the other as per the specified conditions by the branch.

Kisan Vikas Patra Withdrawal Rules

The maturity of the scheme is as specified (currently 124 months). If the individual wants to encash the investment before the maturity period, these are the rules depending upon the time at which withdrawal is made:

- Within 1 year- No interest will be paid, and the investor would be required to pay some penalties.

- 1 Year to 2.5 Years- Interests will be calculated at the lower rates and no penalties will be imposed.

- After 2.5 Years- 2.5 Years is the Lock-in period of the scheme, any withdrawal made after 2.5 years will not result in any interest cuts or penalties.

Nomination Criteria

The Kisan Vikas Patra yojana gives the facility to the investor to name the nominee who will be entitled to the payable amount in the event of the death of the holder. The individual can name the nominee at the time of purchase of the KVP certificate or any time during the duration of the scheme by filling the necessary & required details in Form C.

The holders also have the option to cancel or make variations in the nomination details by submitting Form D.

Also Read : Axis Bank FD Interest Rates

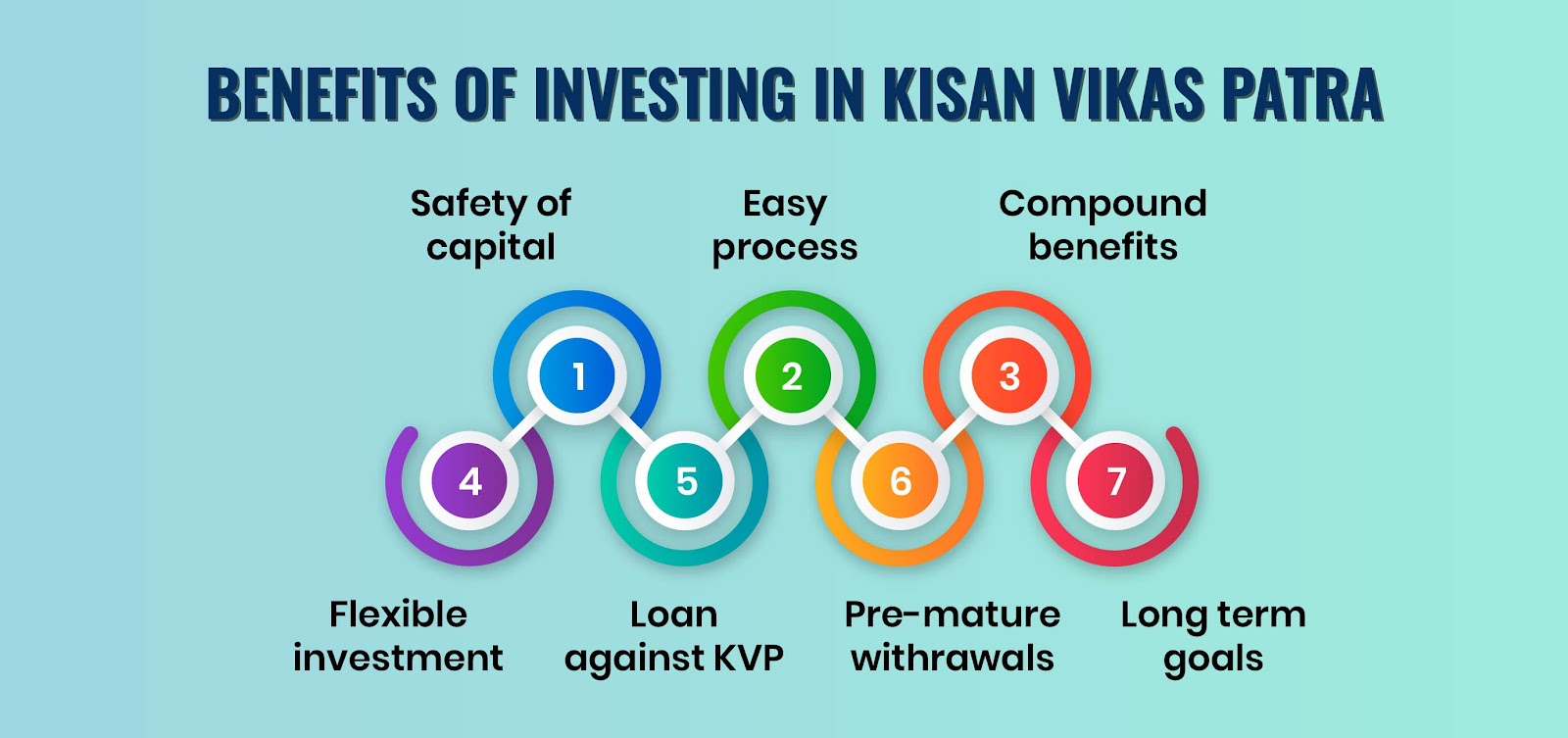

Kisan Vikas Patra Benefits

Investing in KVP offers several benefits to the investors. Some of them are:

Safety of Capital

The scheme provides the advantage of safety of capital and the interest or returns amount because of the guarantee of the government of India. So, it is a risk-free investment one can make for the long term.

FLEXIBILITY OF INVESTMENT

Investment in KVP provides flexibility to the investors as one can invest with as low as Rs. 1000 and after that in multiples of Rs.100. So, it appeals to every kind of investor including small or big by the way of allowing them to invest any size as per their will.

EASY PROCESS

It is a very easy and quick process to make an investment in KVP. The scheme involves an easy & minimal documentation process along with providing the benefit to investors to open an account with their nearest post office branch or registered bank’s branch.

With more than 1.54 lakh post offices across the country, it becomes accessible to investors in every corner of the country.

Read More: Best Post Office Saving Schemes

LOAN AGAINST KVP

One more attractive benefit of investing in Kisan Vikas Patra is that one can avail loans personal or business loans against collateralizing the KVP Certificate.

Also, the loans taken against Kisan Vikas Patra offers the borrowers attractive rates of interest.

COMPOUNDING BENEFITS

The interest earned on the Kisan Vikas Patra certificate is compounded annually, so it brings higher returns to the investors. Investors earn more return by the way of also earning interest on interests.

PRE-MATURE WITHDRAWALS ALLOWED

The tenure of the scheme is generally large, as it is currently at 124 months. However, the investor has the facility to withdraw or encase before maturity. Pre-mature withdrawals are allowed under the scheme with some charges or penalties if done before 2.5 years and no charges after 2.5 years.

So, an individual can withdraw his investment any time as per his needs.

LONG TERM GOALS

As the investment in KVP has a long tenure of maturity, it helps in preparing for long term goals and making the future financially secure.

Cons of Investing in Indira Vikas Patra

Along with the benefits, there are always some cons associated with any investment. Some of the cons in case of investments in KVP are highlighted below:

NO TAXATION BENEFITS

The scheme does not offer any tax benefits related to any tax deductions on the investment amount or the interest. No tax benefits on the scheme make it relatively less attractive to the other similar small saving schemes.

This makes it not suitable for people looking for tax benefits and they might opt for investments in 5-Year tax-saving Fixed deposit, PPF (Public Provident Fund), National Saving Certificate etc. If the investor is willing to take some risks for higher returns along with tax benefits, then one may also consider investing in an ELSS (Equity Linked Saving Schemes) or Tax-saving mutual fund.

Also Read: Difference Between ELSS vs PPF

LOWER RETURNS

As regards to returns, Investments made for such a long period in other investment products such as mutual funds, stocks have the capability to generate much higher returns than the KVP.

The effective returns from the scheme become even lower when taxes are deducted on the investment and return amount.

NO ONLINE INVESTMENT

The scheme does not offer the option to make an online investment. The individual is required to physically reach his nearest branch office and fulfil the necessary document-related verification requirements.

Also Read : HDFC Bank FD Interest Rates

Who should invest in Kisan Vikas Patra ?

Kisan Vikas Patra, being a government-backed investment product carries the sovereign guarantee of the government on the investments made by the investors. No chances of default on investments make this product suitable for risk-averse investors who do not want to take risks while investing.

Also, KVP is a long tenure investment scheme and is therefore suitable for people who want to achieve their long term financial goals with earning risk-free returns on the investment made.

How to Invest in Kisan Vikas Patra?

One can open a Kisan Vikas Patra Account with any of the registered providers like Banks or Post Office. The investor or depositor can directly go to the bank branch or post office and fill up Form A for enrolling in the scheme. In case the application is being made through an agent then he will fill the same form.

Also, there is an option to download the form online from the bank’s websites and post office website. The individual can take a print of the downloaded form, fill it and can submit in the branch at which they want to open the account.

Along with the form, the individual must submit the following self-attested documents:

- Passport size photographs

- Pan Card in case when investments are above Rs.50,000.

- Identity proof, age proof, and address proof (Aadhaar card, birth certificate, driving license, telephone bill, voter ID, senior citizen card, passport). Any one of the documents for each proof required.

- Income Proof (ITR, Bank Statement, or any other) for investments above Rs.10 Lacs is mandatory.

Payment modes for KVP

- Cash

- Cheque, Demand draft or Pay order.

Banks offering KVP Schemes

There are many Banks offering the scheme or Account along with the Post offices. Some of the banks are:

- State Bank of India (SBI) KVP

- Bank of Baroda KVP

- Axis Bank KVP

- Union Bank of India KVP

And others including all the post office branches across India.

Read More: What is Arogya Sanjeevani Policy

KVP Form

There are two modes to apply for the Kisan Vikas Patra.

- Download the form online, fill it, and then submit it to your nearest post office.

- Directly visit the nearest post office and then request for a form, fill the required details, and then submit it.

Click here to download the Online Application Form.

How to transfer KVP online?

The Kisan Vikas Patra account can be transferred from one post office branch to another post office branch and even from one post office branch to the individual’s account at the registered Bank Branch & vice-a-versa.

- Transfer from one post office branch to another post office branch.

One can make the transfer request in their bank or post office branch by filling up the required details in Form B. Along with the form, the following documents are also required:

Documents required for KVP Transfer

- Filled Form B (Click here to download)

- Identification documents like Aadhar Card, Driving License, Voter ID, passport, or any other identification document.

- Residence proof document like Aadhar Card, Driving License, Voter ID, passport, Telephone Bill, or any other residence proof document.

- Original kisan vikas patra certificate.

- Pan card.

- The Account is transferable from one person to the other as per the following conditions by the branch.

- The individual should be an Indian CItizen and should be eligible for KVP.

- The transfer should be as per the orders of the court of law.

- On the death of the holder, the transfer should be done in the name of the nominee or the legal heir.

- If the KVP holder is a minor, then the certificate is not transferable.

Form B should be filled for transfer and after getting the request, the new holder will be issued a new KVP certificate bearing the same dates.

Comparison of Fixed Deposits with Kisan Vikas Patra

Fixed Deposits are the time deposit with the banks, post offices, or financial institutions for pre-defined tenures of days to years. This is also one of the safest forms of investing as there is a very low risk associated with making deposits with the banks and the good rated financial institutions.

Investment Limits

Fixed Deposit Scheme’s requirement for minimum investment amount varies across institutions and the minimum amount required to make FD with the post office or a bank is Rs.1000. There is no upper limit for maximum investment.

The minimum amount required for investment in KVP is the same as in FDs and there is no upper limit for investment.

Returns

Different banks & financial institutions offer varied returns on deposits and are generally in the range of 6-7% for Fixed Deposit depending upon the tenure of deposits. Bajaj Finance, an NBFC offers the highest returns of up to 7.85% on Fixed Deposits.

The interest rate offered on Kisan Vikas Patra for the investments made in the current quarter i.e April to June, FY2021 is 6.9%.

Maturity

Fixed Deposits can be made for any tenure i.e days to years depending upon the requirements of the depositor. However, Tax-Saving Fixed Deposits come with the lock-in period & maturity of 5 years.

Whereas in KVP, there is a pre-defined maturity for the investment (124 months for Current Qtr.).

Withdrawals

Premature withdrawals can be made on bank FDs by paying the mandatory penalty charges as specified. Also, there are financial institutions that offer free premature withdrawals from the FD.

In Kisan Vikas Patra, Premature encashments are allowed after the completion of the lock-in period of 2.5 years without any costs. For withdrawals within 1 year of the issue, the Individuals need to pay mandatory penalty charges and for encashments after 1 year but before 2.5 years, the depositor would have to withdraw at lower interest rates.

Taxation benefits

Fixed Deposits with Banks, Post Office, or Financial Institutions do not offer any taxation benefits for the deposit made. However, there is a Tax-saving Fixed Deposit which comes with a minimum lock-in period of 5 years and offers taxation benefits by the way of allowing to claim tax deductions of up to Rs. 1.5 lacs in a financial year by the depositor under section 80C of Income Tax Act,1961.

Whereas, Kisan Vikas Patra does not offer any kind of tax benefits to its investors.

Comparison of National Savings Certificate with Kisan Vikas Patra

National Savings Certificate is a government-backed small saving scheme made to encourage investments by individuals with lower levels of income. The scheme offers the sovereign guarantee on the amount of investment as well as interest earned. The scheme allows to make a lump-sum investment which will be payable along with the interest earned at the fixed maturity of the scheme i.e 5 years from the date of issue.

Investment Limits

National Savings Certificate & Kisan Vikas Patra, both have the same requirement with respect to the minimum & maximum investments i.e the minimum amount required for investment is Rs.1,000 and there is no upper limit for investment.

Returns

National Savings Certificate offers the interest rate of 6.8% which is compounded annually.

Whereas, KVP offers an interest rate of 6.9% for the current quarter which would mean the investment amount will be doubled in 124 months.

Maturity

National Savings Certificate has a fixed maturity period of 5 years whereas the Kisan Vikas Patra has a maturity period of 124 months or 10 Years 4 months ( for the investments made in Q1 of FY2021) for the investments.

The maturity period of the KVP is subject to revisions every quarter by the Ministry of Finance.

Withdrawals

National Savings Certificate comes with a lock-in period of 5 years. Premature withdrawals are generally restricted & are possible in case of death of the account holder, by the law court order or others as specified.

In Kisan Vikas Patra, Premature withdrawals are allowed after the completion of the lock-in period of 2.5 years without any costs. For withdrawals before the completion of lock-in, the individual needs to pay the mandatory charges or suffer interest rate cuts according to the tenure.

Taxation benefits

Investments in National Savings Certificate are allowed for claiming tax deductions of up to Rs.1.5 lacs under section 80c of IT Act,1961 in a financial year.

Whereas, Kisan Vikas Patra Investments does not offer any tax benefits.

FAQs - Kisan Vikas Patra Post Office Scheme

Q. What is the interest rate of kisan vikas patra ?

A. The latest Kisan Vikas Patra interest rate 2022 is 6.9% for the current quarter April-June of the Financial Year 2022. The interest will be compounded annually. The kisan vikas patra post office scheme as per the current rates will double the amount of investment in 124 months i.e 10 years & 4 months.

Q. How to find the kisan vikas patra calculator ?

A. The calculator for kisan vikas patra online is available on this webpage. Below we have mentioned the maturity period of kisan vikas patra post office in months against the interest rates as per the latest updated rates by the Government of India.

Kisan Vikas Patra Calculator

| Financial Year | KVP Interest Rate (interest compounded annually) | KVP Maturity Period in months |

| FY 2023(Q1) | 7.5% | 115 months |

| FY 2022-23 (Q1) | 7.2% | 124 months |

| FY 2021-22(Q1-Q4) | 6.9% | 124 months |

| FY 2020-21(Q1-Q4) | 6.9% | 124 months |

| FY 2019-20(Q2-Q4) | 7.6% | 113 months |

| FY 2019-20(Q1) | 7.7% | 112 months |

| FY 2018-19(Q3-Q4) | 7.7% | 112 months |

| FY 2018-19(Q1-Q2) | 7.3% | 118 months |

Q. What is the KVP maturity period ?

A. The maturity period of Kisan Vikas Patra or Indira Vikas Patra for the current quarter of April to June 2022 is 124 months with an interest rate of 6.90%.

Q. What is the Kisan Vikas Patra Post office scheme ?

A. The KVP Post Office scheme is a small savings scheme launched by IndiaPost in 1988. The scheme was specifically designed for framers in rural areas to promote and inculcate within them the habit of saving for long term goals. Later, it was open to all.

The scheme promises to double the investment amount on the purchase of the Vikas Patra in a specified time period.

Q. Can I purchase the Kisan Vikas Patra Online ?

A. No, you cannot purchase the Kisan Vikas Patra online. However, you can download the form from the post office or registered Banks like State Bank of India or Union Bank’s website. You would need to take a print, fill and submit the form physically in the nearest branch.

Q. What is the KVP maturity period?

A. The maturity period of Kisan Vikas Patra or Indira Vikas Patra for the current quarter of April to June 2020 is 124 months with an interest rate of 6.90%.

Q. What is the minimum investment for KVP?

A. The minimum amount required to invest in Kisan Patra is Rs.1000 and in multiples of Rs.100 thereafter. There is no limit on the maximum amount of investment.

Q. What is the lock-in period of Kisan Vikas Patra?

A. The minimum lock-in period of Kisan Vikas Patra is 2.5 years. Any withdrawals before the lock-in period will result in interest rate cuts or penalties on investment amount as specified for the time periods.

Q. Is Kisan Vikas Patra Transferable?

A. Yes, the KVP can be transferred from one person to another, from one post office branch to another or to a bank branch. The request for transfer can be made by the holder by filling Form B.

Q. What are the tax benefits of the KVP Post office scheme?

A. There are no tax benefits on the purchase or investment in Kisan vikas Patra. There are no deductions allowed under the section 80C.

For Tax saving purposes, one can look at investing in National Savings Certificates, Tax-saving Fixed Deposits, PPF or other options.

Q. What happens if my KVP certificate is lost?

A. If your certificate is lost, you can easily apply for the duplicate copy of the Vikas Patra by filling Form NC29 at the branch. You just need to remember the details of the certificate number, maturity date, and a photocopy of the original certificate if required.

Q. Do banks also offer Kisan Vikas Patra?

A. Yes, you can purchase the Kisan Vikas Patra from Banks registered to provide KVP certificates. Some of the banks providing this services are SBI, Union Bank, Bank of Baroda, Axis bank etc

Q. What are the documents required for investing in KVP?

A. While purchasing the Kisan Vikas Patra Certificate along with filling the application form, the individual also needs to submit copies of some self-attested documents for verification purposes. The documents are:

- Passport size photograph

- Identity Proof, Address Proof (Adhaar Card, driving license, Birth certificate or voter ID and others)

- Pan Card Proof is mandatory for all investments above Rs.50,000.

- Income Proof (ITR, Bank Statement etc.) is mandatory for investments above Rs.10 Lacs.

Q. Can I withdraw my investments before the maturity period?

A. Yes, the investors can withdraw their investment amount after the completion of the lock-in period of 2.5 years from the date of issue.

For withdrawals before 2.5 years, the Individuals need to pay penalties or suffer interest rate cuts as per the specified conditions for different tenures.

Q. What are the benefits of investing in Kisan Vikas Patra?

A. There are many benefits associated with investing in Kisan Vikas Patra. Some of them are:

- It is one of the safest investment options for the investors because of being backed by the government of India.

- The scheme helps to achieve long term financial goals of the investors.

- The scheme allows the investors to use KV Patra as a collateral for getting loans.Also, the lenders including banks charge lower rates on loans from the investors.

- The scheme allows zero cost withdrawals or encashments by investors after the completion of lock-in period i.e 2.5 years. Withdrawals can also be made before the lock-in however, the investors would have to pay the required penalties or suffer rate cuts.

Q. What are the other investment options similar to Kisan Patra?

A. There are many other investment options available to investors providing similar returns or characteristics, some of them are:

- National Savings Certificate

- Fixed Deposits with banks, post office or financial institutions

Schemes for Regular Income on Lump-sum Investments:

- Post Office Monthly Income Saving Scheme.

- Non-Cumulative Option in Bajaj Finance Fixed Deposit.

- Senior Citizens Savings Scheme exclusively for senior citizens.

Q. What are the Investment Options for earning higher returns than the Kisan Vikas Patra?

A. Kisan Vikas Patra being a government-backed scheme is one of the safest investment options available to the investors. However, it provides lower returns & does not offer any kind of tax benefits leading to lower post-tax returns.

Investors can look into investing in the following products as per their risk appetite and requirements.

- Debt Mutual funds

- ELSS Funds (Tax-Saving Mutual Funds)

- Equity Mutual Funds

- Equity Shares

All of the mentioned investment options carry different risk-return characteristics and are therefore suitable to the investors as per their risk profile & financial needs.

Q. How to encash Kisan Vikas Patra after maturity?

A. Kisan Vikas Patra can be encashed after maturity. You need to visit the post office or bank from where you have purchased the Kisan Vikas Patra certificate. From there you need to get the closure application form, fill it, and then submit it. It is suggested to carry your identification document or identity slip which was issued at the time of the purchase.

Q. How to calculate Income Tax on Kisan Vikas Patra?

A. Interest earned on the KVP is not subject to Tax Deducted at Source. KVP interest is taxed as per the individual tax slab under the Income Tax Act. Investments in KVP are not eligible under Section 80C of the IT Act for tax deductions.

Q. Can an NRI invest in Kisan Vikas Patra ?

A. No, NRIs are not eligible to invest in the Kisan Vikas Patra.

Q. Is interest earned on Kisan Vikas Patra taxable ?

A. Yes, the interest earned from KVP is taxable under the Income Tax Act,1961.

Q Does Kisan Vikas Patra come under section 80C of Income Tax?

A. No, Investment in Kisan Vikas Patra is not eligible for claiming tax deductions under section 80C of the Income Tax Act,1961. Interest earned on KVP is taxable and it is not a tax-saving instrument.

Read More:

Unit Linked Insurance Plans

How to become a Mutual Fund Advisor

National Pension Scheme

Post Office Time Deposit