Best Liquid Funds : Check Liquid Mutual Funds Return & Benefit

Updated on June 27, 2024

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

Looking for the best mutual fund and thinking about which mutual fund to invest in. If you're searching for a short-term investment plan with low-risk ability, then it’s a sure answer to your questions. Here you have a quality fund to invest in. A fund in which you invest into debt funds in which all your criteria are fulfilled, and this could be a great suit for you.

What are liquid Mutual funds?

Liquid funds are those debt funds that lend up to a period of ninety-one days. These funds have the least risk among all the different types of mutual fund categories. Liquid funds have an excessively low lending period. In this kind of mutual funds scheme, most cases, they may be debt and cash market instruments, which consist of non-public and authorities bonds, debentures, certificates of deposit, industrial papers, treasury payments, and many others.

Most of these fixed deposits are held until maturity, and the shorter period of the underlying deposit makes the liquid funds ability to supply profits much less complex. Therefore, even conservative buyers consider liquid funds to be a desirable quick-time investment option. However, the returns from these mutual fund schemes are not assured and rely upon the overall performance of the financial credit score and cash markets.

Features of Liquid Funds

Here are the important features of liquid funds that assist you in making an informed funding decision.

- Short-Term Investment: Liquid funds provide a convenient option for short-term investments. This is ideal for keeping your funds easily accessible in your bank account, making it a preferred choice for business owners who want to invest surplus funds temporarily.

- Quick Access to Funds: With a liquid savings account, you can withdraw your money as soon as the day after you deposit it. This means you can enjoy the returns on your investment almost immediately.

- Bank-Like Liquidity: Liquid funds function similarly to a traditional bank account, offering high liquidity. When you make a withdrawal, the funds are typically credited to your account the very next day.

- Stable Returns: Liquid funds are known for their stability and minimal fluctuations. Additionally, the fund's maturity aligns with your investment period to optimize returns.

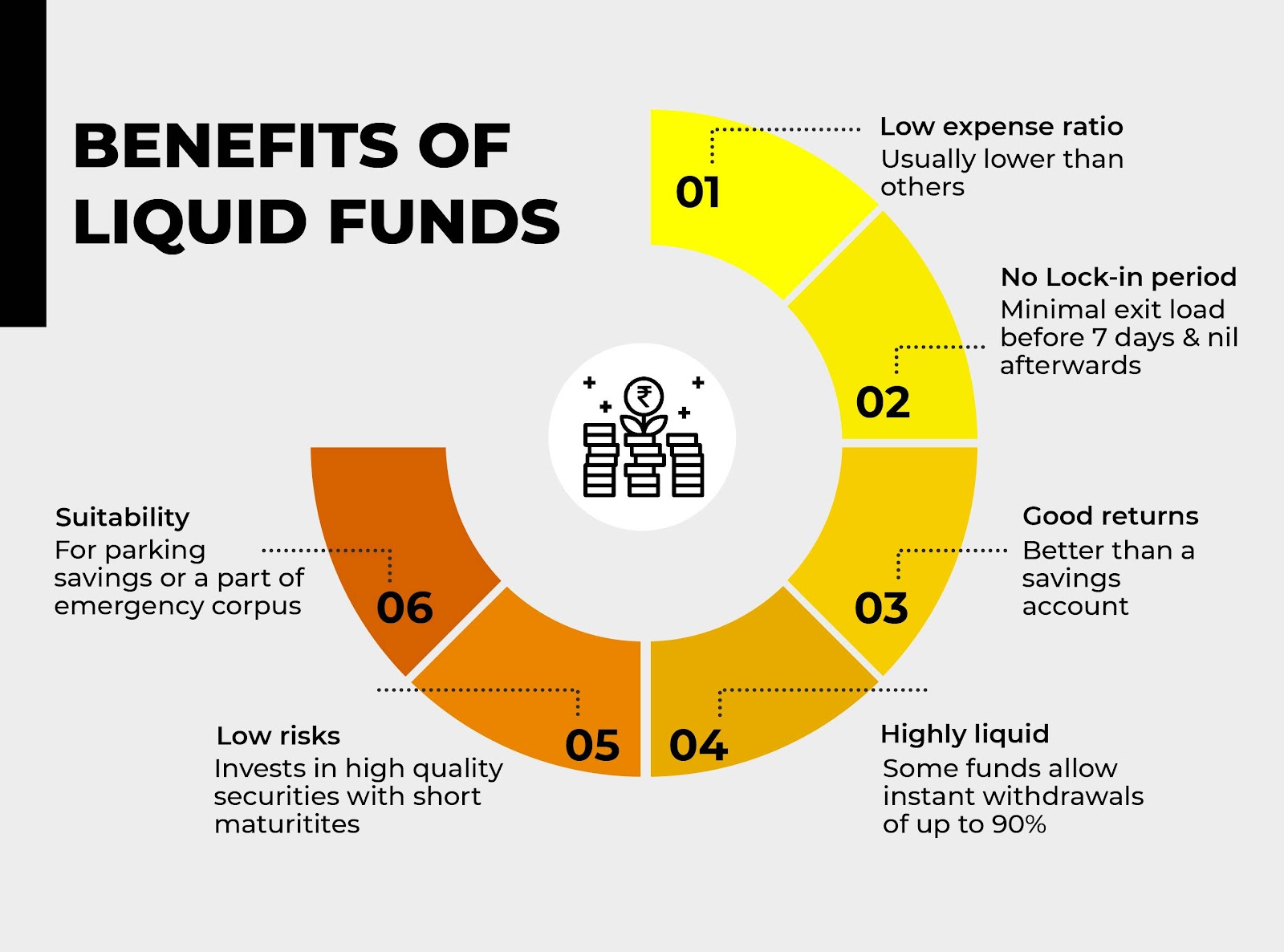

Advantages of liquid funds

Liquid funds are a safer and more secure way to evaluate surplus funds in comparison to their counterparts. The top mutual fund preserves greater advantages for the investor and provides the best funding.

The benefits of mutual funds are indexed below:

➥ Fixed Returns: In the liquid funds, invest in units that yield fixed interest charges, so the returns, investor gets from them are also constant. While maturing, the investor would get a return on the essentials invested and earned.

➥ Low Risk: Liquid Funds pose a low threat due to the motives discussed below. The chance of decreased interest costs converting due to higher liquidity and decreased maturities. With the simplest adulthood of ninety-one days, the mutual fund NAV of the underlying asset does not change appreciably. The credit score chance or the chance of non-price of most important and hobby is likewise much lower with those mutual funds.

➥ Liquidity: The units in which the fund invests have high liquidity because of their quick length. An investor may want to withdraw the investment at any time. Withdrawal requests are processed within 24 hours of the request. There is no time limit on this funding.

➥ Higher returns: Liquid funds offer higher returns in comparison to their opposite numbers, i.e, banking gadget (financial institution account) balances and easy investments, while their opposite numbers provide yields of 4% to 5%, while these mutual funds have traditionally provided over 7%. Due to the above advantages, liquid funds have gained popularity among retail traders in recent years.

➥ Exit load: Unlike constant deposits and other mutual funds where there is no go-out load, it applies to liquid funds. No exit load is charged if the deposit is withdrawn after 7 days of deposit.

Best-performing Liquid Mutual Fund funds to Invest In 2023

| Fund Name | Expense ratio | 3 Yr Return (%) |

| IDBI Liquid Fund | 0.17% | 4.55% |

| Tata Liquid Fund - Regular Plan | 0.32% | 4.54% |

| Baroda Liquid Fund | 0.29% | 4.64% |

| Axis Liquid Fund | 0.24% | 4.63% |

| Aditya Birla Liquid Fund | 0.34% | 4.61% |

| Sbi Liquid Fund | 0.3% | 4.56% |

| Nippon India Liquid fund | 0.34% | 4.55% |

| ICICI Prudential Liquid fund | 0.29% | 4.55% |

| Kotak Liquid Fund | 0.32% | 4.54% |

| HDFC Liquid Fund | 0.3% | 4.54% |

How do liquid funds work?

The investment objective of liquid mutual funds is to maintain capital and generate income for investors. Consequently, the fund manager invests in awesome debt securities and ensures that the average adulthood of the scheme fund does not exceed ninety-one days. This brief duration ensures that the liquid fund is not vulnerable to interest charge adjustments. The best liquid funds constantly suit the maturity of their portfolios.

Moreover, as per the trendy SEBI pointers, liquid funds can be used to spend money on indexed commercial papers. In addition, this policy may have a trendy restriction of 25% consistent with the website. In addition, mutual funds should preserve at least 20% of their property in liquid gadgets, which include cash market prices, coins, and cash equivalents.

Read More: Best Performing SIP Plans for 5 Years

Liquid funds risks

Given that liquid funds make investments in debt securities, the following are the major risks that a debt fund is exposed to:

1. Liquidity Risk: Liquidity risk is the risk associated with not being able to convert the securities or funds into cash at the required time.

As per SEBI requirements, liquid funds have to mandatorily invest in highly liquid debt securities that carry short maturities. This enables the liquid funds to be exposed to zero or negligible liquidity risks. Along with that from an investor’s perspective, the liquid funds allow quick and instant withdrawals on redemption requests which makes them a highly liquid asset.

2. Credit Risk: Credit risk is the risk associated with the defaults from the issuer on its interest or principal repayment obligations.

These liquid funds need to mandatorily make investments in high-credit quality securities including those issued by government & corporates as well which ensures that there are very low risks associated with defaults in these funds. However, there might be some funds that would have taken undue credit risks for generating extra returns. So, investors should always look at the portfolio of a liquid fund before making any investments to avoid facing credit risks.

3. Interest Rate Risk: Interest Rate risks are the risks associated with the fluctuations in the returns or NAV of the fund in response to the interest rate movements in the market.

Liquid funds are also exposed to interest rate risks but to a very low extent when compared to other funds. Due to their low durations & maturities, the impact of interest rate movements on the fund is very low. The liquid funds follow the accrual-based strategy while investing which means they aim to earn fixed coupons from the underlying debt securities and also buy and hold the securities until maturity and therefore are less impacted by the interest rate movements.

Also Read:

How much return can you anticipate from a liquid fund?

As liquid funds spend money on gadgets maturing in 91 days, their returns are lower than those of debt funds, which invest in longer-term instruments inclusive of brief-term fairness, short-term price ranges, equities at very quick intervals, and so forth. However, such liquid fund returns normally rise above the overnight quotes of single-day investments in overnight funds. In regular instances, liquid funds income is likely to exceed the hobby on your financial institution account. That’s why your excess cash in a low-yielding financial institution account is constructed with liquid funds.

Read More: Best SIP Plans to Invest in for 10 Years

Liquid Fund - Benefits

Who can invest in liquid funds?

➥ Investment Horizon: As banks put money into securities with shorter maturities, liquid funds are nice for investors with funding maturities of up to 3 months; however, long-term investors can opt for longer-term, like 6 months or a year.

➥ Higher hobby charges than financial savings accounts: Individual investors if mutual funds advantage from a liquid fund via excessive volatility and robust interest fees Efficient price ranges are used to maintain susceptible finances if they're kept with clean withdrawals.

➥ Contingency Funds: Liquid funds are top-notch options to keep your contingency corpus or emergency fund separate. This creates safety to maintain cash safety as the inventory marketplace itself is much less unstable and more volatile. In addition to this, you can additionally play them whenever you want.

➥ Short-term Investments: High-performance liquid funds are designed in a manner that allows you to invest the cash and earn steady and constant returns. Thus, investors can also choose to invest their capital in a liquid fund until they decide how and where to invest the corpus.

Read More: Best SIP Plans for 1000 per month

Read More: Types of Mutual Fund Schemes in India

How do I invest in the best liquid funds?

➥ Historical Returns: While past returns are no guarantee of future returns, they're an excellent indicator of understanding a financial institution’s performance. See if the fund has continually achieved nicely over the years and outperformed its benchmark square returns. If it has done well inside and beyond, the financial institution is expected to perform similarly nicely in the future. Before investing in liquid funds, one should also take a look at the past report from the AMC.

➥ Credit Rating: It is critical to test the credit score rankings assigned to the underlying assessments. Higher credit ratings make sure there is much less credit chance. Credit risk is a chance for the safety company. misses the most important or interest payments. The maximum rating assigned to any security is AAA, which offers it a first-rate credit score.

➥The average maturity of the portfolio is: Find the common boom price for the portfolio. It is quality to invest in a liquid budget with a mean period of three months or much less. Short-term maturities make sure that the portfolio does not range excessively due to lengthy-term adjustments in interest fees.

➥ Expense ratio: Choose a low-fee liquid financial institution. Lower spending will increase gross income.

➥ Fund Objective: Choose from a growth chart, day-by-day dividend, weekly dividend, and monthly dividend schedule that fits your risk appetite and funding dreams.

When to invest in liquid funds?

Investors can invest in liquid securities in subsequent instances. When investors have an excess amount of cash to invest.

- When investors have a short-term objective of three months of publicity. When investors don’t realize it after they wish for money, liquid funding is the first-rate option for them to invest.

- When an investor wants to invest the extra in equity but wants to use it as an SIP,you can also invest in Daily SIPs( the only investment plan that helps you invest systematically and on a daily basis i.e. daily SIP plan), This option is exclusively available only at Zfunds.

- The investor can then make a lump-sum deposit into the liquid fund and then deposit STP into the fund.

- Another famous investment alternative is to keep an emergency fund with residing charges for up to 6 months. Investors can invest their emergency price range in liquid funds and earn new benefits.

Taxation on a liquid budget

Liquid funds are assessed for tax functions as follows:

Short-Term Capital Gains (STCG): If the investment is less than three years, the fast-time period capital profits are protected in the taxable profits of the funding and taxed as in step with the profits tax slab fee. It is blanketed in their taxable income, and the investor is taxed for this reason.

Long-term profits (LTCG): Long-term gains on investments after 3 years are taxed at 20%, which includes indexation profits. From April 1, 2023, tax on debt funds ought to be taxed on the investor’s IT slab charge, regardless of the holding length. Therefore, there will be no LTCG benefit to the debt budget.

How to Invest in Liquid Funds via ZFunds?

Looking for the best mutual fund app in India to boost your finances? To be able to invest with Zfunds, you must first be able to invest in boom funds. Follow those steps and invest today in increasing your finances:

- Step 1: Log in to the Zfunds app.

- Step 2: Zfunds has curated portfolios for investors to meet multiple needs. For such funds, Zfunds provides the best mutual funds to invest in. They help you invest and allow you to build the best portfolio to invest in.

- Step 3: Review fund recommendations and continue

- Step 4: Provide contact details and date of birth.

- Step 5: Provide PAN details and complete e-KYC.

- Step 6: Decide how much to invest in the portfolio and invest in it.

- Step 7: Set up your auto debit and now you have invested in the desired fund.

When looking for a short-term investing alternative, those with extra money might consider liquid mutual funds as the best investment option. It is also perfect for companies looking for a simple approach to monitor their cash flow.

Frequently Asked Questions

Q. What are liquid funds?

A. Liquid funds are the debt funds that invest in high-quality debt instruments. The debt instrument in which the liquid funds invest has a maximum maturity of 91 days. Investments in debt securities like government bonds, commercial papers, T-bills, etc. make liquid funds less risky and a highly liquid investment.

Q. What is the benefit of liquid funds?

A. Liquid funds have very low risk associated with them because of their investments in high-quality debt securities. These funds have the capability to generate more returns than a typical savings bank account.

Q. Are liquid funds better than savings accounts?

A. Liquid funds are better than savings accounts as they have the potential to offer better returns to investors. Moreover, just like savings accounts these funds also offer high liquidity to investors. In some cases, there are funds that provide an instant redemption facility to investors wherein they can withdraw up to 90% (Max. 50,000) of their account balance every day into their linked bank account instantly.

Q. How are liquid funds taxed?

A. Liquid funds are taxed like debt mutual funds as the investments are done in debt instruments. Units redeemed within a period of 36 months will be taxed as STCG (Short Term Capital Gains). In this case, gains will be added to the income and taxed as per the income tax slab. The units redeemed after a period of 36 months will be taxed as LTCG (Long Term Capital Gains) at a rate of 20% after the benefit of indexation.

Q. Is there any lock-in period in the liquid funds?

A. As the name suggests, liquid funds offer high liquidity to their investors so they do not have any lock-in period. Investors can redeem their units anytime from the fund. Though there are minimal exit loads on withdrawals up to 7 days from the date of investment.

Q. Can SIP investment be done in liquid funds?

A. Yes, liquid funds also offer the SIP method of investment.

More Information:

What is SEBI

Rupee Cost Averaging in SIP

Bharat Bond ETF

Shariah Compliant Mutual Funds

Best Large Cap Mutual Funds to Invest in India

Best Small Cap Mutual Funds to Invest in India

Best Multi Cap Mutual Funds to Invest in India

Best ELSS Mutual Funds to Invest in India