National Pension Scheme (NPS )- Tax Benefits, Eligibility, Features, How to Open, Application Form

Updated on June 27, 2024

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

What is National Pension Scheme ?

Pension plans help the retirees to manage their expenditures by providing regular income after retirement. Planning for retirement is an essential part of the individual’s financial planning even from an early age so as to ensure building a corpus sufficient to meet the expenditures after the requirement along with carrying the current lifestyle in the future.

To provide an architecture ensuring systematic planning for the pension & retirement needs of the citizens, the Government of India launched the “National Pension Scheme” which is also known as National Pension System in the year 2004. The scheme was initially available exclusively for the government employees joining after the launch of the scheme. However, later the scheme was made open for all the citizens in the country including employees working in the private sector as well as in the unorganized sector. The scheme is being regulated by the Pension Fund Regulatory and Development Authority (PFRDA), an authority that is set-up by the government to ensure transparency & efficient working of the pension fund schemes.

Under the scheme, the individuals or employees make contributions to the NPS account of the minimum deposits of Rs.1000 in a financial year till retirement from the job. The central government employees need to make contributions of 10% of the basic salary(and a contribution of 14% is made by the central govt) every month into the NPS account. The deposited amount then will be used for making the investment in various instruments like equity stocks, corporate debt securities, or Government bonds to generate returns for the investors.

At the maturity of the scheme i.e at the time of retirement, the individual can make a lump sum withdrawal of up to 60% of the total corpus and the rest i.e at least 40% of the corpus needs to be mandatorily utilized in purchasing the annuity scheme from government-approved annuity providers which will provide regular pensions to the annuity account holder.

Read More: Best Tips to invest in Mutual Funds

ELIGIBILITY OF National Pension Scheme (NPS)

The eligibility conditions of an individual for enrolling into the NPS scheme are as follows:

- Any Indian citizen including NRIs(Non-Resident Indians) are eligible to enroll in the scheme.

- The individual of the age 18-65 can apply for joining the NPS scheme.

- OCI(Overseas Citizens of India), PIO holders(Person of Indian Origin)& HUFs are not eligible to join the NPS scheme.

- Only one account is allowed, the individuals are not allowed to open multiple NPS accounts.

- The NPS account can be opened individually, no joint holding accounts are allowed.

- The individual is allowed to open the Tier-2 account only if he holds the Tier-1 account in NPS.

- The applicant should be KYC(Know Your Customer) compliant as per the requirements in the Subscriber Registration Form. Also, the applicant needs to submit the required mandatory documents.

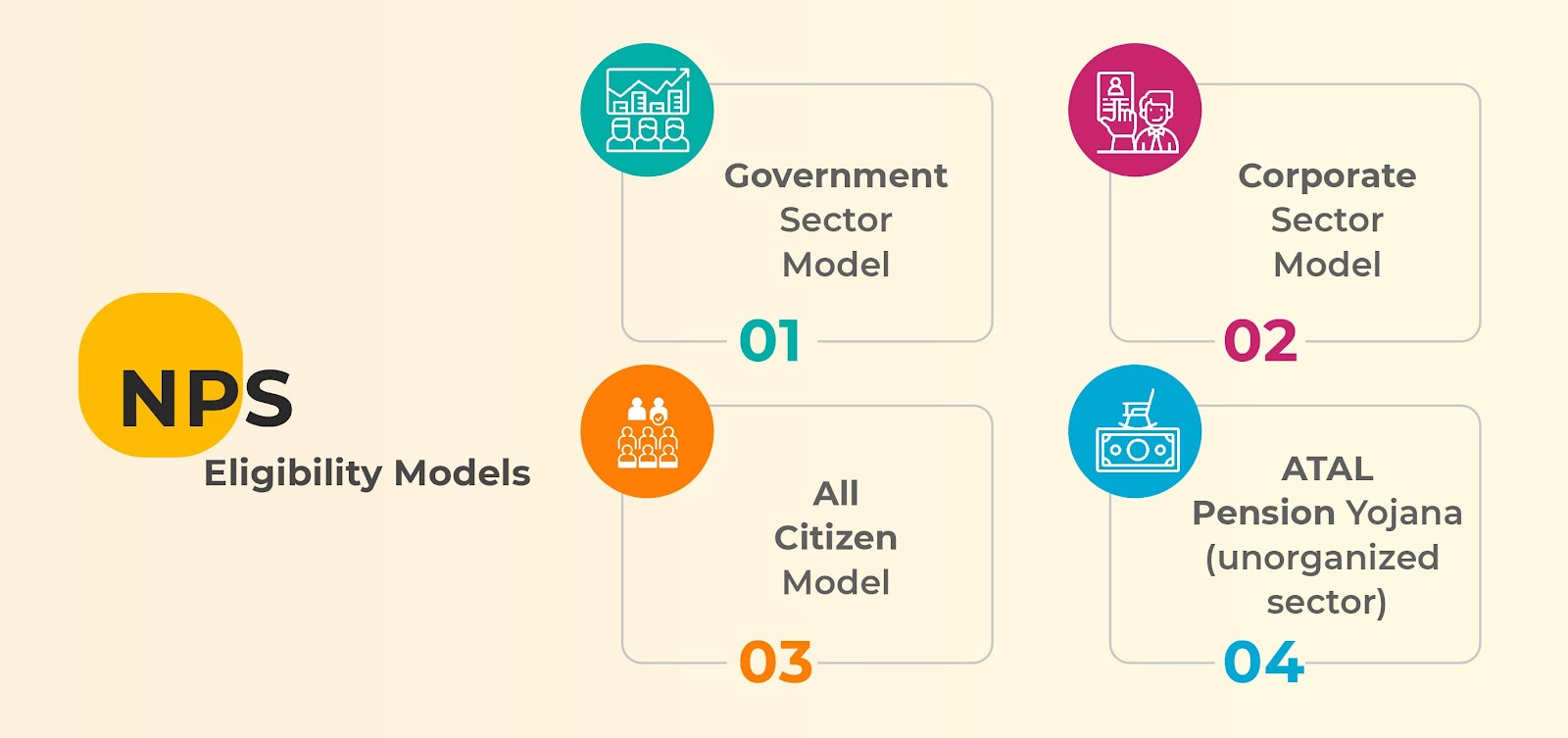

NPS ELIGIBILITY MODELS

National Pension Scheme has developed 4 models or categories catering to a different kind of employed citizens who would enroll in the scheme under their respective categories & need to comply with the requirements in each one:

Government Sector Model:

Central Government: This model is applicable for only the employees of the central government who joined on or after 1st January 2004. The employees(who joined before the launch) who are not covered under this model can enroll in the scheme through the All Citizens model.

State Government: This model is applicable for only the employees of the state government who joined on or after the date specified by the state governments. The employees(who joined before the launch) who are not covered under this model can enroll into the scheme through the All Citizens model.

Corporate Sector Model: This model is applicable to the employees of the corporate organizations registered with the NPS scheme. The model allows the flexibility to employees on choosing the asset allocation for all the employees as well as allowing investment choices to be made by employees.

NPS All Citizens Model: This model is for all the citizens of India including the employees whose employers are not registered with NPS, self-employed individuals, or any other citizens for joining the NPS scheme through POPs or eNPS.

Swavalamban Yojana/Atal Pension Yojana (For Unorganised Sector Workers): This Yojana model is applicable to the workers of unorganized sectors for opening the NPS-Swavalamban Account.

Read More: Kisan Vikas Patra Scheme

Features of National Pension System

Some of the important features of the NPS Scheme includes:

TYPES OF ACCOUNTS

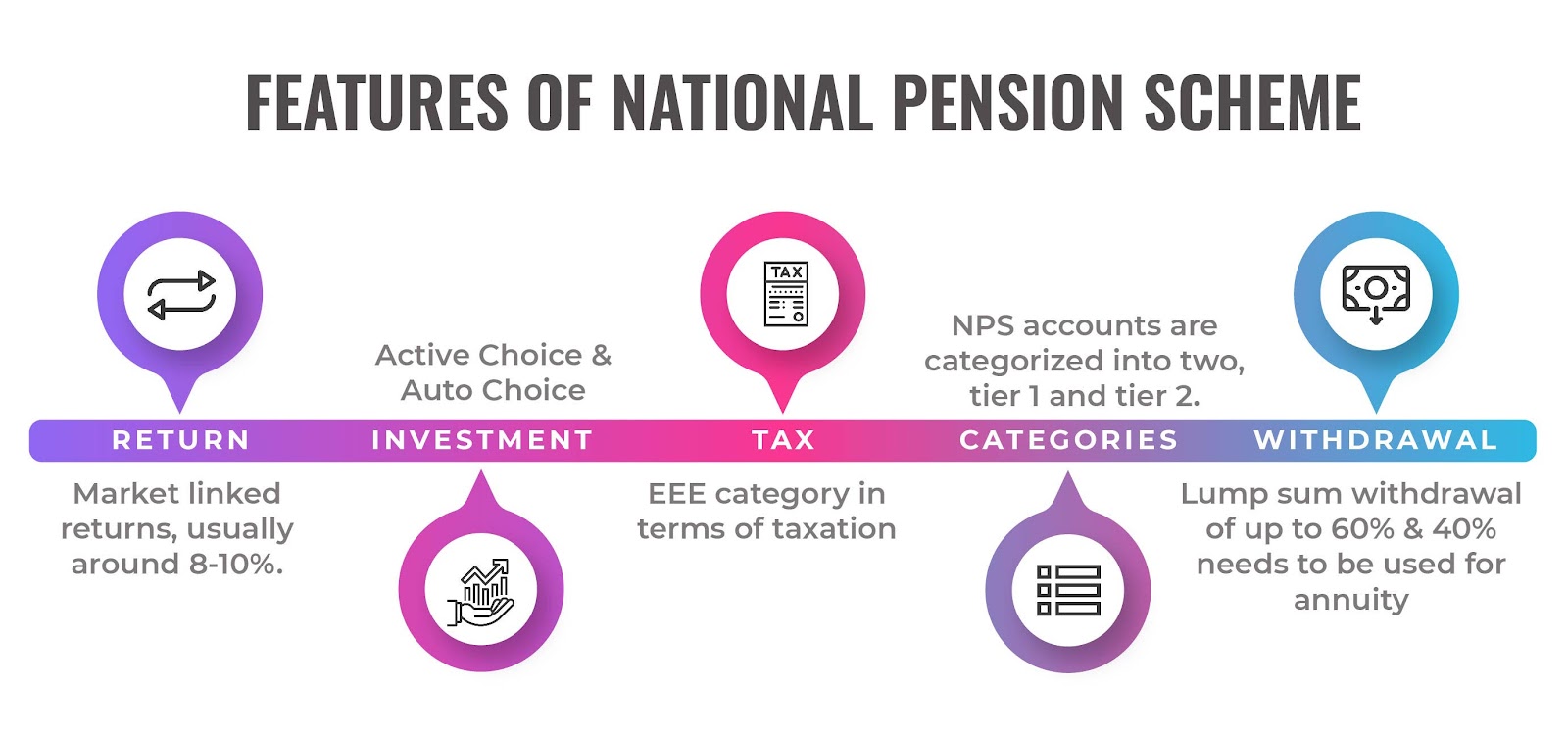

There are two types of accounts offered by the National Pension System. These are:

- Tier-1 Account: Tier-1 Account is the account that has a lock-in till the retirement of individuals i.e withdrawal is not allowed before the retirement. This account aims to build a large corpus through the disciplinary & systematic contributions by the holder and by making investments in the various asset classes for generating returns on investment. The corpus would then later be used to meet the financial needs of the individual after the retirement.

- Tier-2 Account: Tier-2 is a voluntary account for savings purposes offering high liquidity by the way of allowing withdrawals at any time by the account holders as per the requirements. This account can only be opened by the individuals who have an active Tier-1 NPS Account. There is no lock-in period in this account.

INVESTMENT OPTIONS

The NPS Scheme invests the assets across different asset classes namely Class E that invests in equity stocks, Class C that invests in corporate bonds, Class G that invests in the government bonds (issued by Central or State govt.) & Class A investing in AIFs like REITs(Real Estate Investment Trusts) & InVITs(Infrastructure Investment Trusts).

The NPS Scheme subscriber has to choose from the below mentioned two investment choices :

Active Choice

In Active investment strategy, the subscriber has to decide the asset allocation of the investment in Equity, Corporate Bonds, Government Bonds & AIFs. The subscriber has the full right to select the proportion of investments in the asset classes available for the investment.

However, there are some conditions in this strategy:

- The allocation of the portfolio in Equity (Class E) cannot exceed the maximum limit of 75% up to the age of 50 years.

- After 50, the allocation to equity would reduce by 2.5% every year to come at the investment allocation of 50% when the individual turns 60.

- For government employees, a maximum of 50% allocation can be made in equities.

- Also, the investment allocation in AIFs Alternative Investment Funds have been capped at 5% of the total portfolio.

Auto Choice

Auto Choice is a type of passive investment strategy where the subscribers do not need to decide any allocations to be made in different asset classes, rather the investments are made in the specified asset classes by following the lifecycle approach. Here the subscriber would have a higher asset allocation in equity class at a younger age and later on getting older, the allocation to the equities will be automatically reduced to bring more stability in the portfolio while near to the retirement.

In Auto Choice Investment preference, there are 3 options having different asset allocation strategies suitable to investors with varied risk appetite. The subscriber need to choose the one lifecycle fund approach which is suitable to his risk preferences out of these:

- Aggressive Lifecycle Fund

Aggressive Lifecycle Fund is suitable for investors who want a high allocation of the portfolio in equity asset class by taking high risks. The allocation to equity is 75% of the portfolio up to the age of 35, later it will reduce every year to come down at 15% by the age of 55 years.

- Moderate Lifecycle Fund

Moderate Lifecycle Fund is suitable for investors having a moderate risk appetite and thereby wants to invest a moderate portion in the equity asset class. The allocation of 50% of the total assets is made in equities up to the age of 35 and later the allocation is automatically reduced every year to come at 10% by the age of 55 years.

- Conservative Lifecycle Fund

Conservative Lifecycle fund is suitable for conservative investors who want lower allocation to equity in the portfolio. Here, the equity allocation of the portfolio is capped at 25% up to the age of 35, and later the allocation is reduced to come down at 5% by the age of 55 years.

The subscribers also have the option to switch between Auto & Active choice once a year. For adopting any of the above-mentioned investment strategies, the subscribers can choose any one of the pension fund managers authorized by the PFRDA to manage the assets.

CONTRIBUTIONS

The contribution limits vary in the account i.e in Tier-1 & Tier-2. Both accounts have different rules for contributions to be made into the account:

Tier-1: In the tier-1 account, the minimum contribution required for opening the account is Rs.500. And there is a requirement to make a total of minimum contributions of Rs.1000 every financial year.

The subscriber needs to make at least 1 contribution in a year to keep the account operational. Also, minimum amount required to make deposits after initial contribution is Rs.500.

Tier-2: In the tier-2 account, the minimum contribution required to open the account is Rs.1,000. And there are no requirements to maintain a minimum balance in the account at the end of each financial year.

Also, there is a minimum contribution size of Rs.250 for making a deposit.

RETURNS

The NPS Scheme makes investments across different asset classes for generating returns for the subscribers. The returns from the NPS schemes vary across asset classes as well as the investment preference of the scheme opted by subscribers. The portfolio with a higher allocation to equity securities would have the potential to generate higher returns whereas higher investments in government securities would offer stable returns to the investor.

The returns from NPS also vary across pension fund managers as they would invest in securities as per their discretion, thereby resulting in varied returns from different pension fund managers.

The returns from the NPS schemes managed by pension fund managers have been offering annual returns in the range of 8-10% since inception.

CHANGE OF SCHEME/PF MANAGER

The subscribers have the option to change the pension fund manager or shift to another PF manager authorized by PFRDA if they are not satisfied with the performance of the present one.

TAXATION

Following are the taxation rules applicable to the NPS Scheme:

- Tier-1: The tier-1 account investments are taxed at the slab rate over & above the deduction limits offered to investors. The deductions are:

- The subscribers can claim tax deductions of up to Rs.1.5 lakhs for making investments in the NPS Tier-1 account under section 80CCD of Income Tax Act,1961. The self-employed individuals can claim tax deductions of up to 20% of their gross income with a maximum limit of Rs.1.5 lakhs.

- Also, the NPS investors can claim tax deductions of up to Rs.50,000 for making investments under Section 80CCD(1B) of the IT Act. This deduction is over & above the tax deduction limit offered by the section 80c and is exclusively offered to NPS account holders.

- The contributions of the employers (either public or private employer) to the employee NPS Account are also eligible for claiming tax deductions under section 80CCD(2) up to 14% of the salary contribution in case of a government employee and 10% of the salary’s contribution of employer in the private employee account.

The NPS investments into Tier-1 Account come under the EEE category where the investments made into the account, returns earned & the amount at the maturity are all exempted from paying taxes.

2. Tier-2: The Tier-2 account allows claiming tax deductions only by government employees on making a maximum investment of Rs.1.5 lakh with a lock-in period of 3 years under section 80c of Income Tax Act,1961.

Investments into the tier-2 accounts made by all other investors will be taxed at the slab rate applicable to them.

NPS PARTIAL WITHDRAWALS

The partial withdrawal rules as follows:

- Tier-1 Account: The Tier-1 Account allows partial withdrawals by subscribers for meeting the specified needs such as for a child’s education, buying a house, or meeting any medical emergencies. The other conditions are:

- The withdrawals of maximum up to 25% of the total corpus are allowed from the account after completion of 3 years from the date of account opening.

- The withdrawals can only be made for a maximum of 3 times during the whole tenure of the scheme and with a mandatory gap of 5 years(not applicable in case of meeting medical emergencies) in between the withdrawals.

- Tier-2 Account: This account is highly liquid and subscribers are allowed to make withdrawals at any time as per their needs.

WITHDRAWALS AT MATURITY

The Tier-1 account of the NPS Scheme has maturity(or lock-in) till the retirement of the subscriber after which the withdrawal needs to be made from the account. However, the withdrawals from the scheme can also be postponed till the age of 70.

At the time of retirement, the subscriber has to withdraw from the NPS account in the following manner:

- As per the NPS account rules, the subscriber has to make a lump-sum withdrawal of a maximum of 60% of the total corpus.

- And rest of the amount which is at least 40% of the corpus needs to be utilized by the subscriber for purchasing an Annuity Scheme.

ANNUITY

An annuity scheme is provided by the life insurer Annuity Service Providers appointed by the PFRDA who would provide regular pensions every month to the subscribers till the duration as chosen by the subscriber.

Benefits of Investing in National Pension Scheme

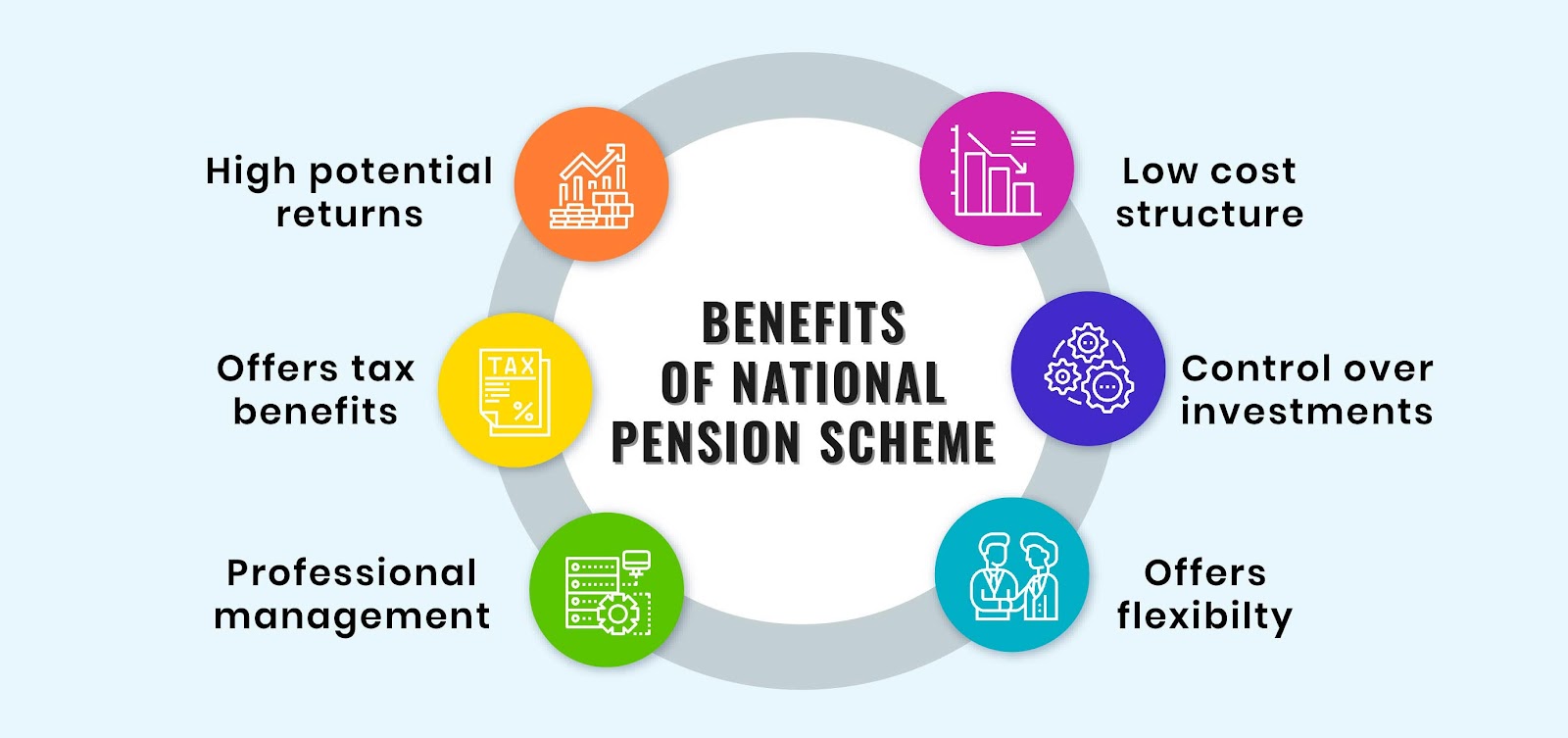

HIGH RETURNS

Investments across the asset classes including the equities by the pension fund managers for the NPS scheme provides the potential to earn high returns on the investments.

The scheme customized for high allocation in equities(active choice) or in case of aggressive lifecycle fund(auto choice option), the return potential would be higher as compared to others.

TAX BENEFITS

Investments or Contributions in the National Pension System allows the individuals to claim tax deductions under the sections 80CCD, 80CCD(1B) & 80CCD(2) of the Income Tax Act.

Also, the NPS scheme comes under the EEE i.e Exempt-Exempt-Exempt category in terms of taxation. The investments made into the account, returns earned & as well as the withdrawal at the maturity are exempted from the taxes. This also makes it one of the best tax saving investment options along with being the best retirement scheme.

PROFESSIONAL MANAGEMENT

The contributions made into the NPS account for investments are handled by professional pension fund managers. These are the industry experts having a lot of experience in portfolio management along with a high understanding of the financial markets which provides the potential to generate good returns.

The pension fund manager works with lots of analysts & researchers to make the selection for the best securities across asset classes which are suitable for the investment strategy of the scheme.

LOW COST

The cost structure for the NPS scheme is very low as compared to the other investment schemes available in the market.

The management charges (expense ratio) for managing the investments by pension fund managers are as low as 0.01% p.a for the accumulated amount. Also, there are very minimal charges for opening the account by POPs & CRA.

TRANSFER

PRAN is a unique number assigned to the subscriber which is completely portable, the subscribers can easily transfer their NPS account from the old employer to new in case of employment changes by filling the necessary application form. Also, the subscribers can shift from the selected POP to the other.

CONTROL

The NPS scheme holders have control over their investments as they can choose the allocation to different asset classes as per their risk preferences which would also provide them the opportunity to take high risks(i.e by allocating higher portion in equities) for earning higher returns and similarly they can bring more stability in their investment portfolio by allocating in low-risk investments.

This control helps the subscribers to take risks as per their risk profile & return requirements.

FLEXIBILITY

The National Pension System scheme provides high flexibility to the subscribers by allowing them to select the pension fund manager, investment preference of their choice. The subscribers even has the option to switch between investment preference from active to auto or vice-a-versa once a year and can change the fund manager if they are not satisfied with the performance of the previously selected fund manager.

Also at the time of retirement, the subscribers have the flexibility to choose the annuity service provider as well as the annuity scheme as per their will.

SIMPLE PROCESS

The process of doing registration for the NPS scheme is simple and can easily be done by the subscriber online. Even, the subscribers can make e-signatures for completing the whole process and therefore making it paperless.

TRANSPARENCY & REGULATIONS

The performances of the NPS Scheme are regularly tracked & monitored by the NPS trust and comes under the regulations of PFRDA which is backed by the Government of India. Also, the subscriber can easily track & monitor the performance of their selected investment strategy through their POP’s website or other websites.

Read More: ICICI Prudential Freedom SIP

NPS Pension Fund Managers

The money invested from the National Pension Account is managed by PFRDA authorized pension fund managers. Currently, there are 8 pension fund management entities managing the wealth of NPS scheme holders across asset categories i.e in Equities, Corporate Bonds, Government Bonds & AIFs. The managers are:

- LIC Pension Fund Limited

- SBI Pension Funds Private Limited

- UTI Retirement Solutions Limited

- Birla Sun Life Pension Management Limited

- Reliance Capital Pension Fund Limited

- Kotak Mahindra Pension Fund Limited

- HDFC Pension Management Company Limited

- ICICI Prudential Pension Funds Management Company Limited

Read More : Invest in Post Office Saving Scheme

Top Annuity Service Providers

Annuity Service Providers are the IRDA(Insurance Regulatory & Development Authority) authorized providers of the annuity scheme who are responsible for providing regular pensions to the annuity holders. The NPS account holders upon retirement are required to purchase an annuity scheme with at least 40% of the total corpus, doing which they would receive a regular pension or monthly payments by the ASP for the duration of the scheme as selected by the holder.

Currently, there are 12 Annuity Service Providers appointed by the Pension Fund Regulatory and Development Authority for providing annuity services to the individuals who have put their money into annuity schemes from the corpus in the NPS account. These are:

- Life Insurance Corporation of India

- HDFC Life Insurance Company Limited

- SBI Life Insurance Company Limited

- Star Union Dai-ichi Insurance Company Limited

- Life Insurance Corporation of India

- India First Life Insurance Company Limited

- Edelweiss Tokio Life Insurance Company Limited

- Bajaj Allianz Life Insurance Company Limited

- Canara HSBC Oriental Bank of Commerce Life Insurance Company Limited

- Kotak Mahindra Life Insurance Company Limited

- Tata AIA Life Insurance Company Limited

- Max Life Insurance Company Limited

The ASPs mentioned above are empaneled by PFRDA for servicing the annuity requirements of the subscribers, the NPS account holders have to choose any one of these for meeting their pension needs. The subscribers would have the option to choose from the various annuity schemes having varied durations & characteristics.

How to open an NPS Account ?

NPS Account can be opened by completing the required registration process through the online mode i.e through the eNPS website/online portals of POP-SP or offline i.e by reaching the nearest POP-SP(Point of Presence-Service Providers).

- Through Point of Presence-Service Providers: This process of doing registration for the NPS scheme involves the applicant performing the following tasks:

- The applicant needs to obtain a PRAN( Application form his nearest Point of Presence or download the form the POP’s/eNPS’s website.

Important Terms

PRAN- or Permanent Retirement Account Number is a unique 12 digit number allotted to the subscriber which provides an authentication of the successful registration of the subscriber with the NPS Scheme.

Point of Presence-Service Providers- POP-SPs are the intermediaries appointed by the PFRDA for providing access to the NPS Scheme through their wide network to the Indian Citizens. POPs are responsible for performing the functions like accepting the subscriber registration forms, verifying the filled forms or KYC documents, submitting the forms to CRAs, receiving & processing of intital as well as regular contributions from subscribers, making changes in subscriber details on request & handling the subscriber’s queries.

CRA: is the Central Recordkeeping Agency i.e NSDL appointed by the PFRDA for providing the services related to the issuance of the PRAN, keeping records of information & transactions, accepting the requests for change in information of the subscriber’s PRAN details & others by interactions with the POP-SP through its facilitation centers located across the country.

- After obtaining the application form, the applicant needs to fill the required details in the form including attaching photographs, signatures, entering identity information, selected scheme preference details, etc. and submit it to their POP-SP along with the mandatory KYC documents for the proof of identity & address.

- Also, the subscriber needs to make the initial contribution for the scheme to the POP-SP while submitting the application for opening the NPS Account.

- The POP-SP will then verify the information and pass the form along with the documents to CRA for the issuance of PRAN.

- The whole process of registration & issuance of PRAN will be completed within 10 days after the CRA receives the registration form & KYC documents. Upon the issuance of PRAN, the subscriber will be notified through email or the registered mobile number. The subscriber can also check the status of PRAN dispatch through this link by entering the receipt number issued by the POP while submitting the application.

Online eNPS: The online registration of NPS can be done through the eNPS website.

- The applicant must have a Permanent Account Number (PAN) for applying to get PRAN online.

- The applicant would have to submit his KYC details for the KYC verification with the selected POP.

- The subscriber would need to fill the mandatory details in the online form along with uploading the scanned copy of the following documents:

- PAN Card

- Canceled Cheque

- Photograph

- Signature

- Then the applicant is required to make payment for the initial contribution to the NPS account.

- After the allotment of PRAN, there are two options available to the subscriber for the completing the whole process:

- e-Sign: Choosing this option on the e-sign page, the applicant would receive an OTP on the registered phone number with his adhaar card for verification. Upon successful verification, the form will be e-signed therefore not requiring any physical signature.

- Print & Courier: Choosing this option, the subscriber would be required to print the form, paste a photograph & do a signature on the form and send that to the CRA’s office address mentioned on the page.

Who should invest in NPS Scheme ?

Investments in the National Pension System can be made by all the citizens of India. Investments in NPS are suitable for employees/workers especially in the private or unorganized sector to develop a large corpus through regular contributions into the account for financially securing their future after retirement. However, the systematic structure of the NPS scheme makes it ideal for anyone who wants to receive regular pensions after the age of 60.

Also, the NPS scheme is one of the best options for Tax-saving investments which makes it suitable for anyone who wants to save taxes by making investments.

Also Read: Retirement Planning with Mutual Funds

NPS vs Other Tax saving instruments - Comparison with Other Schemes

| Investments | NPS (National Pension Scheme) | ULPPs (Unit Linked Pension plans) | EPF (Employee Provident Fund) | PPF (Public Provident Fund) |

| Lock-in period | Till Retirement i.e 60 years of age | 5 Years | 5 Years but full withdrawal allowed after 58 years of age | 15 Years |

| Partial Withdrawals | Allows partial withdrawals of up to 25% of the corpus. | Not Allowed | Partial withdrawals allowed after 5 years for specific expenses. Also, allowed in case of unemployment for more than 1 month. | Pre-mature withdrawals allowed after 5 years with subject to interest penalties. |

| Withdrawals at maturity & Annuity | Allows withdrawals of up to 60% of the corpus & at least 40% needs to be utilized for annuity scheme | Allows withdrawals of 33% of the corpus & rest needs to be utilized for the annuity. | Lump-sum withdrawal, no annuity applicable | Lump-sum withdrawal, no annuity applicable |

| Returns | 8-10% expected returns | Guaranteed maturity benefits b/w 101% to 195% on extra charges. | 8.5% in FY19-20 | 7.10% (Q1- FY2021) |

| Management Costs | 0.01% | 1.35% | No Costs | No Costs |

| Taxation | EEE category in terms of taxation. | ⅓ of the corpus is tax-free. And the other ⅔ taxable in the hands of investors. | EEE Category: Tax deductions under 80c, Interest & amount at the maturity are exempt from taxes. No tax benefits on withdrawals made before 5 years. | EEE Category: Tax deductions under 80c, Interest & amount at the maturity are exempt from taxes. |

NPS Vs ELSS

National Pension Scheme (NPS) | Equity Linked Saving Scheme (ELSS) | |

| Nature | Retirement saving scheme facilitating regular & disciplined investments. | Equity mutual fund offering tax benefits. |

| Lock-in Period | Till retirement | 3 Years |

| Returns | 8% - 10% p.a. | 12% - 14% p.a. |

| Premature Withdrawals | Allowed of up to 25% after 3 years | Not allowed |

| Taxation | EEE-Exempt in terms of taxation. Contributions, returns & maturity proceeds exempt from taxes | Eligible for deductions under Section 80C. Returns are taxed as per the applicable LTCG tax. |

| Withdrawal at maturity | 60% of the amount as a lump sum and the rest 40% needs to be used for annuity | Lumpsum or as per the investor’s needs |

Procedure for Opening an NPS Account

Through the online service eNPS, people may sign up and purchase a membership to the National Pension System. The following steps can be used to register for the program.

- Log in to the eNPS official website, and select your subscriber type from the options given below i.e. ‘Individual Subscriber’ and ‘Corporate Subscriber’.

- Select the appropriate residence status. 'Citizen of India' and 'NRI' are the available alternatives.

- Choose one or both Tier I account types as the former is required for long-term savings.

- Enter your PAN information and choose an appropriate bank or PoP. It is best to select a PoP with whom you already have a relationship because they will complete the KYC verification, such as a savings/current/Demat/account.

- Along with a voided cheque, provide a scanned copy of your PAN card. The picture file should be between 4KB and 2MB in size and be in the.jpg, .jpeg, or.png format.

- Upload your scanned photograph and signature. The file size should be the same as that of the above credentials.

- Once at the payment gateway, continue to pay the necessary fees using online banking. Your Permanent Retirement Account Number will be generated once the payment has been made.

FAQs - National Pension Scheme

Q. How much pension is given in National Pension Scheme ?

A. National Pension Scheme is a market linked product that allows you to invest in a variety of assets such as stock, government debt, corporate debt, and alternative assets.

Q. Is National Pension Scheme a good investment ?

A. Yes, NPS does make for a good retirement savings scheme and worth investing for 20 years.

Q. What is the NPS scheme ?

Ans. National Pension Scheme is launched by the Government of India to provide an architecture of systematic contributions & investments to the citizens of India for securing their future financially after the retirement. At the time of retirement, the scheme allows the subscribers to make a lump-sum withdrawal of up to 60% of the corpus & requires them to put the rest of 40% into the annuity scheme which will provide monthly pensions.

Q. Who is eligible to join the National Pension System (NPS) ?

Ans. All Indian citizens including NRIs(Non-Resident Indians) in the age range of 18-65 years are eligible to join the scheme. Whereas, the OCI, PIO holders & HUFs are not eligible to join the NPS scheme.

Q. What is a PRAN ?

Ans. Permanent Retirement Account Number (PRAN) is a unique 12 digit number allotted to the subscriber providing an authentication of the successful registration of the subscriber with the NPS Scheme.

Q. What are the types of accounts in the NPS scheme ?

Ans. There are two types of accounts offered by the National Pension System. These are:

- Tier-1 Account: Tier-1 Account is the mandatory account having a lock-in period till the retirement of the subscriber. This account aims to build a large corpus for retirement through the contributions by the subscribers & making investments to earn returns on them.

- Tier-2 Account: Tier-2 is a voluntary account for savings purposes which allows withdrawals at any time as per the subscriber’s needs. It is mandatory to have a Tier-1 account for opening a Tier-2 account.

Q. What is the investment preference in NPS ?

Ans. The NPS Scheme invests the subscribers’ contributions across different asset classes namely Equity stocks, Corporate bonds, Government bonds (issued by Central or State govt.) & AIFs like REITs & InVITs.

The NPS Scheme provides the subscriber with two options to choose from i.e Active & Auto Choice for selecting the investment or asset allocation strategy. Active Choice allows the subscriber to decide on the asset allocations as per his preferences, whereas in Auto Choice the asset allocation strategy is based on a lifecycle approach.

Q. What are the benefits of the NPS account ?

Ans. Some of the benefits of the NPS account includes:

- Low-cost structure

- Professional management of assets

- Provides Tax benefits

- Transparency

- Control over Investments

Q. What are the tax benefits on the NPS account?

Ans. Investments or Contributions in the National Pension System are eligible for claiming tax deductions under the sections 80CCD, 80CCD(1B) & 80CCD(2) of the Income Tax Act.

Also, the NPS scheme comes under the EEE (Exempt-Exempt-Exempt) category for taxation purpose i.e the investments or contributions, returns earned & the withdrawal amount at the retirement are exempted from the taxes.

Q. What are the requirements for minimum contribution in NPS Account?

Ans. In the tier-1 account, the minimum contribution required for opening the account is Rs.500. And a minimum contribution of Rs.1000 needs to be made every financial year.

In the tier-2 account, the minimum contribution required to open the account is Rs.1,000. And there are no requirements with respect to minimum contributions in a financial year or maintaining any minimum balance at the end.

Q. Who handles investments made from an NPS Account?

Ans. The contributions made into the NPS account for investments are handled by professional pension fund managers. They are highly qualified managers having a lot of experience in investment management along with a high-level understanding & knowledge of the financial markets which provides the potential to generate good returns on the investments from the NPS account.

Q. Is it possible to change my investment choices & pension fund manager ?

Ans. Yes, the National Pension System scheme provides the flexibility of changing the pension fund manager & the investment preferences as per the subscribers’ choice. And the subscribers can switch between the investment preferences i.e from active to auto or vice-a-versa once a year.

Q. How is the NPS Scheme different from other retirement savings schemes ?

Ans. Here is the comparison of the NPS with other schemes

Q. How many NPS accounts I can open ?

Ans. The NPS scheme has two types of accounts i.e Tier-1 & Tier-2 And only one account of each is allowed, the individuals are not allowed to open multiple NPS accounts.

Q. Can the subscriber choose different pension fund managers for Tier-1 & Tier-2 Accounts ?

Ans. Yes, there can be two different pension fund managers for the Tier-1 & Tier-2 account of the NPS.

Q. What happens in case of the death of an NPS subscriber ?

Ans. In the event of the death of NPS subscriber, the amount accumulated would be passed on to the nominee or legal heir of the subscriber.

Q. What is the annuity scheme ?

Ans. An annuity scheme is provided by the Annuity Service Providers (Life Insurance companies) appointed by the PFRDA who would provide regular pensions every month to the subscribers till the duration of the annuity scheme as selected by the subscriber.

Q. Who are the Annuity Service Providers ?

Ans. Annuity Service Providers are the IRDA authorized providers of the annuity scheme who are responsible for providing regular pensions to the annuity holders. Currently, there are 7 ASP entities appointed by the PFRDA for providing pension to the NPS account holders after their retirement.

Q. What are the tax benefits on the Annuity scheme ?

Ans. The subscribers have the benefit of tax exemption on the amount utilized for purchasing the annuity scheme. However, there are no tax benefits on the monthly pension payments made by the ASPs and they are taxed as per the slab rate applicable to the account holder.

Read More:

SBI Fixed Deposit Interest Rates

HDFC Fixed Deposit Interest Rates