NPS Vs PPF: Comparison, Tenure, Risks, Returns, Tax Benefits & Which is Better

Updated on January 9, 2024

Written by Manish Kothari

CEO Zfunds

Share

Get Research Approved Mutual Funds for Your Portfolio

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

Difference Between NPS Vs PPF

The National Pension System (NPS) scheme was launched by the Government of India and is regulated by Pension Fund Regulatory and Development Authority (PFRDA). It is specifically designed to facilitate the financial requirements of people after retirement. It was launched in January 2004 initially for government employees and later on, in the year 2009, the scheme was made open to a wider section of the population.

The scheme lets the subscribers make monthly investments into a pension account while working. After retiring, the people subscribed to the scheme can withdraw a portion from the corpus as a lump sum withdrawal and use the rest of the corpus for buying an annuity to receive a regular income from the annuity scheme purchased.

Any Indian citizen over the age of 18 years is eligible for this scheme and the person has to conform to KYC (Know Your Customer) standards. NRIs are also eligible to subscribe to this scheme. A person cannot open more than one account under this scheme. National Pension System (NPS) Scheme which is regulated or administered by the Pension Fund Regulatory and Development Authority (PFRDA) also allows investors who have subscribed to the scheme an early exit option from the scheme before retiring or choosing superannuation.

NPS Features and Benefits

1.) Flexibility

The scheme gives the flexibility of choosing by offering two choices for investing, i.e., auto choice and active choice. Auto choice is a default option for the account holder(s). Under this option, fund investments are managed by an appointed manager as per the account holder’s age profile.

On the other hand, the individual has an option to decide among the available asset classes in which to invest. They can allocate varying percentages of contributed funds in different asset classes like equity, corporate bonds, government bonds & AIFs. The maximum allocation to equities has been capped at 75% up to the age of 50 years. After that the equity portion begins to reduce systematically.

The investors also have an option to switch their fund managers if they are not satisfied with the performance.

2.) Liquidity

The NPS scheme offers the investors two types of accounts i.e Tier-1 account & Tier 2 account.

Tier-1 Account has a lock-in till the retirement of individuals i.e. withdrawals are not allowed before retirement. In Tier-2 Accounts, individuals can make withdrawals at any time as per their needs & requirements. So, the Tier-2 account provides high liquidity.

3.) Partial Withdrawals

Premature withdrawals(anytime before the retirement) from this account are allowed but subject to some conditions that are:

- Withdrawals can only be made for meeting some specified financial requirements like for a child’s education, buying a house, or for meeting medical needs.

- Premature withdrawals are allowed only up to the extent of 25% of the total corpus is allowed after the 3 years of opening the account.

- Also, withdrawals can be made for a maximum of 3 times that to each one after the gap of 5 years.

4.) Tax Benefits

The tier 1 account investments in the NPS scheme come under the EEE category i.e. Exempt-Exempt-Exempt in terms of taxability. By EEE or Exempt-Exempt-Exempt category, there are three types of exemptions in taxes. First Exempt means the investment is qualified for deduction and a portion of annual income which is equal to the investment amount is not taxable. Second Exempt means interest which is earned on investment is exempted.

Third Exempt means the amount generated from investment is not taxed at the time of withdrawal. Tier 2 account permit claiming tax deductions just by government employees on making at most of the venture of Rs.1.5 lakh with a lock-in term of 3 years under Section 80c of the Income Tax Act,1961.

As the investments or contributions in the National Pension System are eligible for claiming tax deductions by the individuals under sections 80CCD, 80CCD(1B) & 80CCD(2) of the Income Tax Act.

Read More: |

PPF Features and Benefits

Public Provident Fund (PPF) is a prevalent scheme in the country. The Public Provident Fund is a long-term investment. This scheme produces a stable flow of income through guaranteed returns. The minimum amount for investments in a PPF account is Rs. 500 and the maximum is Rs 1.5 Lakhs in a financial year.

1.) Tenure of investment

Public Provident Fund is a long-term investment of around 15 years. There is also an option to extend the tenure by 5 years after the termination of the lock-in term.

2.) Loan Facility

This scheme offers the benefit of availing loans against investment. Loan can only be granted from the third year till the end of the sixth year from the time of account activation. It is important to note that the maximum amount that can be claimed for the purpose is 25% of the total account balance. The maximum term of loans against PPF is 36 months.

3.) Criteria of Eligibility

Indian citizens over the age of 18 years can open PPF accounts and minors are also eligible to open accounts under this scheme, but the account has to be operated by a guardian or a parent. NRIs and HUFs are not allowed to open an account under this scheme.

4.) Tax Benefits

All deposits made under this scheme are tax-deductible under Section 80C of the Income Tax Act, 1961. During the time of withdrawal, the amount accumulated along with interest is also exempted from tax.

5.) Nomination Facility

Accountholders under this scheme can assign a nominee for his account during the time of opening the account or later.

6.) No Risks Involved

This scheme involves no risks in terms of the safety of capital as well as the interest because of the sovereign guarantee by the Government of India.

Read More: |

Comparison of NPS and PPF

After knowing about both schemes, it is important to compare these schemes in different areas and realize the differences between them.

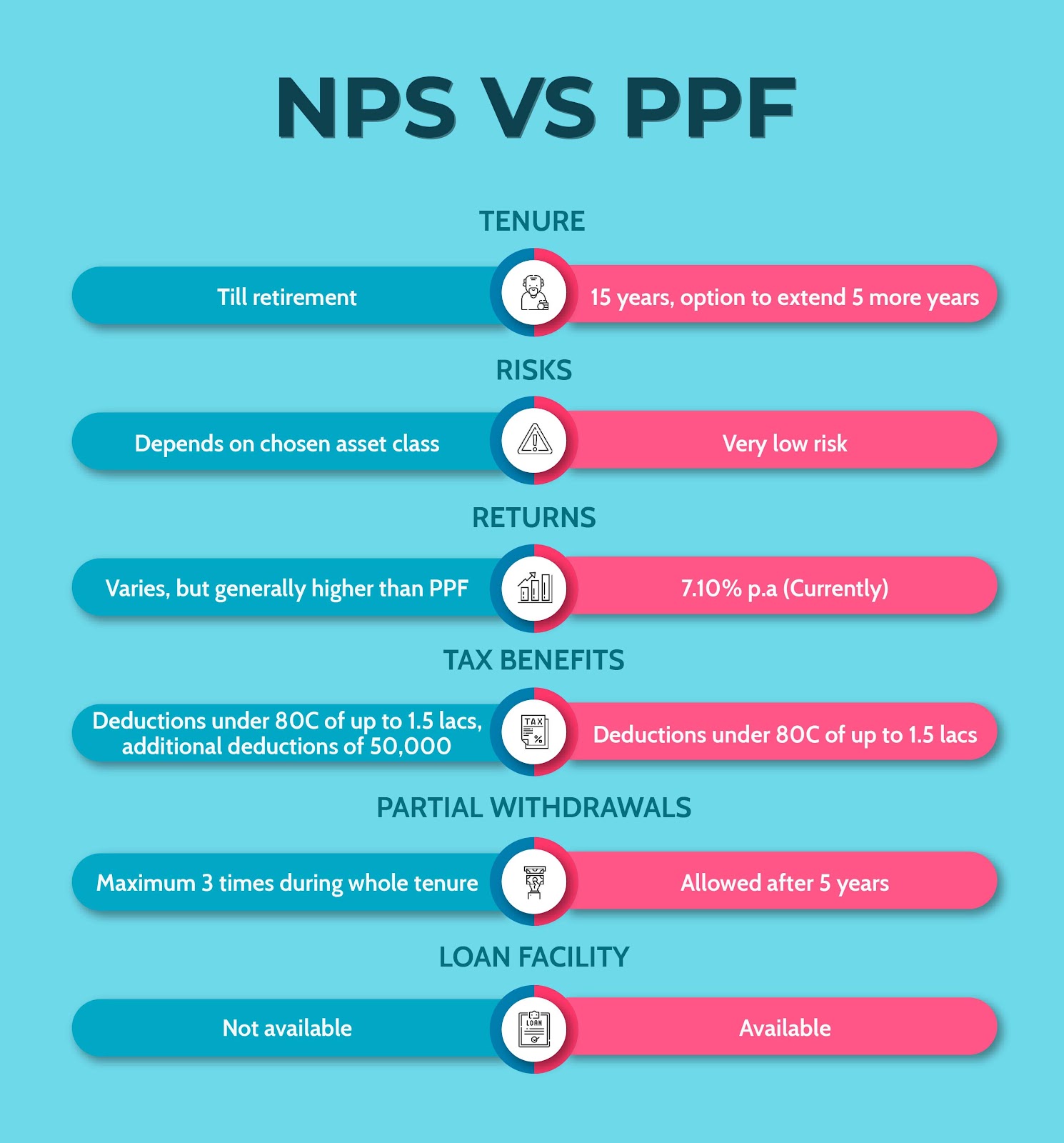

Risks Involved

The National Pension System (NPS) account carries risks on investments. The amount of risks varies across the investment options & asset classes chosen for investments. For example- The higher allocation of the portfolio in equities will carry higher risks whereas the higher allocations of the portfolio in government bonds or corporate bonds will carry lower risks.

On the other hand, the amount of investment & the interest from the PPF account are backed by the sovereign guarantee of the government so carries almost no risk involved.

Returns

The Public Provident Fund has a fixed rate of interest which is set quarterly by the Ministry of Finance. Currently, the PPF account offers an interest rate of 7.10% p.a.

The returns from the NPS account vary across the investment options & asset classes selected for allocations. However, returns from the NPS Account are generally higher than those of the PPF Account.

Tax

Investing in PPF accounts for a maximum of Rs 1.5 Lakh per annum provides tax deduction under Section 80C of the Income Tax Act, 1961. PPF also enjoys the benefits of tax exemption. Investment of NPS for a maximum Rs 1.5 Lakh per annum provides tax deduction under Section 80C of the Income Tax Act, 1961. The returns from the scheme are also exempted from taxes. NPS also enjoys additional tax deductions under Section 80 CCD (1B). Post maturity, the withdrawal amount as well as the returns earned are also exempted from taxes.

Liquidity

The Public Provident Fund (PPF) allows the partial withdrawal facility after 5 years of opening the account. The National Pension System (NPS) scheme allows a maximum of three partial withdrawals during the whole tenure for emergencies under particular policies. The withdrawals can be made after the completion of 3 years from the date of opening the account.

One can also avail loan against the balance in the PPF account. Loan can also be availed against the PPF account from the third year to the end of sixth year and the maximum amount that can be availed is 25% of the balance in the PPF account.

Objective

NPS is specifically designed to help citizens to meet their financial requirements after retirement whereas PPF is not designed especially to solely cater financial requirements of citizens after retirement. While this may be the reason for some citizens to invest into PPF, there are also many different requirements of different individuals such as child’s future savings, marriage savings, emergency funds, etc. PPF accounts can also be opened for minors which will mature in their adulthood and could help in meeting the child's financial requirements for education purposes. NPS account gets matures only when the account holder reaches the age of 60 years, which can also get extended till the age of 70 years.

| Parameters | NPS | PPF |

| Lock-in Period | Till Retirement | 15 years |

| Tax benefit | Can be claimed upto Rs 1,50,000 in a financial year under section 80C of Income Tax Act, 1961 and also recieves additional tax deduction under Section 80 CCD (1B). | Can be claimed upto Rs 1,50,000 in a financial year under section 80C of Income Tax Act, 1961. Interest also exempted from taxes. |

| Premature/ Partial Withdrawal | The National Pension System (NPS) scheme allows three partial withdrawals for emergencies under particular policies. | The Public Provident Fund (PPF) allows the partial withdrawal facility after the completion of 5 years. |

| Loan facility | Loan cannot be availed. | Loan can be availed against PPF account from third year to the end of sixth year of up to 25% of the balance in PPF account. |

| Maximum investment | Not set | Rs 1,50,000 in a financial year. |

Frequently Asked Questions

Q. What is NPS?

A. National Pension Scheme or the NPS, is a scheme launched by the government of India. It is an account which helps to collect a corpus for the account holder which can be used after retirement as per the needs of the individuals. NPS account is available for the general public between the age of 18-65 years.

Q. What is PPF?

A. Public Provident Fund or the PPF, is a long-term investment scheme launched by the National Savings Institute of Finance Ministry in 1968. This scheme helps an investor to create a large corpus through small savings made every year into the scheme. The PPF account also offers tax benefits under Section 80C of the Income Tax Act,1961.

Q. Does NPS and PPF have the same maturity period?

A. The tenure or maturity period is different for both the NPS and PPF. NPS has a maturity period till the retirement age of the account holder, while PPF has a maturity period of 15 years which can be extended for 5 more years.

Q. What is the interest rate offered by the NPS and PPF?

A. NPS does not offer a fixed rate of interest rather its returns are market-linked because of its investments in marketable securities like equity, bonds, REITs, etc. The interest rate for the NPS varies across investment options & PF managers but generally, we can expect higher returns in NPS as compared to PPF over the long term. PPF has a fixed rate of interest which is currently fixed at 7.10% p.a. It is subject to quarterly revisions by the Government of India.

Q. Are partial withdrawals allowed in the NPS and PPF?

A. Both NPS and PPF provide a partial withdrawal facility. NPS partial withdrawal is allowed only up to the extent of 25% of the total corpus. The withdrawal can only be done after the 3 years from the date of account opening and it can be done for a maximum of 3 times during the whole tenure. Also, there should be a difference of 5 years between the withdrawals.

While for the PPF, Partial withdrawals are allowed only up to 50% of the total corpus. The withdrawals can only be made after the completion of 5 years of the tenure. And, the limit for the withdrawal is restricted to 1 time during each fiscal year.

Q. Can we avail of a loan against NPS and PPF?

A. NPS does not offer a loan facility to its investors. While PPF offers a loan facility. The loan can be availed against the PPF account balance from the third year from the date of investment to the end of the sixth year. The loan amount can be extended up to 25% of the total corpus available at the time of taking a loan.

Q. Is there any tax benefit difference between the NPS and PPF?

Both NPS and PPF offer tax deductions under the Income Tax Act, of 1961. In both accounts, an investor can avail of tax deductions of up to Rs.1.5 lakh per financial year under Section 80C of the Income Tax Act, 1961. However, the NPS offers additional tax deductions of up to Rs.50,000 under Section 80CCD (1B).

Also Read:

Post Office Saving Schemes