Post Office Monthly Income Scheme (POMIS): Eligibility, Interest Rate, Benefits

Updated on May 23, 2025

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

Post Office Monthly Income Scheme

Post Office Monthly Income Scheme (POMIS) or Post Office Monthly Savings Scheme is a savings scheme offered by the Indian Post Office which upon a lump-sum investment offers a fixed interest payout every month to the account holders. Being backed by the Indian Government, this scheme is considered to be very consistent as it involves very low risks and offers good returns. The chances of default or capital losses are almost negligible in this scheme.

It is known to be suitable for those investors who are looking for a one-time investment for a long tenure. Also, the scheme is extremely helpful for individuals/senior citizens who want steady & regular income for meeting their financial needs.

The scheme comes with a maturity tenure of five years. The accounts opened under this scheme can be transferred from one post office branch to another across the country.

Eligibility Criteria

Any resident of India above the age of 10 is eligible to open an account. Non-resident Indians (NRIs) are not allowed to avail of the scheme.

Who can open a Post Office Monthly Income Account ?

Account may be opened by

(i) a single individual (above the age of 18 years)

(ii) Joint Account (Max. 3 adults)

(iii) Minor above the age of 10 years

(iv) A guardian may open the account on behalf of a minor or person of unsound mind.

POMIS account can be opened by a deposit through cash or cheque as well. In case of cheque, the date of realization of cheque in the account of government will be the date of opening of the account. Single account holders are allowed to convert their account into a joint account or vice versa.

Also Read: Kotak Bank FD Interest Rates

How to open a Post Office Monthly Income Account ?

- You'll need to pay a visit to your local post office branch to open a monthly income scheme account.

- First, you will need to open a post office savings account.

- Then, ask for the POMIS application form, fill in the required information, and attach the documents including identity and address proof.

- The document proofs will need to be self-attested.

- No online facility is available yet to open this account.

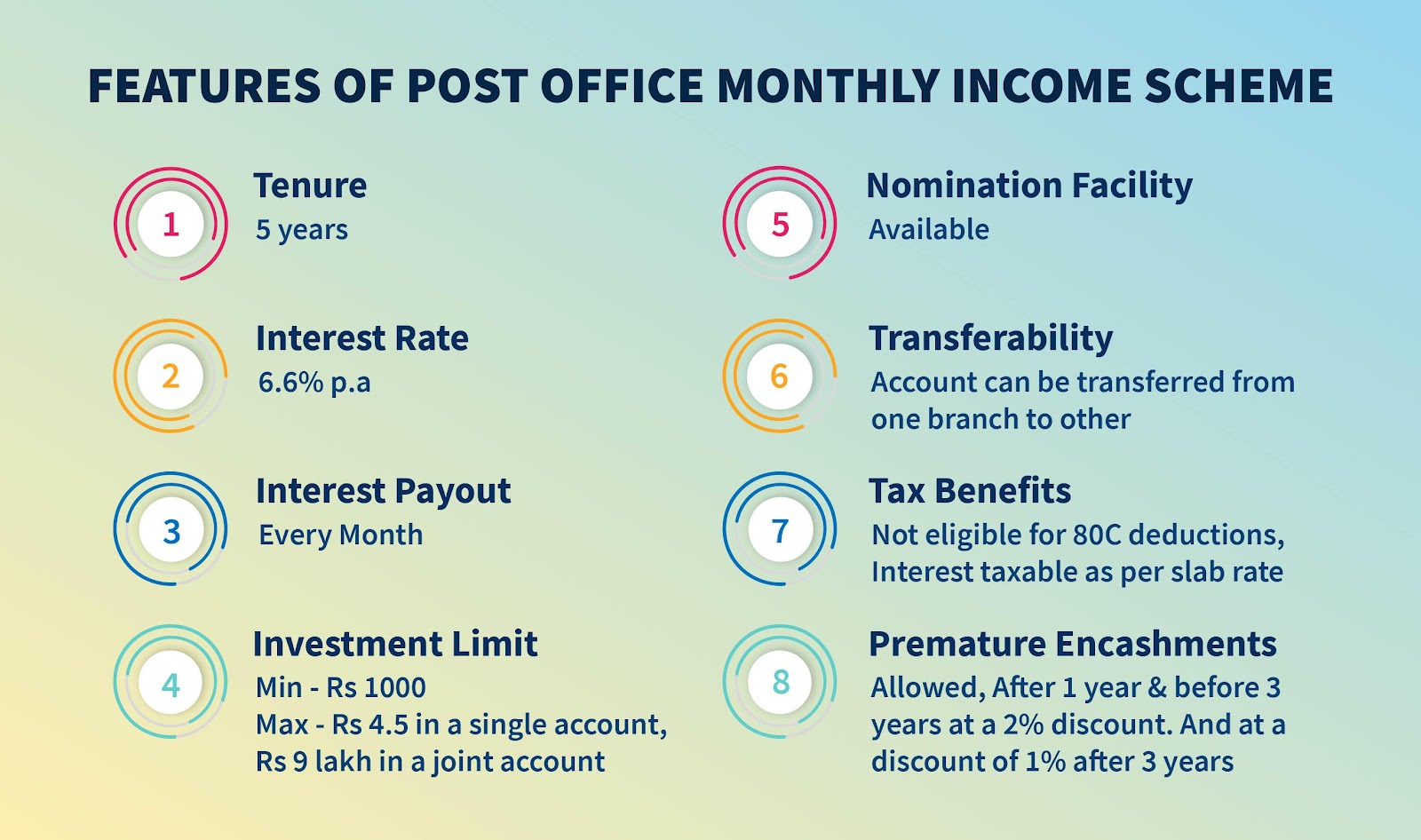

Features & Benefits of Post Office Monthly Income Account

Tenure

Post Office Monthly Income Scheme has a maturity tenure of 5 years. The investment amount is paid back to the depositor at the end of maturity.

Interest Rate

The interest rate offered on the account is fixed at a given rate and it is reviewed by the Ministry of Finance at the beginning of every quarter. However, interest is payable every month. Currently, the interest rate offered on the Post Office Monthly Income Scheme is 6.6% p.a.

Investment Limits

The minimum amount required to make investments into POMIS account is Rs.1,000 and in multiples of Rs.1,000 thereafter.

The maximum investment allowed for a single account is Rs. 4.5 lakh and Rs. 9 lakh for a joint account. A person may invest a maximum of Rs. 4.5 lakh in MIS (including the share in joint accounts).

Ownership in multiple accounts

Any number of accounts at any post office branch subject to the maximum investment limits could be opened by the account holders.

Payouts

Monthly payouts are made to the depositors in the form of interest. The returns & capital invested are backed by the sovereign guarantee of the Indian Government. The post-tax gains aren't really inflation-beating, but still are better than other saving schemes.

Tax Benefits

The investments or contributions in the post office monthly income scheme are not eligible for claiming deductions under Section 80C. Also, the interest on investment is taxable as per the slab rate.

Lock in Term

The scheme comes with a mandatory lock-in period of 5 years. Investors may also reinvest after the maturity period in the same scheme if they wish.

Involves Low Levels of Risks

PO Monthly Income Scheme is a very low-risk investment which provides guaranteed returns after maturity. The risks of capital losses are almost negligible in the account.

Nomination Facility

The investor has the facility to appoint a nominee for the deposit, who in the case of the investor’s demise, may claim the benefits and the account corpus. Nomination facility is available at the time of opening the account and during the tenure of the scheme as well.

Transfer Facility

If you are moving from one city to the next, you could easily transfer your investment to your new city's post office branch.

Premature Withdrawal Facility

The account could be prematurely en-cashed after one year but before 3 years at a 2 percent discount on the deposit and after 3 years at a 1 percent discount on the deposit. (Discount means a deduction will be made from the deposit)

Also Read: Post Office Saving Schemes

Comparison with other schemes

| Particulars | Post Office Monthly Income Scheme | Post Office Time Deposit | Senior Citizens Savings Scheme | Mutual Funds |

| About | Offers monthly payouts on a lump sum investment. | Term/Fixed Deposit for a specific tenure. | Offers quarterly payouts on a lump sum investment. Available exclusively for senior citizens. | Pooled Investment vehicle. Systematic Withdrawal Plan can be used to make regular withdrawals as per needs. |

| Interest Rate/Returns | 6.6% p.a. | 5.5% p.a. for 1,2 & 3 Years. 6.7% p.a. for 5 years. | 7.4% p.a. | Debt Funds: 5-7% Equity Funds: 12-15% Hybrid Funds- 8-10% (expected assuming long horizon) |

| Risks | Very Low | Very Low | Very Low | Low to High(varies) |

| Tenure | 5 Years | 1,2,3 & 5 Years | 5 Years with 3 year extension option. | Varies. |

| Investment Limits | Min- Rs.1,000 Max- Rs.4.5 lakh or Rs.9 lakh (joint account) | Min- Rs.1,000 Max- No limit | Min- Rs.1,000 Max- Rs.15 lakh | Min-Starts from Rs.100 & varies across schemes. Max- No limit |

| Tax Benefits | No tax benefits. | 5 Year Deposits eligible for deductions of up to Rs.1.5 lakh under 80C. | Investments of up to Rs.1.5 lakh eligible for deductions under 80C. | Investments in ELSS funds eligible for deductions under section 80C. |

Frequently Asked Questions (FAQs) -

Q. What is the tenure of the POMIS scheme ?

A. Post Office Monthly Income Scheme has a maturity tenure of 5 years.

Q. Is the nomination facility available ?

A. Yes, a nomination facility is available at the time of opening the account as well as during the tenure of the scheme.

Q. Does the scheme allow premature withdrawals ?

A. Yes, the deposits can be prematurely encashed after 1 year subject to the following penalty conditions:

Q. After 1 year but before 3 years: 2% discount on the deposit

A. After 3 years: 1% discount on the deposit

Q. Is a transfer facility available ?

A. Yes. Transfer facility is available in the scheme. One can easily transfer his/her account from one post office branch to another.

Q. What is the interest rate currently on POMIS ?

A. As of 1 October 2020, the interest rate offered on the Post Office Monthly Income Scheme is 6.6% p.a.

More Information:

AU Small Finance Bank FD Rates

Shriram Transport FD Rates

Senior Citizens Savings Scheme

Post Office Time Deposit

Public Provident Fund

Post Office Recurring Deposit