Post Office Recurring Deposit: Scheme Benefits, Interest Rate, Eligibility Criteria

Updated on October 6, 2022

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

Post Office Recurring Deposit

Post Office Recurring Deposits is a very popular savings scheme offering a disciplined approach of regular savings & investments by the investors. The scheme is one of the savings schemes offered by the Post Office through its branches across the country. The scheme being backed by the Government of India provides many benefits to the depositors including high safety, good interest rates, flexible investment limits, premature closure facility, and many more.

We’ll be covering everything about Recurring Deposits (RDs) in this article, let’s begin!

What is the Post Office Recurring Deposits (RDs) Scheme ?

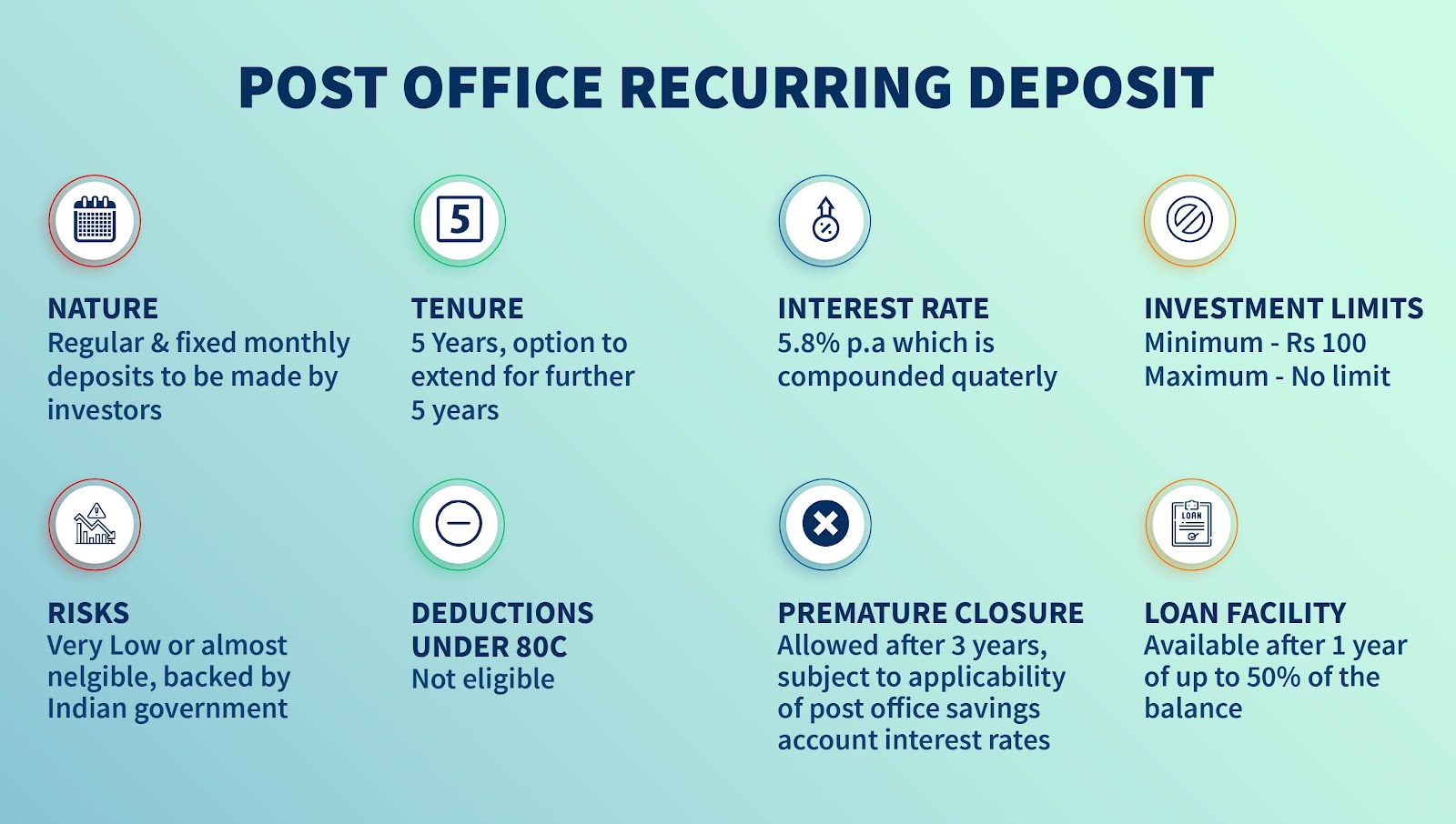

Post Office Recurring Deposits (RDs) scheme is an investment scheme that allows investors to make fixed amounts of monthly deposits for a tenure of 5 years. The investors earn a fixed interest rate of 5.8% p.a. which is compounded quarterly. The capital invested by the depositor is paid back at the time of maturity of the scheme along with the interest earned on deposits.

Eligibility Criteria for Post Office Recurring Deposits

Account in this scheme can be opened by

(i) an adult

(ii) Joint Account (Max. 3 adults)

(iii) Minors above the age of 10 years

(iv) A guardian on behalf of the minor or a person of unsound mind

Account can be easily opened by cash or cheque. In case of cheque, the date of deposit would be the date of clearance of the cheque. And there is no limit on the maximum number of accounts in the post office.

Also Read : Bank of Baroda Fixed Deposit Interest Rates

How to open a Post Office Recurring Deposit Account ?

- Visit your nearest Post Office branch to open a Post Office Recurring Deposit Account

- Ask for the application form and fill all necessary information in the form.

- Submit it along with the required self-attested documents and pay-in slip with the first deposit.

Also Read: Post Office Monthly Income Scheme

Features and Benefits of Post Office Recurring Deposits

Tenure of Post Office RD Scheme

The maturity tenure of the Post Office RD scheme is 5 years which can be extended for further 5 years by submitting an application at the branch.

Interest Rate

The interest rate offered by the Post Office RD scheme is 5.8% per annum which is compounded quarterly. The interest rates are subject to revisions by the government every quarter.

Investment Limits

The minimum amount required to make investments in the scheme is Rs.100 per month or multiples of Rs.10 thereafter. There is no upper limit set for investments.

Taxation

Contributions to Post Office Recurring Deposit accounts are not eligible for claiming tax deductions under Section 80C of Income Tax Act,1961. The interest earned from RD scheme is taxable as per the income tax slab of the investors.

Risks

Since the scheme is backed by the Government of India, it involves very low or almost negligible risks. The chances of capital losses or defaults on interest payments are very low and hence, it is considered to be a very safe mode of investment.

Nomination Facility

Like any other postal savings scheme, investors are offered a nomination facility which allows the account holder(s) to nominate a person to receive payout in case of sudden demise of the account holder(s). This facility can be opted for at the time of opening of the account and also during the tenure of the scheme.

Transferability

Investors are offered a transfer facility that allows investors to transfer the account from one post office branch to another across the country.

Rebate

The scheme provides a rebate facility for investments in this scheme. The rebate is offered on advance deposit of at least 6 installments, which is Rs.10 for 6 months and Rs. 40 for 12 months. The rebate will be paid in the denomination of Rs.100.

Premature Closure

Premature closure is allowed after 3 years from the account opening date, and the interest rate on such a prematurely closed account is payable at the rate applicable from time to time to the Post Office Savings Account.

Loan Facility

The scheme offers a loan facility to the depositors wherein investors can avail a loan of up to 50% of the balance after 1 year, which needs to be repaid in a single shot payment along with the applicable interest rate.

Online Deposit

The scheme allows online deposits by the depositor which can be made through Intra Operable Netbanking/Mobile Banking/IPPB Saving Account.

Also Read : Bank of India FD Interest Rates

Frequently Asked Questions

Q. What is the minimum amount required to invest in Post Office RD ?

A. The minimum investment required for the scheme is Rs.100 per month & in multiples of Rs.10 thereafter.

Q. Is there any maximum amount set to invest in Post Office RDs ?

A. There is no upper limit set to invest in Post Office RDs.

Q. Is there any penalty for delaying the deposit ?

A. If the subsequent deposit is not made until the prescribed day, a default fee is charged for each default, which is Rs.1 for every Rs.100. After 4 regular defaults, the account will be discontinued and can be reinstated in two months, if not revived during the period no further deposits can be made.

Q. What is the prescribed tenure for making a deposit ?

A. Subsequent deposits may be made up to the 15th of the next month if the account is opened before the 15th of a calendar month and until the last working day of the next month if the account is opened after the 16th day and before the last working day of a calendar month.

Q. Is the Rebate Facility provided in this scheme ?

A. Yes, the scheme offers a rebate facility to depositors on their advance deposits.

More Information :

Post Office Saving Schemes for Girl Child

PM Vaya Vandana Yojana

Kisan Vikas Patra Scheme Benefit

Sukanya Samriddhi Yojana Scheme

Kisan Credit Card Scheme

What is Fixed Deposit

Canara Bank Fixed Deposit Interest Rates

Punjab National Bank Fixed Deposit Interest Rates

State Bank of India Fixed Deposit Interest Rates