Post Office Savings Account - Eligibility Criteria, Interest Rate, Benefits & How to Open Account

Updated on July 26, 2022

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

What is a Post Office Savings Account?

A Post Office Savings Account is quite similar to a regular savings bank account. The Post Office Savings Account is a deposit scheme backed by the Government of India which is available in the branches of the post office across the country. It provides returns on the deposits made by individuals at a fixed interest rate set up by the Finance Ministry of the Indian Government. The interest rate currently offered on the PO Savings account is 4% p.a for the Q2 of 2022 which is compounded annually.

Eligibility Criteria- Who can make deposits?

Eligibility criteria set for Post Office Savings Account is as follows:

- A Post Office Savings Account may be opened by any Indian resident adult.

- A joint account with a maximum of 2 adults can be opened. Conversion of joint to a single account is not allowed & vice versa.

- Guardians can open an account on behalf of a minor or a person of unsound mind. In the case of minors, when they attain the age of 18 years, the account needs to be converted in their name by submitting the fresh account opening form.

- A minor above the age of 10 years is also eligible to open an account in his/her name.

- An individual is allowed to open only one single account & a joint account in a post office branch.

How to open a Post Office Savings Account?

- The Post Office Savings account application form is available in all the branches of the post office as well as on the official website of India Post. You can get the application form from your nearest post office.

- This application form needs to be duly filled & submitted along with the required self-attested documents. Upon successful activation, the individual will be able to access the PO savings account and other banking facilities.

- The minimum deposit as required would need to be paid while submitting the application form & documents.

Must Read: Post Office Saving Schemes: Types, Plans, Benefits, Who Should Invest

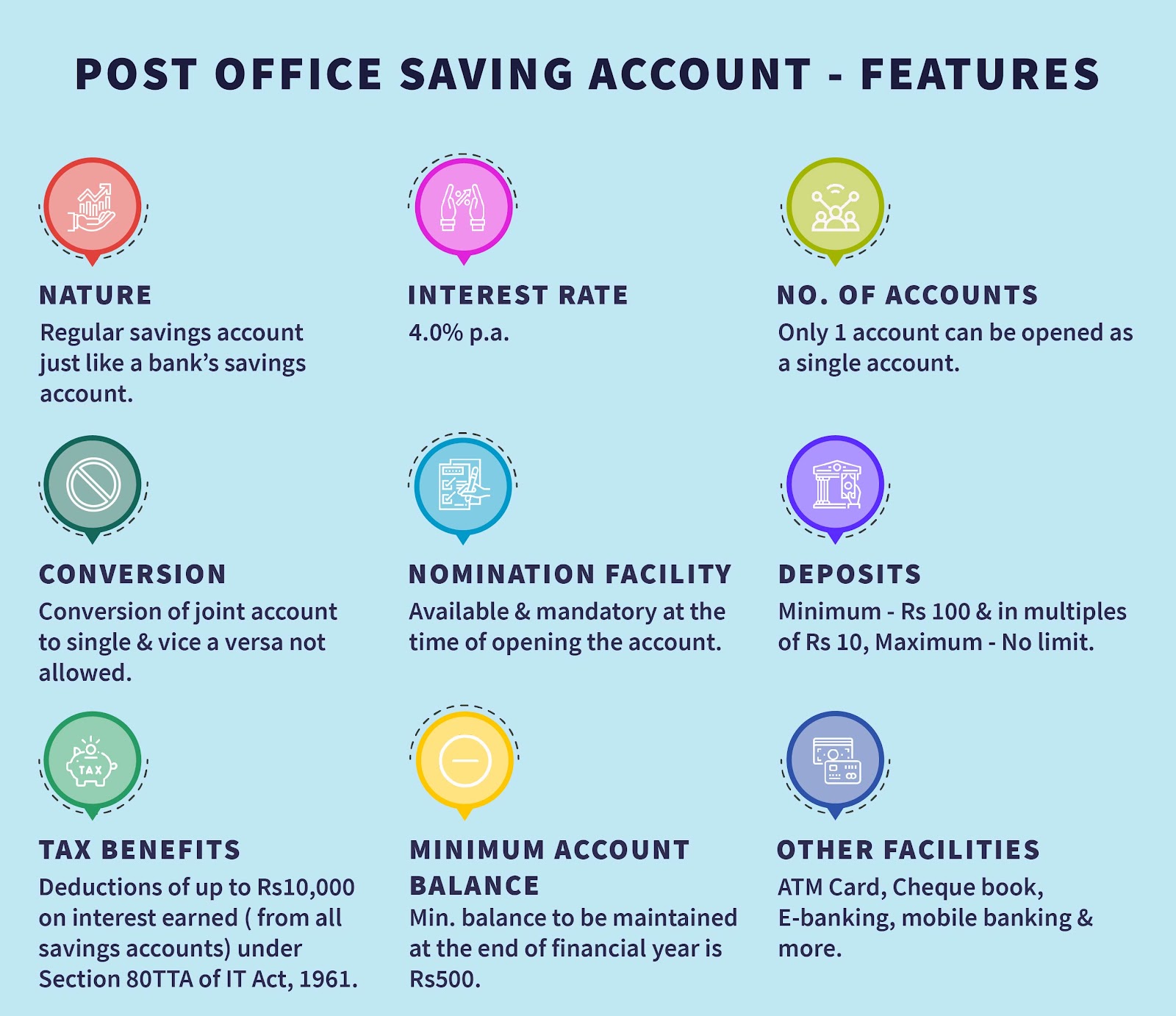

Features & Benefits of Post Office Savings Account 2022

1. Deposits

The minimum deposit to be made while opening the account is Rs.500.

The minimum amount required to make deposits into the Post Office Savings Account is Rs.500. And there is no upper limit for deposits into the account.

2. Minimum Account Balance

The minimum account balance to be maintained at the end of a financial year is Rs.500. If the balance falls below Rs.500 at the end of the financial year, account maintenance fees of Rs.100 will be deducted from the account.

And if the balance becomes zero, the account will be automatically closed.

3. Withdrawals

The minimum withdrawal amount has been set at Rs.50. Withdrawals will not be allowed if they will reduce the account balance below the minimum balance requirement of Rs.500.

4. Nomination Facility

Nomination facility is available in the post office savings account. Also, it is mandatory to add nominees for depositors while opening the account. The nominees are entitled to receive benefits & corpus in account upon the unfortunate death of the depositor.

5. Post Office Savings Account Interest Rate 2022

Post Office Savings Account offers a fixed interest rate of 4.0% p.a. which is compounded annually. This rate is for the 2nd quarter of FY2022-23.

The interest rates are subject to quarterly revisions by the Government of India.

6. Transferability

Accounts can be transferred from one post office branch to another across the country.

7. Tax Benefits

Interest earned by individuals from savings accounts (including all accounts in banks, post offices) are eligible for claiming tax exemptions of up to Rs.10,000 in a financial year under Section 80TTA of Income Tax Act,1961.

8. Silent Account

In case no transactions i.e deposits/withdrawals are made continuously for 3 financial years, the account will be treated as a silent or dormant account.

One can revive that silent account by submitting an application along with the required KYC documents & passbook at the branch.

9. E-banking/ Mobile banking

E-banking or Mobile banking facility can also be availed in the post office savings account by submitting the duly filled application form at the branch. These facilities allow you to have online access into various facilities such as the opening of time deposit/recurring deposit, taking loans against RD or PPF withdrawals, repayment of loans, deposits into various schemes, accessing transaction history & many more.

10. Additional Facilities

Following facilities can also be availed on the post office savings account:

- Cheque book

- ATM Card

- Banking - Internet & Mobile

- Atal Pension Yojana

- Aadhaar Seeding

- Pradhan Mantri Suraksha Bima Yojana

- Pradhan Mantri Jeevan Jyoti Bima Yojana

Service Charge on Post Office Savings Account

| Particulars | Charges |

| Minimum Account Balance not maintained | Rs.100 |

| 1st ATM/Debit Card | Free |

| Subsequent ATM/Debit Cards | Rs.100 |

| Annual Maintenance Charges from 2nd year | Rs.100 |

| ATM PIN generation | Rs.50 |

| Mobile Alerts | Free |

| Doorstep banking | Rs.15 - Rs.35 |

| ATM Monthly Charges | |

| At India Post ATM | Free |

| At Punjab National Bank ATM | Free |

| At other Bank ATM (Metro) | 3 Transaction Free. After that Rs.20 per financial transaction and Rs.8 per non-financial transaction |

| At other Bank ATM (Non-Metro) | 5 Transaction Free. After that Rs.20 per financial transaction and Rs.8 per non-financial transaction |

| Cheque Book | |

| Issue of Cheque Book | Free up to 10 Cheques in a calendar year. Rs.2 per cheque leaf thereafter |

How to withdraw from the Post Office Saving Account?

The minimum amount for withdrawal from Post Office Savings Account is Rs.50. The individuals can only withdraw their deposits after leaving at least Rs.500 in their account, which is the minimum balance requirement. There are 3 ways to withdraw from the post office saving account :

- Post Office Branch: The account holder can visit the nearest Post Office Branch during working hours and fill the withdrawal form. By submitting the filled withdrawal form, the account holder can get the requested cash instantly.

- ATM: The account holder will get the ATM card along with the savings account. By visiting the nearest ATM machine, depositors can anytime withdraw their deposits with the use of an ATM card.

- Cheque: Post office savings account also offers the cheque facility. An account holder can request the cheque book from the post office branch. After getting the cheque book, an account holder can easily withdraw their deposits through cheque or can pay through cheque to any other person, if he/she wants to do the payment.

Frequently Asked Questions (FAQs)

1. How many accounts can be opened in one post office?

Only one account can be opened in a single branch of the post office.

2. What is the lock-in period for the Post Office Savings Account?

There is no lock-in period for the Post Office Savings Account.

3. Is a nomination facility available for the post office savings account?

Yes, a nomination facility is available.

4. Is a transfer facility available for the account?

Yes, one can transfer his account from one branch of the post office to another.

5. What is the interest rate currently offered on the PO savings account 2022?

The interest rate currently offered is 4% p.a. for 2022.

6. What is the minimum balance requirement for a Post Office Saving Account?

The minimum balance required to be maintained in the post office savings account is Rs.500. If the account balance is not raised to Rs.500 at the end of the financial year, then the individual will be charged with an account maintenance fee of Rs.100.

And the account will be closed automatically in case the account balance becomes NIL.

7. Does the post office have an ATM withdrawal facility?

Yes, the Post office provides the ATM facility along with their savings account. An account holder can withdraw their deposits from the nearest IndiaPost ATM or from any other ATM.

8. Is there any maximum deposit limit in the Post Office Savings Account?

There is no maximum limit for deposit in the savings account of the Post Office. The account holder can freely deposit their savings into the account without any limits.

More Information:

PM Vaya Vandana Yojana (PMVVY): Scheme Eligibility, Interest Rate, Process to Apply

National Pension Scheme (NPS )- Tax Benefits, Eligibility, Features, How to Open, Application Form

Kisan Vikas Patra (KVP) Scheme: Benefits, Types, Interest Rates, Eligibility, Calculation

Sukanya Samriddhi Yojana (SSY) Scheme: Benefits, Eligibility, Interest Rate 2020, Application Form

Kisan Credit Card (KCC) Scheme - Eligibility, Interest Rate, Loan, Fee

Senior Citizens Savings Scheme (SCSS): Interest Rate, Eligibility, Benefits, Calculation

Post Office Time Deposit: Scheme Interest Rate, Eligibility, Risks, Calculation

Public Provident Fund (PPF): Interest Rate, Eligibility Criteria, Benefits, Application Form

Employees Provident Fund (EPF): Benefits, Eligibility, Forms, Registration Process

Unit Linked Insurance Plan (ULIP) - Types & Benefits of ULIPs