Post Office Time Deposit (POTD): Scheme Interest Rate, Eligibility, Risks, Calculation

Updated on May 25, 2023

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

Post Office Time Deposit Scheme 2023

Post Office Time Deposit (POTD), also called ‘Post Office Fixed Deposit’ is a great investment scheme which is backed up by the Government of India and is offered exclusively in branches of the Indian Post Office. It is designed to inculcate the habits of savings & investments among the citizens along with offering them risk-free returns on their deposits. Time deposits are offered in tenures of 1-year, 2-year, 3-year, or 5-year. This scheme is considered to be a great and safe mode of investment for those who are seeking investment modes involving low levels of risks.

Post Office Time Deposit (POTD) Interest Rate

The interest rates offered on the Post Office Time Deposits are pretty low as compared to other investments, however being backed by the government, these deposits are risk-free. Rate of interest for the Post Office Time Deposit (POTD) scheme is reviewed by the Ministry of Finance in the beginning of every quarter of the financial year. However, interest is payable yearly. The interest rate for Post Office Time Deposit for different tenures with effect from 1.01.2021 to 31.03.2021 is presented in the following table.

| Tenure | Interest Rate |

| 1-year a/c | 5.5% |

| 2-year a/c | 5.5% |

| 3-year a/c | 5.5% |

| 5-year a/c | 6.7% |

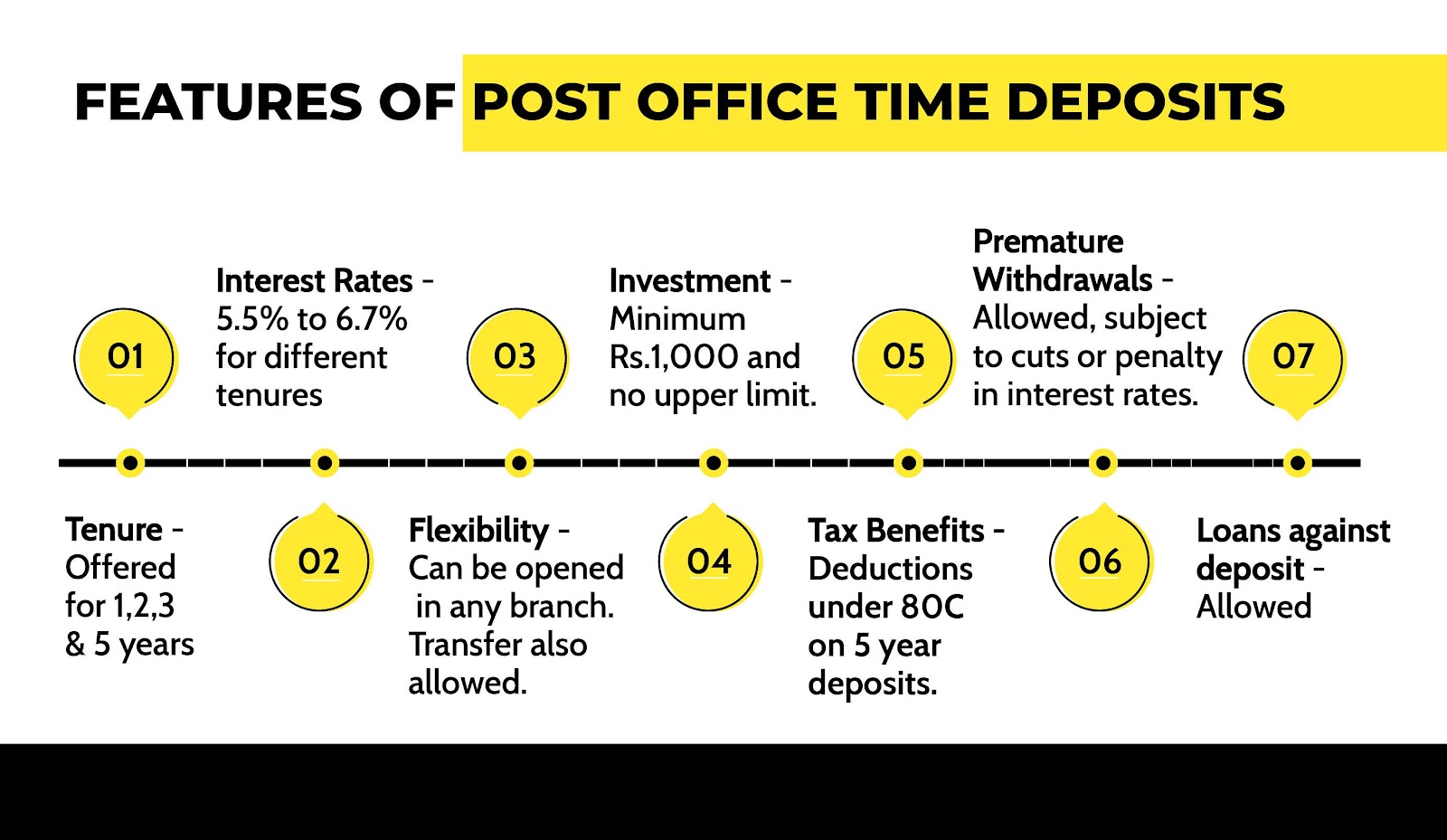

Features and Benefits of Post Office Time Deposit Scheme

Tenure

Post Office Time Deposit (POTD) scheme is offered in four various tenures like 1-year, 2-year, 3-year, and 5-year. Interest rates of this scheme vary with different tenures. The application of certain benefits also varies with different tenures of this scheme.

Flexibility

Post Office Time Deposit (POTD) scheme offers flexibility to the investors. Any number of accounts can be opened by an eligible individual in any branch of the post office. A POTD account can be switched from a single holding account to a joint account as well.

Transfer Facility

Since Post Office Time Deposit (POTD) is a postal savings scheme, it offers a transfer facility among Indian Post Offices. The deposit account can be transferred from one post office to another post office in any part of the country.

Nomination Facility

For the Post Office Time Deposit Scheme, nomination facility is offered at the time of opening the account and is also available after opening the account. This facility allows the account holder to nominate a person while opening the account. The person nominated can claim the proceeds of the deposit account in case of a sudden demise of the account holder.

Tax Benefits

Tax benefits are offered for the Post Office Term Deposit scheme for 5-year tenure, no other POTD scheme for different tenure is eligible for tax benefits. Tax deductions are allowed only on the deposits with 5-year tenure under Section 80C of Income Tax Act of India, 1961. Interest paid is subject to TDS. If there is a case where no TDS is deducted, then it is essential to be declared in the return of income.

Premature Withdrawal Facility

The Post Office Time Deposit scheme offers a premature withdrawal facility under certain terms and conditions. To qualify for using this facility, a minimum six months should have passed from the day of the first deposit. The other important factors concerning premature withdrawal facility are as following:

- For Premature Withdrawal of any tenure of POTD scheme made in the period of 6 months to 1 year from the date of opening the account, interest rate applicable to the PO Savings account is payable.

- For Premature Withdrawal of any tenure of POTD scheme made in after 1 year from the date of opening the account, the applicable rate of interest is 1% lower than original corresponding interest rate.

Maturity

At the time of maturity, the account holder can either withdraw or renew the account for the same tenure. Maturity proceeds which are not drawn are eligible for savings account rate of interest for a maximum tenure of two years.

Investment

The minimum amount required to open an account in the POTD scheme is Rs. 1000 & in multiples of Rs. 100 thereafter. However, there is no upper limit set upon investment.

Liquidity

Post Office Time Deposit is considered liquid, even with lock-in. An account holder is allowed to borrow against deposits or can avail premature withdrawal facility under certain conditions.

Also Read: What is Fixed Deposit

Risks Involved

In the Post Office Time Deposit scheme, there are very low levels of risks involved as this scheme is backed up by the Government of India. However, there are certain provisions which investors willing to invest into this scheme should take note of.

Investment Safety

The investments under Post Office Time Deposit (POTD) scheme are fully protected and returns from this scheme are guaranteed since the scheme is backed up by the Government of India.

Inflation

When it comes to inflation, the POTD scheme is not that safe. There is no provision of protection from inflation for this scheme which may make matters worse by making investors earn no real returns from this scheme if inflation hits higher than the guaranteed rate of interest. Therefore, there will always remain a possibility of returns to get affected by inflation.

Also Read : Indusind Bank FD Interest Rate

Eligibility Criteria

Eligibility criteria for opening an account in Post Office Time Deposit scheme is as follows:

1. Any Indian Citizen over the age of 18 years is eligible.

2. A minor over the age of 10 years is eligible for opening and managing an account.

3. A parent or guardian can also open an account on behalf of a minor or person with an unsound mind.

However, certain institutions or sections of people are not eligible to apply for this scheme as mentioned below:

1. Non-Resident Indians (NRIs) are not eligible.

2. Trust funds, Regimental funds, welfare funds, or any institutional account holders are also not eligible for this scheme.

3. Hindu Undivided Families (HUFs) are not eligible for this scheme.

Who should apply for the Post Office Time Deposit account?

Post Office Time Deposit (POTD) is a great scheme for those investors who are very conservative about their money and its safety. Also, those investors who are seeking out good alternatives to fixed deposit schemes offered by banks can consider investing in this scheme. Eligible citizens living in rural or remote areas can also look at this scheme as it can be availed in any of the Indian post office branches. For investors who tend to move frequently due to personal reasons in the country can also look at this scheme as it features a convenient transfer facility which allows one to transfer an account from one post office to another within the country. Children above the age of 10 years can also be encouraged to apply to this scheme.

Also Read : Kotak Bank FD Interest Rates

How to apply for a Post Office Time Deposit account?

Any eligible person can apply for this scheme either offline or online.

Via Offline Mode:

For anyone interested to apply for this scheme offline, certain steps need to be taken:

1. Visit the nearest post office branch.

2. Certain documents are required for applying which are:

- Proof of identity and proof of address. For example, any of the following documents can be presented as proof for each requirement: Aadhar Card, copy of passport,

- PAN Card, or declaration in Form 60 or 61 as per Income Tax Act, 1961, driving license, Voter’s ID, ration card & others.

- Passport size photographs

- Deposit Opening Form (duly filled)

3. Ask an official about the scheme and a concerned official shall be provided to guide you further through the process.

Via Online Mode:

Anyone can apply for this scheme online as well through options like mobile banking and Intra operable net-banking. Certain documents may be required.

Certain steps are required to be taken:

- Log in to the Post Office e-banking site with registered User ID and password.

- Click on General Services.

- Click on ‘Service Request’

- Choose the Time-Deposit opening request and proceed further.

About Opening an Account

Account in this scheme can be opened in various ways such as:

- A single account can be opened.

- A joint account can be opened which has an upper limit of 3 adult account holders.

Accounts in this scheme can be opened via depositing through cash/cheque. In the case of opening an account under this scheme through a cheque, the date of realization of cheque in the Government account would be the date of the account opening.

Post Office Time Deposit vs Bank Fixed Deposit

There are not many differences between a Post Office Time Deposit and a Bank Fixed Deposit:

Tenure:

Bank fixed deposits are more flexible than Post office Time Deposits in terms of tenure. Bank Fixed Deposits tenure can vary from 7 days to 10 years whereas Post Office Time Deposit is offered for a tenure of 1,2,3 and 5 Years.

Interest Rate:

Post Office Time Deposits offer a slightly higher rate of interest in comparison to Fixed Deposit with Banks.

Senior Citizens Interest Rates:

Post Office Time Deposits don’t offer any additional interest rates to senior citizens while Bank Fixed Deposits offer additional interest rates on fixed deposits. The additional interest rates for senior citizens in bank fixed deposits can vary from Bank to Bank.

Premature Withdrawals:

Both Banks & Post Offices offer the facility of premature withdrawals to depositors. However, they usually charge a penalty on interest rates to offer such a facility. The penalty rates vary across institutions & as per term of deposit.

Tax Saving:

The deposits with a maturity period of 5 years or more in Bank Fixed Deposits and Post Office Time Deposits are eligible to claim tax deductions under Section 80C of the Income Tax Act, 1961. Both offer the deductions on the deposit amount of up to ₹1.5 lakh per financial year.

Must Read : Shriram Finance Transport FD Rates

Post Office Time Deposit vs Other Post Office Saving Schemes

| Particulars | Post Office Time Deposit Account | Senior Citizen Saving Scheme Account | National Saving Certificate (NSC) | Post Office Monthly Income Account |

| Interest Rate | 5.5% p.a. to 6.7% p.a. (Vary With Tenure) | 7.4% p.a. | 6.8% p.a. | 6.6% p.a. |

| Tenure | 1 Year to 5 Years | 5 Years | 5 Years | 5 Years |

| Minimum Investment | ₹1000 | ₹1,000 | ₹1,000 | ₹1,000 |

| Maximum Investment | No Limit | ₹15 Lakhs | No Limit | ₹4.5 Lakhs |

| Taxability | Interest earned is taxable and is subject to TDS. The 5 Years PO Time deposit is eligible for claiming tax deductions of up to ₹1.5 lakh under section 80C of the IT Act. | Interest earned is taxable & subject to TDS. Tax Deductions on the deposit can be claimed of up to ₹1.5 lakh in a financial year under section 80C of the IT Act. | Tax Deduction on the deposits can be claimed of up to ₹1.5 Lakh under section 80C of the IT Act. Interest earned is taxable as per the income tax slab rate of investors. | Interest earned is taxable as per the income tax slab of investors. |

Frequently Asked Questions About Post Office Time Deposit

Q. What is the investment process of Post office time deposit (POTD) ?

A. Post office time deposit : An Individual who is above the age of 10 can open a time deposit account at any post office. Also Guardians can open an account on behalf of a minor.

Q. Is POTD Taxable ?

A. According to the Income Tax Act 1961, Interest Rates on FDs is treated as 'income from other sources' and hence, is fully taxable. The FD interest earnings are included in your gross annual income and the tax liability is estimated, following the prevalent tax laws.

Q. What are the minimum and maximum investment requirements for the Post Office Time deposit?

A. Post office Time Deposit account can be opened with Rs. 1,000 and there is no upper limit for the investment.

Q. What are the interest rates for the Post Office Time Deposit?

A. The interest rate varies with the tenure of the deposit. The above interest rate table can be referred to know the interest rate for different tenures. The Post Office FD interest rates are in the range of 5.5% to 6.7%.

Q. Do Post Office Time Deposits offer tax deductions under Section 80C?

A. The Deposits made for 5 years are eligible for claiming tax deductions of up to ₹1.5 lakh per financial year under Section 80C of the Income Tax Act, 1961.

Q. Does the Post Office Time Deposit account allow premature withdrawals?

A. Yes, the deposits can be prematurely withdrawn but after 6 months from the date of deposits. And, also after paying the penalty for the premature withdrawal of deposits.

Q. Can a Time deposit account be opened online?

A. Yes, a Post Office time deposit account can be opened online but for that, you need to have a savings account with the Post Office and the credentials for net banking or mobile banking.

Q. What are the documents required to open a Post Office Time Deposit?

A. You need to have the following documents:

Proof of identity and proof of address.

PAN Card, driving license, Voter ID card or ration card.

Passport Size Photograph.

More Information:

SBI Fixed Deposit Interest Rates

Indian Post Office Saving Schemes

Sukanya Samriddhi Yojana Scheme