Public Provident Fund (PPF): Interest Rate, Eligibility Criteria, Benefits, Application Form

Updated on October 7, 2022

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

Public Provident Fund (PPF)

Public Provident Fund (PPF) is a popular investment scheme which is backed by the government of India. The Public Provident Fund scheme was launched by the National Savings Institute of Finance Ministry in 1968. This investment scheme has been considered a breakthrough ahead of other schemes available in the market. Public Provident Fund is a long-term investment. This scheme offers investors a steady stream of income through high and guaranteed returns. This scheme has aimed to facilitate citizens in making small savings and has been successful for years in doing so.

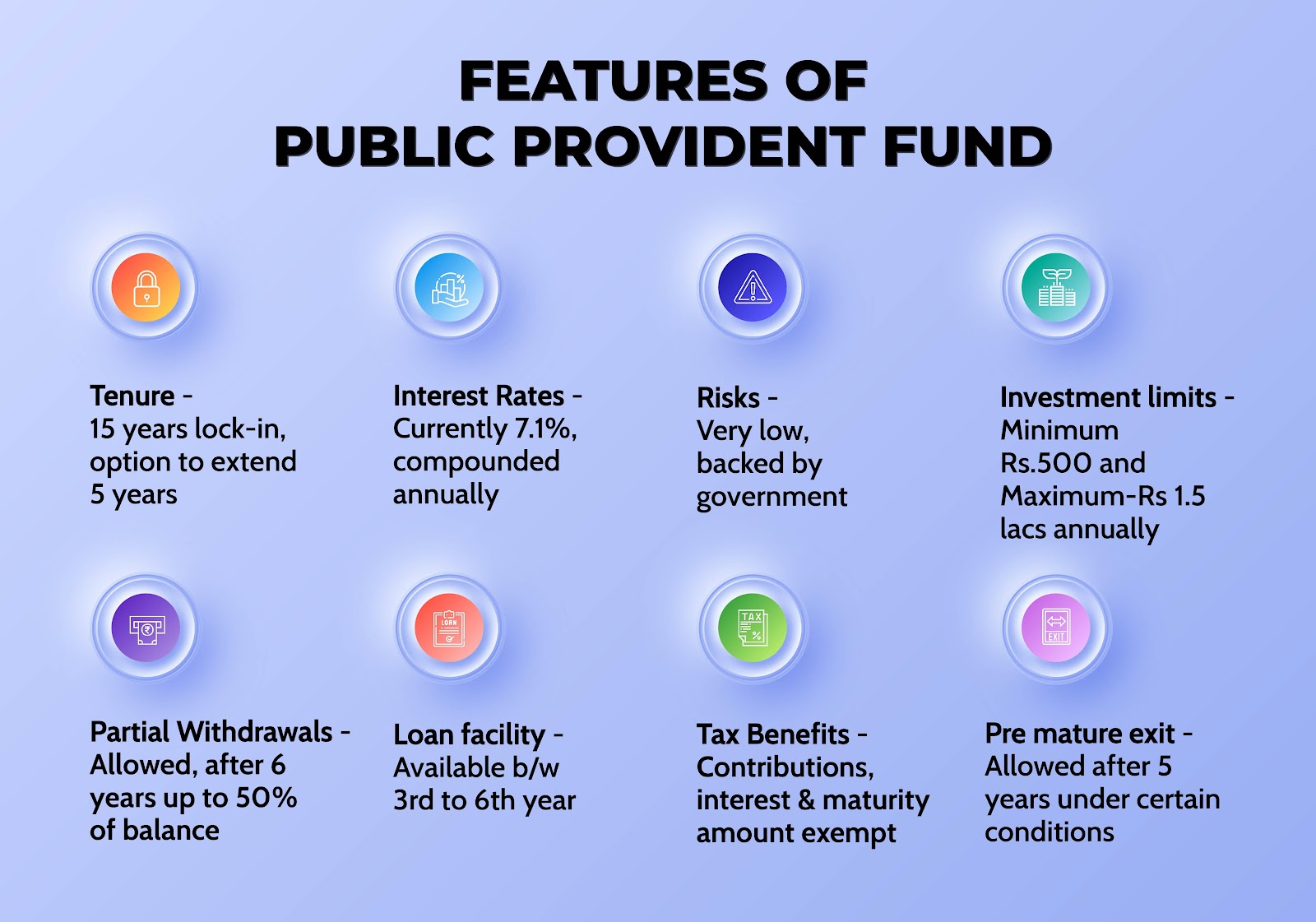

Features and Benefits of PPF

PPF has many great features and benefits. The primary features and benefits of PPF are mentioned below:

Tenure of investment

Public Provident Fund is a long-term investment with a lock-in term of 15 years. There is also an option to extend the tenure by 5 years after the termination of the 15-year lock-in term.

Loan Facility

This scheme offers the benefit to avail loans against the investment. Loan can only be granted from the third year till the end of the sixth year from the time of account activation. It is important to note that the maximum amount that can be claimed for the purpose is 25% of the balance left in the financial year of the year preceding the year when loan was applied for. The maximum term of loans against PPF is 36 months. As per the revised rules in December 2019, the loans taken against the PPF account will be charged an interest rate of 1% p.a. instead of the earlier charged rates which was 2%p.a.

Tax Benefits

Investments made in an account under this scheme are classified as Exempt-Exempt-Exempt (EEE) category in terms of taxation. Hence, all deposits made under this scheme are deductible under Section 80C of the Income Tax Act of India, 1961. During the time of withdrawal, the amount accumulated along with the interest amount in the PPF account is also exempted from tax.

Nomination Facility

Account-holders under this scheme are able to assign a nominee for his/her account during the time of opening the account or later. Account holders cannot nominate any trust for his/her account. This scheme allows account holders to nominate more than one person. Account holders have to mention the percentage of stake if there is a case of more than one nominee. Nominees receive the ownership rights in authoritarian terms to receive a corpus in the case of the sudden demise of the account holder. In the case of accounts opened on behalf of minors, a nomination facility is not provided in the scheme.

Transfer Facility

For the PPF scheme, it is easy to transfer accounts opened from one post office to any other post office or across branches of a bank located anywhere in the country easily.

Risk-Free Investment

PPF scheme is backed by the government of India and therefore, provides a guarantee on the investment as well as the returns to the investors. Given its risk-free nature, investments in the PPF account are perfectly suitable for risk-averse investors.

7. Interest Rates

Interest rates of the PPF scheme are usually higher than the other small savings schemes available in the market which assures higher returns to investors. The scheme currently offers an interest rate of 7.1% p.a. which is compounded annually. The rate of interest on the PPF account is set by the Ministry of Finance and is subject to revisions by the central government quarterly.

8. Limits on investments

Lower limit set or minimum amount of investment that can be made to account under the PPF scheme is Rs. 500 per year and upper limit set or maximum amount of investment that can be made to account under the PPF scheme is Rs. 1.5 Lakh in a financial year. The maximum contributions that can be made during a financial year into the PPF scheme is 12 times(monthly). Deposits can be made in the lump sum amount or in installment mode.

9. Premature/Partial Withdrawal Facility

Premature partial withdrawal in this scheme can be made after the completion of 6 financial years from the date of opening the account. After 6 years, funds in this facility are available for withdrawal under certain terms and conditions each year. One can withdraw up to 50% of the available balance at the end of the fourth financial year or the balance in the immediately preceding year, whichever is lower. For each year, only one partial withdrawal is permitted. The amount withdrawn under this facility is exempted from tax. Verification of certain documents is required before availing this facility.

10. Premature Exit Facility

An account under the PPF scheme is entitled to premature exit facility after the completion of 5 financial years under certain terms and conditions which are mentioned below:

- This facility is available under the grounds of critical illness treatments of the account holder or their family members, higher education purposes, etc. Certain documents are required to be presented in support of the reasons provided to avail of this facility.

- 1 percent interest will be deducted from the valid rate of interest on PPF account for premature exit from the scheme.

11. Accounts and Deposit modes

One person is entitled to open only one account under the PPF scheme. Also, Joint accounts cannot be opened under the scheme. However, one can open another PPF account on behalf of the minor. Investors can make deposits in PPF account via different modes such as online transfer, demand draft, cheque, or cash.

12. Liquidity

The PPF scheme offers low levels of liquidity as the scheme has certain terms & conditions for availing loan facility and partial withdrawal facilities.

Also Read: ELSS VS PPF

Risks

As mentioned earlier, PPF scheme involves zero or minimal risks. PPF as a mode of investment can witness default risk which means risk allied to a default of the government on its failure to pay back the investments of investors, but the chances of such situations are almost negligible. PPF scheme is also prone to reinvestment risk which means risk allied to reinvesting in this scheme due to the difference in interest rate as the interest rates are subject to revisions every quarter.

Eligibility Criteria and Who should Apply?

There is an eligibility criterion set for the PPF scheme. Any Indian resident citizen can open an account under the PPF scheme. There is no age limit set for eligibility. Parents or guardians can open accounts under this scheme on behalf of minors. National Resident Indians (NRIs) and Hindu Undivided Families (HUFs) are not eligible to open an account under this scheme.

Any Indian resident who is conservative about investments and has low-risks tolerance should consider investing in this scheme. Citizens who have to move a lot and have an itinerant lifestyle and are looking to invest can find this scheme suitable for themselves as it offers a transfer facility.

How to Apply for PPF account?

If you’re eligible and are willing to invest in this scheme, you can proceed to apply to this scheme and visit the nearest bank or post office and enquire more about this scheme. There are certain documents required to apply for opening a PPF account as mentioned below:

1. The application form

2. Proof of Identity such as Aadhar Card, Permanent Account Number (PAN) card, passport, etc.

3. Proof of Address

4. Signature proof

Inactive PPF Account Reactivation

If there is a case when a minimum contribution of Rs. 500 is not made in a year, the account may become inactive. Mentioned below are steps to revive an account:

1. There is a requirement of a written request for reactivation of an account which is to be submitted to the post office or branch of the bank where the account has been opened.

2. There is a fine of Rs. 50 for every year the account remains inactive.

3. The undeposited minimum amount of Rs. 500 for the whole tenure the account has stayed inactive needs to be paid. The minimum contributions for each financial year needs to be settled for reactivating the account.

Checking balance of PPF Account

The checking of the balance in the PPF account can be done via online mode or offline mode through certain steps.

Online Mode:

Online mode option is currently available only for those PPF accounts that are opened with relevant banks.

1. There is a requirement to have activated internet banking with a linked bank account.

2. Log in via net banking User ID and password in order to check details of PPF account.

3. After logging in, PPF account status and balance can be checked, and furthermore, funds can also be transferred to the PPF account. One can also set up standing instructions for the PPF account, download the PPF account statements, submit PPF loan applications, etc.

Offline Mode:

a. For PPF account in an authorized bank:

1. PPF account status can be checked by simply visiting the branch of the bank where the account has been opened. A passbook is provided while opening the account under this scheme which contains specific details like PPF account number, bank branch details, PPF account balance, transactions, etc.

2. One can get his PPF account passbook updated occasionally by visiting the branch of the bank.

3. Once the passbook is updated, there will up-to-date details of all transactions and including the current PPF account balance.

b. For PPF account in post office:

1. While opening a PPF account, a PPF account passbook is provided that contains important details such as PPF account number, transactions done, current balance, etc.

2. One can get a PPF account passbook updated by visiting the relevant post office in order to check the balance in the PPF account.

FAQs

Q. Can transfer take place online for PPF account ?

A. Yes, transfer of money can take place online in the case of a PPF account opened with a bank.

Q. Can multiple accounts be opened for one person in this scheme ?

A. No, only one account can be opened for one person under PPF scheme.

Q. What is the minimum amount considered to open an account in this scheme ?

A. Minimum amount set to open an account under this scheme is Rs. 500.

Q. What is the age criteria set for opening an account under this scheme ?

A. There is no age criteria set for opening an account under this scheme.

Q. Can NRIs open an account under the scheme ?

A.No, NRIs cannot open an account under PPF scheme.

Q. What is the tenure of the PPF scheme ?

A. The tenure of the PPF scheme is 15 years.

Q. Can money be transferred in PPF account through BHIM app ?

A. Yes, money can be transferred in PPF account through BHIM app.

More Information:

Bank of Baroda FD Interest Rates

Bank of India FD Interest Rates

Punjab National Bank FD Interest Rates

State Bank of India FD Interest Rates