RD vs SIP - Risk, Returns, Benefits, Tenure, Comparison, Which is Better Investment

Updated on June 27, 2024

Written by Manish Kothari

CEO Zfunds

Share

Get Investment Advice from India's Top Experts

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

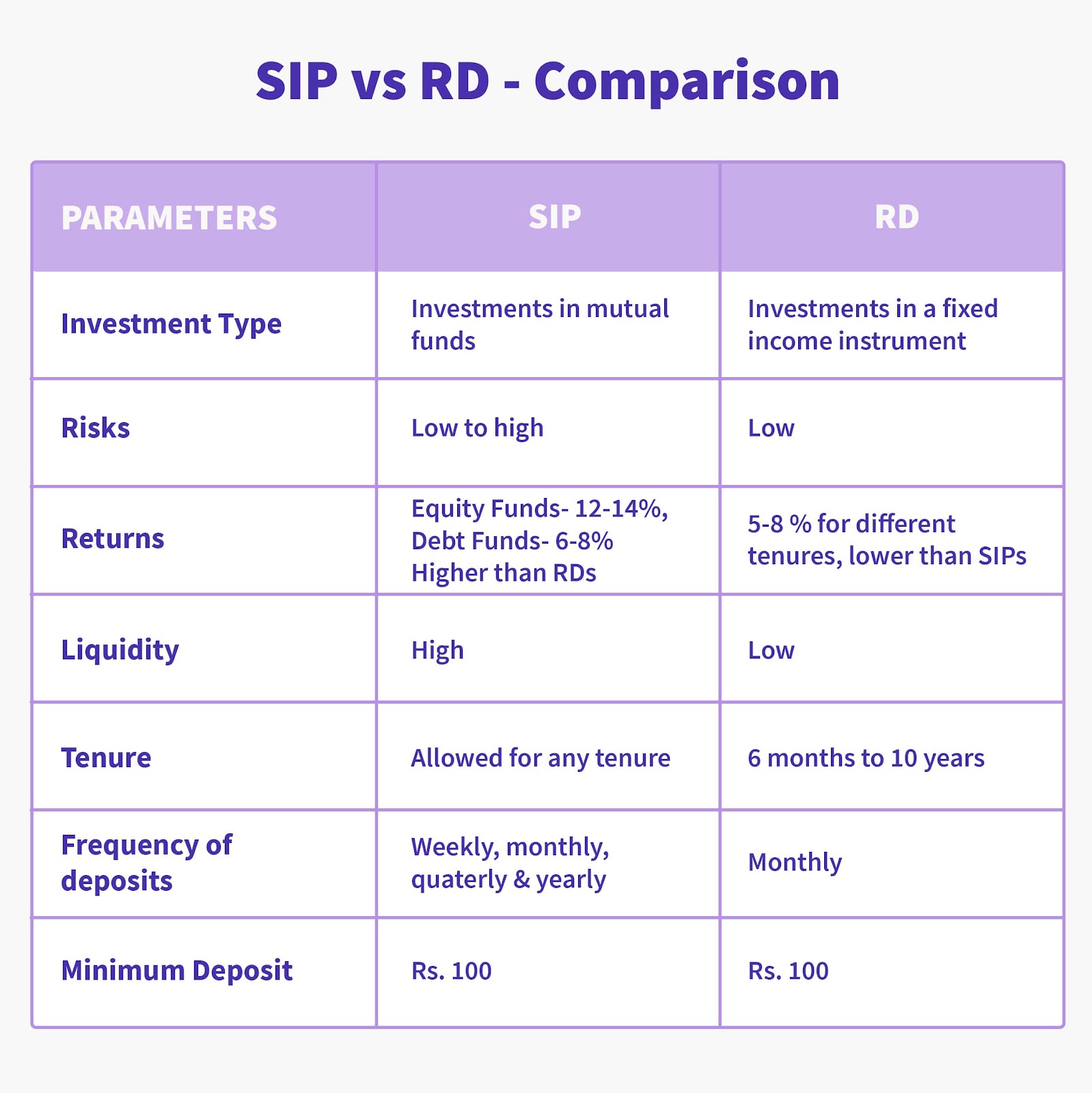

Difference Between SIP and RD on various important parameters

| Parameters | SIP | RDs |

| 1. Investment Type | Investments in mutual funds. | Investments in a fixed income instrument. |

| 2. Risks | Low to High | Low |

| 3. Returns | Equity Funds- 12-14%, Debt Funds-6-8%. Higher than RDs. | 5-8% for different tenures. Lower than SIPs. |

| 4. Liquidity | High | Low |

| 5. Tenure | Allowed for any tenure. | 6 months to 10 years |

| 6. Frequency of deposits | Weekly, monthly, quarterly & yearly. | Monthly |

| 7. Minimum Deposit | Rs.100 | Rs.100 |

What is Recurring Deposit ?

Recurring Deposit (RD) is a type of term deposit where the investors make fixed amounts of deposits every month for a specific tenure. It is offered for periods ranging from 6 months to 10 years. The recurring deposits are very popular among investors for its various benefits like being a low-risk investment, flexibility of term, offering good interest rates, facility of premature withdrawals, etc. Recurring deposit schemes in India are offered by various public & private banks, post offices & other financial institutions. While depositing with NBFCs may offer better returns, most banks carry lower risks.

Features of Recurring Deposit (RD)

Tenure of Investment

Recurring Deposits (RD) have investment tenures in the range of 6 months to 10 years, depending upon the offering institution.

Rate of Interest

The rate of interest offered on RDs varies across offering institutions. Also, the interest rate is different for varied investment tenures.

Premature Withdrawal

Withdrawal from this account is allowed only after it attains maturity. However, if you choose to withdraw the amount before the maturity period, it attracts a premature penalty which varies across banks.

Loan Availability

There is also an option to avail a loan against RD. Banks may allow up to 95% of the deposit amount as a loan against deposit used as collateral.

Risks

Recurring Deposits (RDs) involve low levels of risks and is considered to be one of the safest modes of investment. However, it is very important to consider the credit ratings of the institutions in case of depositing with NBFCs.

Partial Withdrawal Facility

Banks do not offer a partial withdrawal facility for Recurring Deposit (RDs). However, post offices do offer a partial withdrawal facility in which a loan of up to 50% of the balance is allowed after 1 year subject to minimal interest, which needs to be paid back in a single shot payment. The interest rate will be applicable as per the prescribed rates at the time of withdrawal.

Also Read: What is Fixed Deposit

What is Systematic Investment Plan (SIP) ?

A Systematic Investment Plan (SIP) is a way of investment offered by mutual funds to the investors in which they can make fixed investments at periodic intervals instead of making a lumpsum investment. This way SIPs help to make small contributions for investments as per the investor’s needs & provides a disciplinary approach of investing which could help meet financial goals.

Also Read : Canara Bank FD Interest Rates

Features of Systematic Investment Plan (SIP)

Compounding Effect

When you make investments through SIP and contribute for a long tenure, the SIP benefits are amplified by the compounding effect. The compounding effect ensures that you also earn returns on the returns made on the investment. This way over the long term, an investor is able to build a large corpus for meeting his/her requirements

Rupee Cost Averaging

SIP is known to enable investors to lower down their average cost of investments and cut down the risks linked with market volatilities by being able to invest periodically across the market conditions. This concept is known as rupee cost averaging.

Minimum Investment Requirements

SIPs allow investors to make a minimum investment of as low as Rs. 100 or 500, depending upon the schemes..

Meeting Long Term Goals

SIPs can help to meet long term financial goals through a disciplinary approach of regular savings & investments for a long tenure. SIPs can be planned as per the investor’s requirements, financial goals & time horizon to reach the goals.

Comparison between Recurring Deposit (RD) and Systematic Investment Plans (SIP)

Risks

RDs usually involve lower levels of risks as compared to mutual funds and hence, are suitable for investors with a low-risk appetite. Not all RDs carry low risks, like the ones offered by NBFCs and other financial institutions can be risky and require a thorough inspection of their credibility on the part of investors.

Whereas in SIPs, different mutual fund schemes carry varied risk-return characteristics. A broad universe of mutual fund schemes across asset classes & their sub-categories offers products for all types of investors.

Liquidity

RDs are considered to offer lower levels of liquidity. Withdrawals from the RD account is allowed only after it attains maturity. However, if you choose to withdraw the amount before the maturity, it would attract penalties or interest rate cuts.

Whereas SIPs comparatively offer higher levels of liquidity by allowing investors to exit from the mutual fund schemes anytime except for the ELSS funds. However, the schemes may carry some exit loads if withdrawn before a specified time period.

Also Read: Best ELSS Funds to Invest in India

Investment Tenure

RD is available for a tenure of 6 months to 10 year period. Whereas, SIPs do not have any specific period for investing and can be continued for any time period.

Interest Rates of RD and SIP

RDs have a fixed interest rate associated with them while SIPs do not have any fixed interest rate. The rate of interest of SIP depends on the market conditions & performance of the fund’s underlying securities in the market.

RDs have an interest rate of 3.5% to 6.5% which varies with the tenure of the RD. Generally, the RD interest rate is lower than the returns expected from the SIP of similar tenure. However, the return will depend upon the chosen fund & asset class for investment. On long-term investments, SIPs can offer returns anywhere between 6% to 12%, depending upon the mutual fund selected.

Also Read : Bank of India Fixed Deposit Interest Rates

Frequently Asked Questions

Q. What is the minimum deposit amount of the RD and SIP?

A. The deposits in RD can be done with a minimum amount of Rs. 100, however, the minimum amount varies across institutions. The minimum required in SIPs varies from fund to fund. However, the minimum amount of SIP starts with an amount as low as Rs.100.

Q. Do the RDs and SIPs have the lock-in period?

A. RD has a lock-in period that varies from 6 months to 10 years. The investor in RD can select the tenure for the deposits as per their financial goals. While there is no lock-in period in the SIP except for ELSS funds, an investor can continue the investment in SIP as long as they want.

Q. What are the returns offered by the RD and SIP?

A. RDs offer a fixed rate of interest which varies with the investment tenure. The interest rate for RD varies from 3.5% to 6.50% while SIPs do not have a fixed rate of interest. the returns on mutual fund investments are market-linked.

Q. What is the risk profile for RD and SIP?

A. RD has a low-risk profile as it is a fixed income instrument while in the case of SIP in mutual funds, the risk profile can be low to high risk depending upon the chosen fund.

Q. Do the SIPs offer a loan facility like RD?

A. No, SIPs do not offer a loan facility like RD. However, mutual fund investments offer high liquidity to investors as investments can be withdrawn anytime as per requirements.

More Information:

Difference between SIP and Lumpsum

ELSS VS PPF Tax Benefits

ELSS vs ULIP

Difference between Direct and Regular Mutual Funds

National Pension Scheme Benefits

Post Office Saving Schemes