Unit Linked Insurance Plans

Updated on July 21, 2023

Written by Manish Kothari

CEO Zfunds

Share

Rs.3 Lac ka Cover at Just Rs.390/Month*

By clicking on button you agree with and

Get Updates on WhatsApp and SMS

Unit Linked Insurance Plans

Unit Linked Insurance Plan (ULIP) is a type of life insurance plan which is multifaceted in nature and provides an opportunity to invest along with an insurance cover. ULIP was initially presented in our country by Unit Trust of India (UTI) in 1971. While investing in ULIP, the insurance company invests a portion of the amount of premium into different types of investment instruments like equities, bonds, money market instruments etc. The balance of the premium is used in offering the insurance coverage. ULIPs also provide certain benefits and hassle-free management for keeping the record of investments.

Types of ULIPs

There are different types of ULIPs available in the market. ULIPs are classified on the basis of the purpose that they serve.

For funding child’s education

Some ULIPs help investors save to fund their child’s education. These plans are suitable for parents who are looking for options to save for their child’s future. Many of these ULIPs also help in providing money for important events occurring in their kid’s life.

For wealth collection

Some ULIPs are aimed to help investors to start saving and accumulate a great amount of wealth for the future. People who have any kind of financial aim to attain in future can look at these plans as an option. There are many plans which help in wealth creation and give good returns on investments.

For health benefits

Some ULIPs help in providing any monetary assistance in the times of healthcare or medical emergencies of investors. Riders are also available specifically to cover major problems concerning health. At times of visiting hospitals or medical institutions, such plans can help in relieving one from stress of bills and charges.

For retirement

Some ULIPs help investors plan the flow of money during their lives as per requirement. One such event in life that can be planned through ULIPs is retirement. Once a person retires, there is no regular income, so it is very important to sort out financial plans for retirement to live a stress free life later.

On the basis of ULIPs investments:

Equity Funds

Some ULIPs invest a portion of the amount paid as premium by the investor in equity and stocks. These plans involve a higher level of risk.

Cash Funds

Some ULIPs invest the premium paid by investors in cash funds. Cash funds imply that the amount gets invested in cash, money market instruments, bank deposits, etc. These funds are also called money market funds. These plans hence involve lower levels of risk.

Debt Funds

Some ULIPs invest the premium paid by investors in debt funds. It gets invested in debt instruments like corporate bonds, fixed income instruments, government securities, etc. These funds involve a moderate level of risk.

Balanced Funds

Some ULIPs invest premium paid by investors in both equity and debt in order to reduce the levels of risk involved for investors. These balanced funds are also called hybrid funds. These are considered to be a very sensible type of investment considering the stability and promising results.

On the basis of death benefit:

Type 1 ULIPs

In Type 1 ULIPs, if sudden demise of the life insured takes place, the nominee receives higher of the sum value assured or fund value from the insurance companies. In this type, mortality charge is usually seen decreasing annually.

Type 2 ULIPs

In Type 2 ULIPs, in case of sudden demise of the life insured takes place, the nominee receives the sum value assured along with the fund value from the insurance companies.

On the basis of premium:

Single Premium

These ULIPs offer investors to pay a one-time amount as premium during the start of the plan.

Regular Premium

These ULIPs offer investors to pay premium at regular intervals like monthly, quarterly or annually.

On the basis of guarantee:

Guaranteed ULIPs

These ULIPs offer guaranteed benefits which are usually for longer periods of time. These plans also involve lower levels of risks.

Non-Guaranteed ULIPs

These ULIPs don’t make any promises and usually provide a variety of investments for choice.

Features of ULIPs

Some of the features of ULIP plans include:

Flexibility

ULIPs provide high flexibility to policyholders in terms of having a choice to switch between different funds according to varying requirements. There are different types of funds like equity funds, cash funds, etc. to choose from.

Liquidity

ULIPs offer very limited and low liquidity. Liquidity usually depends on insurance companies that offer plans.

Life Cover

ULIPs provide life coverage along with investments to the policyholders and provide security. Life coverage is provided by ULIPs that offer a variety of choices so a person can select on the basis of financial capabilities.

However, these plans generally offer low coverage to the policyholders and levy extra charges for increasing the coverage amount which lead to high costs.

Transparency

ULIP Plans have very low transparency. It becomes very difficult to find information about the plans regarding its investments, structure, holdings etc.

Tax benefits

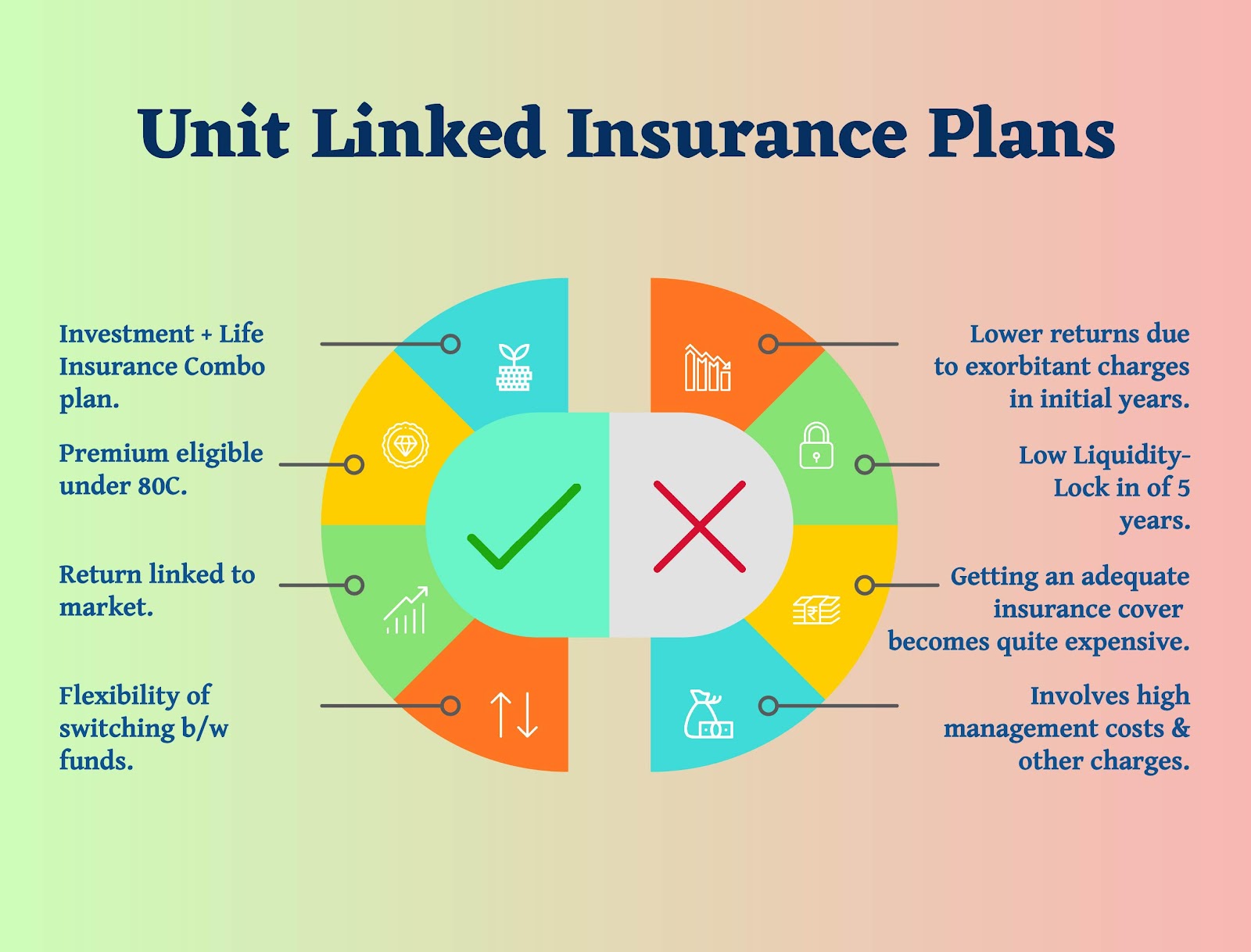

Premium paid for ULIPs is eligible for tax deductions of up to Rs.1.5 Lacs under Section 80C of Income Tax Act, 1961. Maturity benefits of ULIPs are exempt from taxes under section 10(10D) of IT Act,1961 on certain conditions. Hence, ULIPs offer many tax benefits.

Returns

The returns from ULIP plans vary across different funds like equity, debt, cash & balanced as per the choices made by the investors for investments. However, the returns offered by Ulip plans are generally lower than the other investment products like mutual funds, stocks because of their high-cost structures, especially in the initial years of the plan.

Long term investments

ULIPs is an option for longer-term investments.

Risk Involvement

There are a variety of funds to choose in ULIPs and hence risk levels also vary. ULIPs can be considered by investors with any level of risk tolerance.

Death Benefits and Maturity Benefits

Death benefits are provided by ULIPs in case of sudden demise of policyholders. Depending upon the cause of death, death benefits may differ. Maturity benefits are provided by ULIPs when the policy gets matured or passes the maturity period.

Lock-in Period

ULIPs usually have a lock-in term of 5 years.

Premature Withdrawal

Premature Withdrawals from ULIPs are allowed before the lock-in period. However, money is paid back to the policyholders only after the completion of 5 years. Also, the plans levy heavy discontinuance & other charges due to which the policyholders have to suffer significant cuts on their accumulated investments.

Withdrawals after the lock-in period are allowed subject to charges as per the plan terms.

Eligibility for ULIPs

Eligibility criteria usually varies from policy to policy on the basis of minimum and maximum limit set for age, ability to pay premium. Usually, minimum age to be eligible is set to be 18 years and maximum age is usually set around 70-75 years.

Read more : NISM Certification Exam

How to Apply for ULIPs?

There are certain documents required to apply for ULIPs which are mentioned below:

Age Proof

Documents like driving license, passport, voter’s ID, etc. are needed as a proof for age.

Identity Proof

Documents like PAN Card, Aadhar Card can be used as proof for identity.

Address Proof

Documents like Driving License, Passport, Voter’s ID are required as proof for address.

Income Proof

Documents like Income Tax return details, passbook, bank statements can be required as proof for income.

Other documents like medical certificates, records may also be required.

Read More : ARN Number

How to choose the best ULIP?

Choosing the right ULIP for one could be a tough task since it involves taking care of many aspects such as tenure, goals, returns, etc.

Goals

ULIPs always provide a variety of objectives to cover like helping in retirement, funding for children’s future, medical facilities, etc. and helping in achieving financial goals. Since there is flexibility in switching between funds, it gets even more easier to attain financial goals.

Life Insurance Cover

ULIPs also provide cover in case of sudden demise of the policyholder, hence it is suggested to take life insurance cover requirements into consideration while selecting the right plan for yourself.

Comparing offers

It is very necessary to compare the offers provided by various plans to get a bigger picture of what is suitable. Compare all the factors and benefits regarding various ULIPs.

Also Read : New India Assurance Health Insurance Plans

Should You Invest in ULIP Plans ?

Talking about investments in ULIPs, these plans intend to provide a solution for both insurance & investment needs. However, as both the needs are of different nature, one being an expense (Insurance) and the other an investment (Investment needs), these plans are not able to offer efficient returns for a number of reasons, especially because of the exorbitant charges levied on these plans in the initial years.

Getting an adequate cover for meeting the family needs from the ULIP plans becomes quite expensive as one would have to pay hefty premiums for that. Also, the part of premium which is actually invested for generating returns is reduced with the high management & other charges imposed on them, which would mean lower returns on investments.

Another major disadvantage of ULIPs is their lock-in period. ULIPs have a 5 year lock-in period. Even beyond that, in case of redemption the surrender value is much lower than the value of the units held. So, in case you are in need of funds you need to forego a fairly substantial amount.

Also Read : Amfi Registration Number

What are the alternatives ?

Investors should consider making separate purchases for meeting both their insurance & investment needs. A great option would be to buy a term insurance policy with adequate cover as per the needs of the family. For investments, it would be better to invest in more conventional investment products, such as mutual funds - equity, debt or hybrid funds, stocks, small savings instruments, bonds, etc. The choice of instrument would depend on the investors risk appetite, investment horizon & financial goals. It would also depend on the investors comfort and understanding of each of these products. For amateurs, mutual funds are surely the most suited product.

Choosing these alternatives in place of the Combo (Insurance + Investment) providing ULIP plans, investors would be better off in terms of both costs & returns.

FAQs

Q. What is NAV ?

A. NAV is Net Asset Value which is the cost of units of a fund and is estimated in Indian Rupees.

Q. What is the lock-in period ?

A. Lock-in period is the period for which money invested in ULIP is kept locked and can’t be withdrawn in this period.

Q. Are there any charges related to ULIP ?

A. Yes, there are two types of charges usually namely mortality charge and premium allocation.

Q. Is it possible to surrender ULIP ?

A. Yes, as per IRDA guidelines, it is possible to surrender ULIPs after paying surrender charges.

Q. What is a free-look period ?

A. Free-look period is a period starting from the date of commencement of the policy till a few days in which it is possible to cancel the plan without any penalties.

Q. Is there any free-look period in ULIPs ?

A. Yes, usually there is a free-look period of around 30 days offered by some insurance companies.

Q. What is a unit ?

A. Unit is a constituent of a fund in Unit Linked Policy.

Read More Articles :